This steel supplier is set to benefit from a potential supply-chain supercycle

Companies trying to optimize their supply chains have been investing in new manufacturing facilities back home in the Americas in countries like Mexico. This is called nearshoring.

As the need for new facilities in the Americas increases, the need for steel that goes into construction goes up.

That is where Ternium (TX) comes in. It sells steel in the Americas, with half of those sales coming from Mexico.

Demand for Ternium’s steel products will likely increase as the supply-chain supercycle plays out in the Americas. That means a potential upside for investors.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

U.S. companies have been offshoring for a long time.

They moved their operations and manufacturing facilities to distant countries to take advantage of lower labor and operational costs.

This seems like a pretty good business decision at first, until things go south.

The pandemic did just that. Orders got canceled, lead times got extended and manufacturers couldn’t find the raw materials they needed on time. Customers had to wait a long time to get their products, and producers’ margins suffered.

This has led companies to question their networks and search for new strategies to optimize their supply chains, investing heavily in that area.

A popular way of optimizing supply chains has been nearshoring. Companies move their manufacturing facilities closer to the customer to make operations more efficient.

It allows companies to benefit from lower costs than operating in their home country while maintaining closer geographical, cultural, and temporal alignment with their home base.

And the strategy has been growing exponentially… That is especially true for U.S. companies investing in Mexico.

That means more facilities being built and more steel needed for their construction.

This is where Ternium (TX) comes in.

The company manufactures flat and long steel products, serving customers active in the construction, automotive, manufacturing, home appliances, packaging, energy, and transport industries.

It is one of the leading steel companies in Latin America with a highly integrated process, from extracting iron ore to manufacturing high-value-added products.

The company has enjoyed surging demand thanks to nearshoring companies.

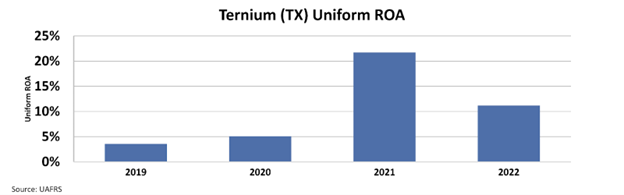

In the last two years, Ternium has enjoyed a decade-high return on assets (“ROA”) with 2021 bringing in its highest ROA figure over the last 15 years.

Take a look…

This clearly shows that the company benefited a lot from the increase in demand for steel.

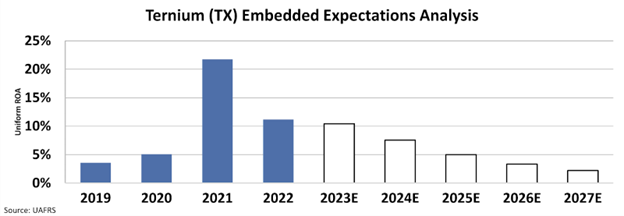

And yet, the market doesn’t seem to understand the potential growth in nearshoring activity, and how it is likely to affect the company.

We can see this through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the market expects the company’s ROA to fall critically to nearly 2%, even lower than 2019 levels.

There will be an improved demand for Ternium’s steel products as more companies nearshore their operations.

We have just started to fix our supply chains, and investments will continue for another decade. This means sustained high returns for the company.

The market’s pessimism about future returns might create an opportunity for investors.

SUMMARY and Ternium S.A. Tearsheet

As the Uniform Accounting tearsheet for Ternium S.A. (TX:USA) highlights, the Uniform P/E trades at 5.9x, which is below the corporate average of 18.4x but around its historical P/E of 4.7x.

Low P/Es require low EPS growth to sustain them. In the case of Ternium, the company has recently shown a 49% shrinkage in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Ternium’s Wall Street analyst-driven forecast is a 15% and 25% EPS shrinkage in 2023 and 2024, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Ternium’s $44.51 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 25% annually over the next three years. What Wall Street analysts expect for Ternium’s earnings growth is above what the current stock market valuation requires in 2023 but in line in 2024.

Furthermore, the company’s earning power is 2x its long-run corporate average. Moreover, cash flows and cash on hand are 1.2x its total obligations—including debt maturities, capex maintenance, and dividends. Also, the company’s intrinsic credit risk is 90bps above the risk-free rate.

All in all, this signals low dividend risk.

Lastly, Ternium’s Uniform earnings growth is in line with its peer averages but below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research