UAFRS shows how this consulting firm has unlocked value through offering unique insights, just like one of our business partners

This global research firm recently purchased a successful insights and technology company to boost its business.

Only looking at as-reported numbers, it appears this transaction, and the company’s legacy business, generates below cost-of-capital levels. However, on a closer look, its strategy produces much stronger profitability.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

A firm we work with and admire is MBO Partners. MBO is disrupting how people think about staffing. Due to its powerful marketplace for high potential independent contractors, companies have an easier way to hire high-end consultants and other staff.

This allows companies to lower their overhead costs related to legacy business models.

Now, MBO is looking to disrupt high-end knowledge based industries in a new way through its acquisition of MindSumo.

MindSumo unlocks insights for companies from a younger generation, relying on college students. Large companies like Amazon (AMZN), Facebook (FB), and Coca-Cola (KO) pose problems they are currently facing. Then, college teams submit different ideas for how to tackle the challenges.

This benefits both parties as the companies receive a wide variety of unique solutions and college students get phenomenal experience, can earn money, and pad their resumes.

By acquiring MindSumo, MBO can help bring innovation at a superior cost. Additionally, MBO is able to gain insights from a customer group that is not well captured by traditional market research.

This type of market research and innovation has been at the heart of Gartner’s (IT) businesses for years.

Gartner is a global research and consulting firm. The firm aims to provide executives with the knowledge and data they need to be successful.

Historically, Gartner targeted information technology, marketing, and supply chain executives as well as chief information officers. However, in 2017 the firm acquired CEB, a global insights and technology firm, which allowed Gartner to focus on all major functions of businesses.

While CEB does not use college students, it is similar to MindSumo in its approach to source unique solutions for its clients.

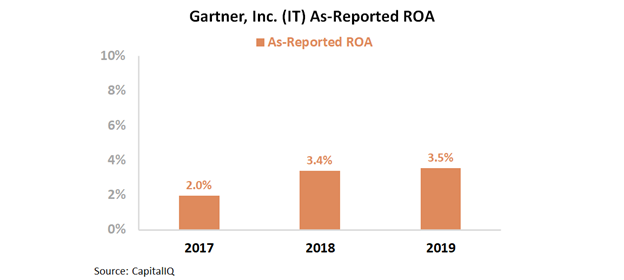

However, even with such a wide variety of powerful research offerings, it appears as though Gartner is not able to generate high returns. The firm’s as-reported return on assets (ROA) has been below cost-of-capital levels since it acquired CEB. ROA has ranged from 2%-4% over the past three years.

Looking at the weak profitability metrics of Gartner makes investors wonder whether the firm has wasted investor capital with its latest acquisition, and if MBO was wrong to purchase MindSumo.

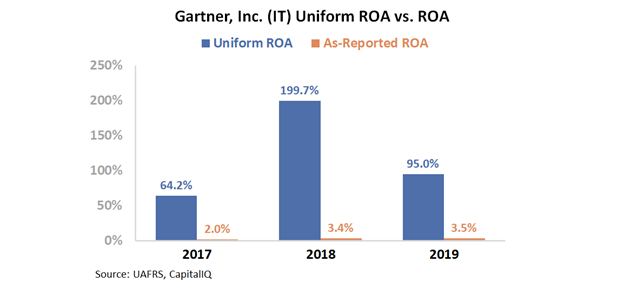

However, Gartner’s profitability metrics are being misrepresented due to the GAAP treatment of amortization and goodwill, among other distortions.

In reality, Gartner’s ROA reached an all-time high in 2018. Over the past three years, Uniform ROA has ranged from 64% to 200%. Clearly, this business is a profitable one to be in.

Uniform Accounting shows Gartner has been able to capitalize off of its recent acquisition. It also shows how MBO made a smart choice with its own acquisition by moving into a high return industry.

Gartner is a business with soaring profitability levels and conservative expectations. When looking at the Uniform numbers, it is clear this is a company investors should keep their eye on.

Gartner, Inc. Embedded Expectations Analysis – Market expectations are for Uniform ROA to remain stable, and management is confident about the strength of their business, their ability to operate remotely, and conference attendance

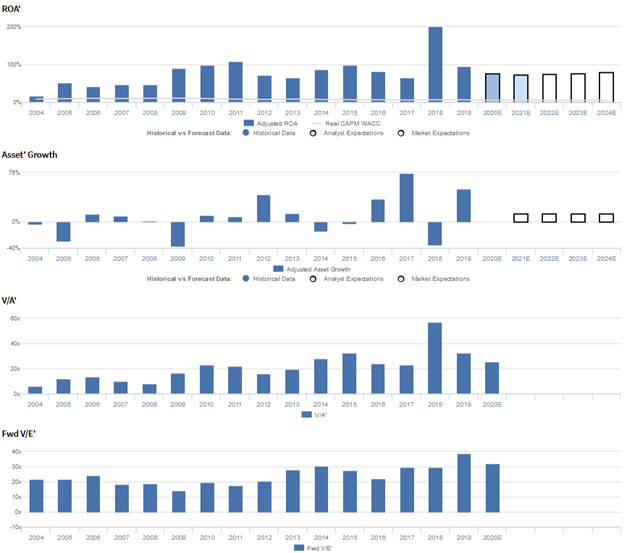

IT currently trades near recent averages relative to Uniform earnings, with a 32.3x Uniform P/E (Fwd V/E′). At these levels, the market is pricing in expectations for Uniform ROA to compress from 95% in 2019 to 80% in 2024, accompanied by 13% Uniform asset growth going forward.

However, analysts have bearish expectations, projecting Uniform ROA to fade to 74% by 2021, accompanied by an immaterial Uniform asset growth.

Historically, IT has had robust, somewhat stable profitability. After improving from 17% in 2004 to 109% in 2011, Uniform ROA stabilized at 64%-99% levels through 2017. Thereafter, Uniform ROA jumped to a peak of 200% in 2018 before dropping to 95% in 2019.

Meanwhile, Uniform asset growth has historically been volatile over the past sixteen years, ranging from -37% to 74%.

Performance Drivers – Sales, Margins, and Turns

Overall stability in Uniform ROA has been driven primarily by general stability in both Uniform earnings margins and Uniform asset turns.

Since improving from 5% in 2004 to 12% in 2010, Uniform margins have sustained 12%-13% levels through 2019. Meanwhile, after expanding from 3.2x in 2004 to 4.7x-8.8x levels in 2005-2011, Uniform turns compressed to 4.9x-7.0x levels in 2012-2014, before recovering back to 8.2x levels in 2015. Thereafter, Uniform turns fell to 5.0x in 2017 and subsequently rebounded to 15.5x in 2018, before fading to 8.2x in 2019.

At current valuations, the market is pricing in expectations for Uniform margins and Uniform turns to remain near current levels.

Earnings Call Forensics

Valens’ qualitative analysis of the firm’s Q1 2020 earnings call highlights that management generated an excitement marker when saying that they are in a stronger position than they were during the Great Recession in 2008-2009. In addition, they are confident their Research business is well-positioned to operate successfully as a virtual business, and that they had more than 1,900 total registrations for their first virtual conference.

However, management may have concerns about selling and servicing their clients remotely, the impact of supply chain interruptions, and the limited number of conferences held during Q1.

Furthermore, they may lack confidence in their ability to maintain lower cost and lower decremental margins, manage cash flow, and work through insurance recovery.

Additionally, they may be concerned about the limited marketing for their first virtual conference, the spending cut on their new office space, and continued declines in NCVI per salesperson.

Meanwhile, management may lack confidence in their ability to sustain their strong EBITDA, contribution margins, labor-based revenues, backlog coverage, and Contract Optimization revenues.

Moreover, they may have concerns about the decline in wallet retention for Global Technology Sales (GTS) business and reductions in total Global Business Sales (GBS) new business.

UAFRS VS As-Reported

Uniform Accounting metrics also highlight a significantly different fundamental picture for IT than as-reported metrics reflect.

As-reported metrics can lead investors to view a company to be dramatically stronger or weaker than real operating fundamentals highlight. Understanding where these distortions occur can help explain why market expectations for the company may be divergent.

As-reported metrics significantly understate IT’s asset efficiency, one of the key drivers of profitability.

For example, as-reported asset turnover for IT was 0.6x in 2019, materially lower than Uniform turns of 8.2x, making IT appear to be a much less efficient business than real economic metrics highlight.

Moreover, since 2016, as-reported asset turnover has fallen from 1.0x to 0.6x in 2019, while Uniform turns have remained at 5.0x-15.5x levels over the same time frame, directionally distorting the market’s perception of the firm’s recent asset efficiency trends.

SUMMARY and Gartner, Inc. Tearsheet

As the Uniform Accounting tearsheet for Gartner, Inc. (IT:USA) highlights, the Uniform P/E trades at 32.3x, which is above the global corporate average valuation levels but in-line with its historical average valuations.

High P/Es require high EPS growth to sustain them. In the case of IT, the company has recently shown a 2% growth in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, IT’s Wall Street analyst-driven forecast is a 15% EPS shrinkage in 2020 and a 4% EPS growth in 2021.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify IT’s $126 stock price. These are often referred to as market embedded expectations.

In order to justify current stock prices, the company would need to have Uniform earnings grow by 14% per year over the next three years. What Wall Street analysts expect for IT’s earnings growth is below what the current stock market valuation requires in 2020 and 2021.

Furthermore, the company’s earning power is 16x corporate average. However, cash flows are lower than its total obligations—including debt maturities and capex maintenance. Together, this signals an average credit risk.

To conclude, IT’s Uniform earnings growth is below peer averages, but the company is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research