As customer service expectations are rapidly advancing, this firm’s services have never been more important

With new technology and offerings every year, people’s needs have only become more discerning. This tech firm has positioned itself well to be at the forefront of providing vital services.

Despite its robust operations, many investors see this firm’s various financial metrics sliding down well into the negative. However, this may not be the case once GAAP distortions are cleaned up.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

The internet is no longer a platform for static communication. Before there was enough bandwidth for audio and video calls, internet users were comfortable navigating to a frequently asked questions (FAQ) page to find the answers to their questions.

Recently, firms have entered a customer service “arms race” as more advancements in technology have become prevalent. Nowadays, customer service is expected to be robust and on demand.

This can include services such as AI chats, text customer service, audio communication and more. Customers expect companies to stay in communication with them and fix any problems 24/7.

The technology to facilitate these services is essential in the modern era of internet communication. As a result, investors might suspect a company that provides the technology to do this would generate tremendous amounts of value.

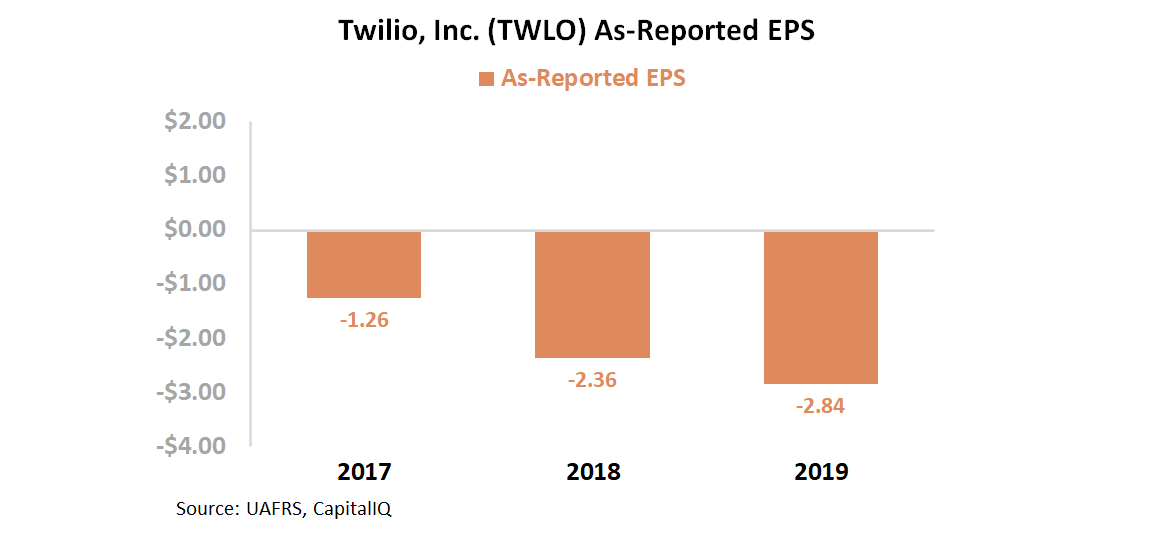

Twilio (TWLO) is a company at the heart of this technology. Yet, on an as-reported basis, the firm has seen EPS fade further negative from its already massively negative levels. This trend has occurred in an era where Twilio’s aforementioned services have become even more important.

As you can see below, it appears Twilio’s earnings story has gone from bad to worse. EPS has faded from ($1.26) levels in 2017 to ($2.84) levels in 2019.

In reality, the exact opposite has happened. Being at the center of this innovation has led to significant value creation.

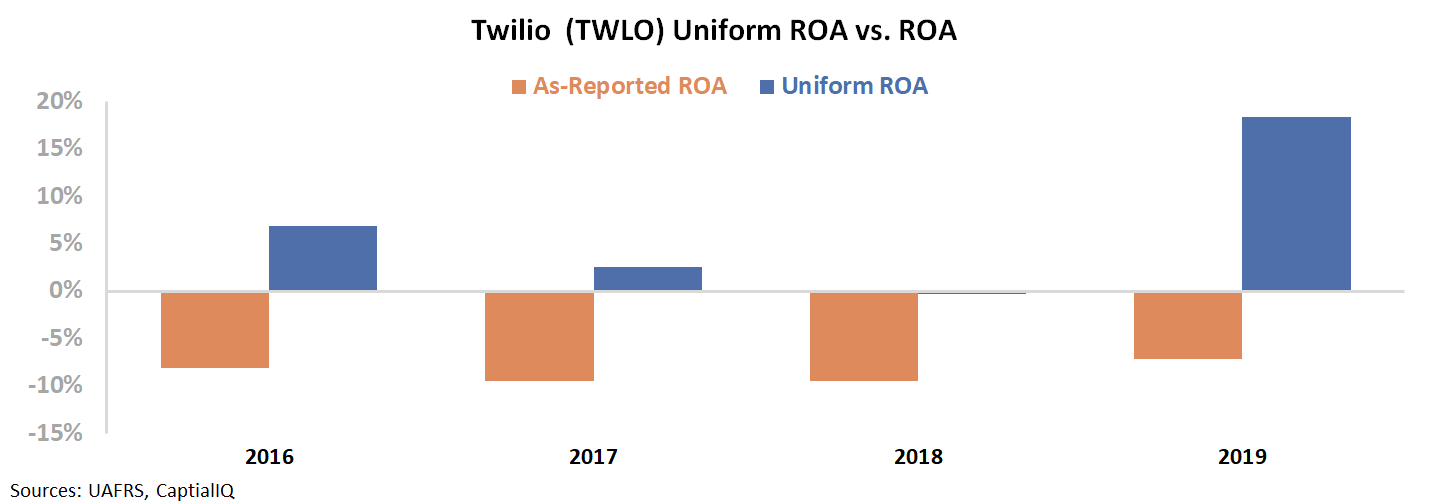

Under Uniform Accounting, EPS has not been negative during the same time period captured above. Once we make the Uniform Accounting adjustments around goodwill, stock options, and other distortions, the firm’s true earnings metrics can be analyzed.

The firm’s earnings have been driven by strong demand and sustainable services. Instead of sharply declining, Uniform EPS has increased from $0.11 in 2017 to $1.73 in 2019. In the chart below, Uniform EPS metrics are consistently higher than what the market perceives them to be.

In addition to this large discrepancy in as-reported versus Uniform EPS metrics, ROA levels are also much stronger.

Twilio has been able to generate robust returns by being at the heart of this technology.

Specifically, while as-reported ROA levels have maintained -7% to -10% levels since 2016, Uniform ROA has been improving.

Uniform ROA has expanded from 7% in 2016 to 18% in 2019. Twilio is improving performance thanks to these tailwinds, not squandering its market opportunity.

Once we make the necessary Uniform Accounting adjustments, we can see Twilio has in fact generated returns well into the positive levels. In fact, by providing innovative tech solutions, Twilio has earned premium returns in 2019.

Twilio has been profitable for years by paying attention to a space others should be operating in. However, only through using Uniform Accounting can investors see the complete picture.

SUMMARY and Twilio’s Company Tearsheet

As the Uniform Accounting tearsheet for Twilio Inc. (TWLO:USA) highlights, the Uniform P/E trades at 631.8x, which is above the global corporate average of 25.2x and its historical average of -150.5x.

High P/Es require High EPS growth to sustain them. In the case of Twilio, the company has shown a 985% Uniform EPS shrinkage in the previous year.

Wall Street analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Twilio’s Wall Street analyst-driven forecasts are a 143% EPS and 227% EPS shrinkage in 2020 and 2021, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Twilio’s $400 stock price. These are often referred to as market embedded expectations.

The company would need to grow its Uniform earnings by 72% per year over the next three years to justify current stock prices. What Wall Street analysts expect for Twilio’s earnings growth is below what the current stock market valuation requires in 2020 and 2021.

Furthermore, the company’s earning power is 3x the long-run corporate averages. Also, cash flows and cash on hand are almost 3x its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit and dividend risk.

To conclude, Twilio’s Uniform earnings growth is below its peer averages, but is trading above peer average levels.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research