Uniform Accounting shows this company is taking advantage of more people practicing their swing in the pandemic

During the pandemic, consumers have found lots of time to take up new activities. Two popular choices are yard work and golfing. Both can easily be done while social distancing, and allows for an excuse to get out of the house.

Today’s company provides equipment used for yard work as well as golf course maintenance. Looking only at as-reported numbers, it appears a 2019 acquisition is hurting the firm’s returns.

However, UAFRS (Uniform) based analysis shows the firm’s real performance, with investors looking at bad data missing the profitability of the firm.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

In Q2 2020, Home Depot (HD) reported record sales, with revenue of $38 billion, up 23% year over year. The story is the same across the rest of the home improvement industry, with consistent revenue gains in the face of coronavirus restrictions.

As people spend more of their time at home, they are pouring more money into making their stay enjoyable. Not to mention, with all of the extra time available, people are pursuing home renovation projects they simply did not have the time for in the past.

The increased spending has not been limited to just inside the home, but extends to lawnwork and outside improvements as well. It also means more spending on outdoor activities that allow for social distancing, including things like golfing and bike riding.

In particular, in the wake of coronavirus lockdowns lifting, many states are seeing huge increases in the number of golfers. The sport has a built in measure of social distancing, and gives people the chance to escape the confines of their homes.

Wisconsin reported a 14% increase year over year in rounds played this past June. Valens even highlighted this phenomenon on Forbes a few months ago, talking about Callaway Golf.

Today’s company directly benefits from an increase in lawn care spending and an uptick in golf rounds. The Toro Company (TTC) provides turf and landscape equipment, irrigation products, mowers, and golf course maintenance equipment.

As people continue to invest in yard improvements, Toro is well positioned to benefit. Additionally, its golf course products are in high demand due to the huge increases in rounds played across the country.

In 2019, Toro expanded its offerings by acquiring privately held Charles Machine Works for $700 million. This merger diversified Toro’s products and gave the company access to the equipment market for underground construction.

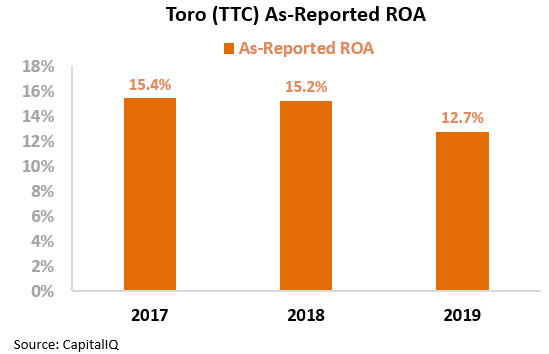

While getting exposure to this market sounds beneficial, looking at the as-reported numbers, it appears the acquisition didn’t have the positive impact Toro anticipated.

The firm’s as-reported return on assets (ROA) declined from 15% to 13% in the wake of the merger. Investors seeing this would reasonably assume Toro’s diversification efforts away from its traditional business is a drag to the firm’s core offerings.

However, this picture of Toro’s performance is inaccurate, pulled down by distortion in as-reported accounting. Due to the GAAP treatment of goodwill, among other distortions, the market is blind to the reality of Toro’s performance.

Toro’s acquisition of Charles Machine Works has allowed it to expand its products away from the more seasonal lawn equipment markets.

The Uniform ROA for Toro, in fact, rose modestly in the wake of the acquisition from 19% to 20%, not decline as as-reported metrics show. Additionally, Uniform ROA was 20% in 2019, compared to just 13% for GAAP metrics.

The acquisition has not been value-destroying, but modestly beneficial for Toro’s profitability.

However, understanding a company’s historical returns isn’t enough to decide whether the stock is a compelling buy.

To know if the firm can continue to create value for shareholders, we can use the Embedded Expectations Framework to easily understand market valuations.

The chart below explains the company’s historical corporate performance levels, in terms of ROA (dark blue bars) versus what sell-side analysts think the company is going to do in the next two years (light blue bars) and what the market is pricing in at current valuations (white bars).

As you can see, both analysts and the market expect returns to fall below current levels. Expectations are for returns to contract slightly to 18%, which would reach five year lows.

Despite Toro’s expansion into the underground equipment market, and tailwinds for growth in the residential and golf sectors, the market is pricing in no benefits for the company in the future.

Toro has expanded into less seasonally impacted businesses with its acquisitions creating a more stable company. It is also set to take advantage of trends in the home improvement market, as well as the increase in golf rounds seen during the pandemic.

Without Uniform Accounting, investors would miss a high return company with solid macro tailwinds improving its returns after a large acquisition.

Toro looks primed to capitalize on unique trends driven by the pandemic, and continue to improve returns going forward. Once the market realizes how as-reported metrics are painting the wrong picture, investors may re-think the company’s outlook.

The Toro Company Embedded Expectations Analysis – Market expectations are for Uniform ROA to slightly decline, and management may be concerned about sales, inventory, and their supply chain

TTC currently trades near corporate averages relative to Uniform earnings, with a 22.1x Uniform P/E (Fwd V/E′). At these levels, the market is pricing in expectations for Uniform ROA to decline from 20% in 2019 to 18% in 2024, accompanied by 5% Uniform asset growth going forward.

However, analysts have somewhat less bearish expectations, projecting Uniform ROA to sustain 19% levels through 2021, accompanied by 5% Uniform asset growth.

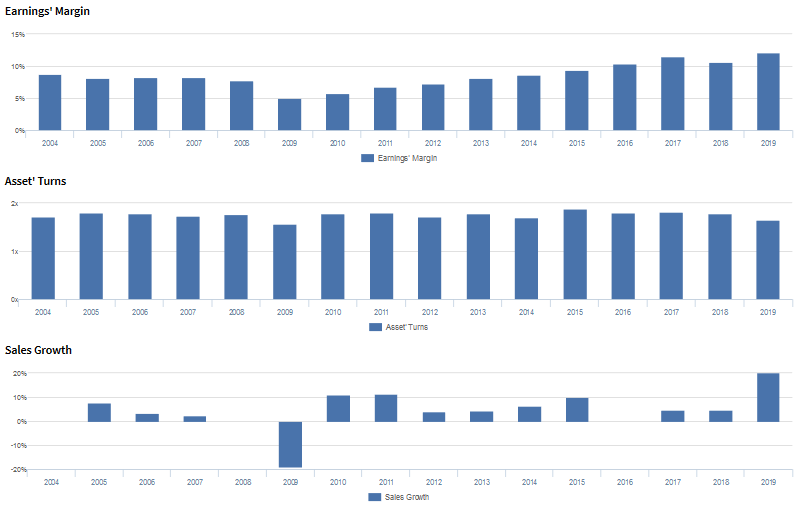

Historically, TTC has seen strong and generally improving profitability. After ranging from 14%-15% levels from 2004-2008, Uniform ROA collapsed to 8% in 2009, amid recessionary headwinds, before recovering to a peak of 21% in 2017. Since then, Uniform ROA has slightly faded to 19%-20% levels in 2018-2019.

Meanwhile, Uniform asset growth has been generally muted and somewhat volatile, positive in thirteen of the past sixteen years, while ranging from -6% to 9%, excluding outlier 24% growth in 2019, due to its Charles Machine Works acquisition.

Performance Drivers – Sales, Margins, and Turns

Overall improvements in Uniform ROA have been driven primarily by improving Uniform earnings margins, coupled with stable Uniform asset turns.

After ranging from 8%-9% levels from 2004-2008, Uniform margins compressed to 5% in 2009, before rebounding to 11%-12% peak levels in 2017-2019.

Meanwhile, Uniform turns have remained at 1.6x-1.9x levels since 2004 and currently sit at the low end of that range.

At current valuations, the market is pricing in expectations for Uniform margins to reverse recent improvements, accompanied by continued stability in Uniform turns.

Earnings Call Forensics

Valens’ qualitative analysis of the firm’s Q1 2020 earnings call highlights that management generated an excitement marker when saying the Charles Machine Works integration is well ahead of schedule due to the immediate restructuring and strategic actions they took. In addition, they are confident residential segment net sales for Q1 2020 were up 14.3% to $165.8 million.

However, they are also confident last year’s scheduled spring activity was pushed back to mid-summer due to significant snowfall in April and that Q1 2019 was followed by an unusually wet selling season, resulting in higher-than-anticipated year-end inventory.

Furthermore, they may have concerns about sales disruptions in heavily impacted coronavirus geographies and their SKUs with components produced in China.

Additionally, they may also be overstating the strength of their BOSS segment inventory positioning and their new product growth opportunities.

Moreover, they may lack confidence in their ability to execute their strategic priorities and their key Chinese suppliers’ ability to become fully operational.

UAFRS VS As-Reported

Uniform Accounting metrics also highlight a significantly different fundamental picture for TTC than as-reported metrics reflect.

As-reported metrics can lead investors to view a company to be dramatically stronger or weaker than real operating fundamentals highlight. Understanding where these distortions occur can help explain why market expectations for the company may be divergent.

As-reported metrics significantly understate TTC’s recent profitability. For instance, as-reported ROA in 2019 was 13%, substantially lower than Uniform ROA of 20%, making TTC appear to be a much weaker business than real economic metrics highlight.

Moreover, since 2018, as-reported ROA has fallen from 15% to 13%, while Uniform ROA has maintained 19%-20% levels over the same timeframe, directionally distorting the market’s perception of the firm’s profitability following the Charles Machine Works acquisition.

SUMMARY and The Toro Company Tearsheet

As the Uniform Accounting tearsheet for The Toro Company (TTC:USA) highlights, its Uniform P/E trades at 22.1x, which is below corporate average valuation levels but around its historical average valuations.

Average P/Es require average EPS growth to sustain them. In the case of Toro, the company has recently shown a 35% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Toro’s Wall Street analyst-driven forecast an EPS growth of 1% and 8% in 2020 and 2021, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Toro’s $76 stock price. These are often referred to as market embedded expectations.

The company needs to have Uniform earnings grow by 5% each year over the next three years to justify current prices. What Wall Street analysts expect for Toro’s earnings growth is below what the current stock market valuation requires in 2020 but above its requirement in 2021.

Furthermore, the company’s earning power is 3x the corporate average. Also, cash flows are 2x higher than its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit and dividend risk.

To conclude, Toro’s Uniform earnings growth is above peer averages. However, the company is trading below average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research