Two ‘surefire’ recession indicators are saying different things

There are several datapoints people use to predict when the next recession is coming. Yield curves are popular, as are labor rates, income growth, and spending—to name a few. There are other less traditional recession indicators that have been getting attention recently, although they don’t tend to work quite as well.

Today, we’ll take a look at a handful of recession indicators and walk through what each of them is saying. There are mixed messages, although some are likely more trustworthy than others.

Investor Essentials Daily:

The Monday Macro Report

Powered by Valens Research

Investors breathed a collective sigh of relief after the World Series.

Even if you’re a diehard Philadelphia Phillies fan – or if you were tired of seeing the Houston Astros at the championships for the fourth time in six years – it was hard to wholeheartedly root for Philly.

You see, there’s a superstition about Philadelphia baseball teams. Whenever they win the World Series, the economy crashes.

The Philadelphia Athletics (before they moved to Oakland) won the World Series two weeks before the 1929 market crash that kicked off the Great Depression… and again in 1930. The Phillies won in 1980 amid plummeting stocks and mass layoffs.

Their fourth and most recent World Series victory came in 2008, during the lead-in to the Great Recession.

Philadelphia baseball is four-for-four on economic disasters. Superstitious investors were hoping it wouldn’t become five-for-five.

To these folks’ relief, the Houston Astros won the series in six games. I’m sure for many, it was too close for comfort.

That being said, a Phillies loss doesn’t guarantee there won’t be a recession.

Of course, there’s no causation between Philadelphia wins and economic ruin. It’s pure coincidence.

One metric does mean we’re almost certain we see a recession in the next six to 24 months, though.

Unlike Phillies wins, this signal is much more consistent…

We’re talking about the inverted yield curve.

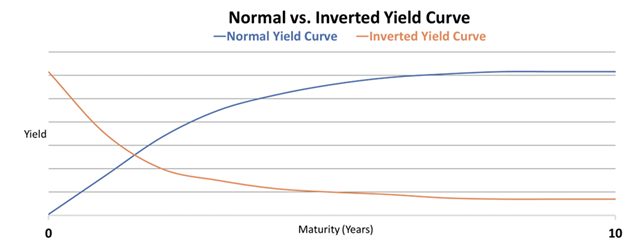

The yield curve measures interest rates of U.S. Treasury bonds over various time horizons. Normally, longer-dated bonds have higher rates because there’s more uncertainty that far out. An inverted yield curve is when short-term bond interest rates climb above long-term interest rates.

A normal yield curve means that investors are optimistic about the immediate future. When the curve inverts, it shows the market believes the economy will be worse in the short term than in the long term. That’s why it tends to indicate a looming recession.

Comparing two yields is quite simple. All you need to do is subtract the short-term rate from the long-term rate. If the result is negative, the yields are inverted.

When that happens, it looks something like this:

Yields get higher over time in a normal curve. With an inverted curve, they become lower the further out you go.

Investors look at many different kinds of yield curves. One of the most widely used is the “2-10 curve.” This compares the yield of two-year and 10-year U.S. Treasury rates.

While it’s widely used, we don’t think the 2-10 curve is the best recession indicator. Our research shows that the 10-year/three-month spread is actually the best way to identify a pending recession.

Even as rates have risen, this curve has remained positive for some time. Ten-year rates were consistently higher than what you’d find on three-month bonds. And the economy continued to chug along.

Unfortunately, this couldn’t last forever.

The 10-year/three-month curve finally inverted in late October. It was the first time this had happened since late 2019 (not long before the sharp but short-lived pandemic recession).

As you can see, on October 18, the three-month yield hit 4.04%. The 10-year yield sat at 4.01%.

Now, this doesn’t mean we’re going to see a recession tomorrow.

The 10-year/three-month inversion has historically preceded a recession by between six and 24 months.

This does confirm that the Fed’s actions against inflation are guiding us towards a recession.

That doesn’t mean it’ll be a bad recession.

The Fed is managing the economy by raising rates. While this will likely lead to a minor recession, it should rein in inflation.

Investors have been bracing themselves for a lot of risk lately. Stock prices are reflecting that. If anything, we’ll likely see a sideways market until the Fed gets inflation under control and lowers rates again.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research