The semiconductor shortage is causing a slew of problems for seemingly everyone but this company

Smart investors always have an ear to the ground to be aware of current events, to protect a portfolio from risk, or lean into a potentially evolving trend.

This company may be one of the biggest winners as they are primed to see strong demand as the capacity for semiconductor chips expand.

However, rating agencies depict otherwise.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Wednesday Tearsheets

Powered by Valens Research

Yesterday, we wrote about how Intel (INTC) is trading at higher valuations than investors realize, and how people should be mindful before jumping in.

We also discussed how new leadership is taking the company in a direction many did not expect. They are striving to become a powerhouse in manufacturing as many chips as possible.

As we highlighted, right now the world is facing a serious scarcity of semiconductor chips. And one of the most important ways that is going to be solved is by building more semiconductor fabrication plants.

Building out these fabrication plants will help companies grow capacity constraints, and it will help alleviate some of the pressures being caused by the current shortage.

As always, when an event as big as this takes place, there will always be potential winners and losers from the aftermath.

The biggest winners of building out more fabrication plants will be the chip equipment manufacturers.

These players in the space are likely to see years of strong demand as capacity expansion continues to be driven by climbing demand.

For example, companies like Ultra Clean Holdings (UCTT) will prosper.

On a higher level, Ultra Clean Holdings makes equipment that semiconductor manufacturing equipment companies need to make their products.

By providing such valuable services for the manufacturers everyone needs, Ultra Clean Holdings sits at the heart of demand within the space.

That said, it looks like rating agencies are making a major mistake when rating Ultra Clean Holdings’ debt.

Despite the potential for a surge in chip capacity expansion thanks to more semiconductor fabrication plants being built, the major rating agencies are still skittish when rating Ultra Clean Holdings’ debt.

Specifically, S&P gives the company a highly speculative B+ rating, with the implied assumption of a 25%+ risk of default over the next five years.

It seems like the S&P did not get the memo around the potential for the company with these many secular tailwinds in store.

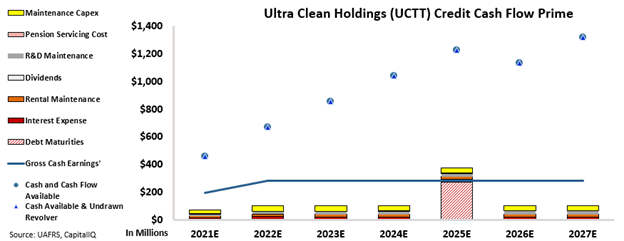

However, our Credit Cash Flow Prime (CCFP) analysis is able to get to the heart of the firm’s true credit risk.

In the below chart, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

As depicted, Ultra Clean Holdings has massive cash liquidity and therefore should have no issues handling its obligations going forward.

The company’s cash flows alone should comfortably exceed all operating obligations through 2027. On top of this, even if the firm faces some pressures on cash flows into the future, its ample cash on hand and available cash should be more than sufficient to handle all obligations, including $275 million in debt maturities in 2025.

Rather than a name in distress, Ultra Clean Holdings actually has a rock-solid balance sheet. This is why S&P’s highly speculative B+, with a 25%+ risk of default expectation does not make sense.

Using the CCFP analysis, Valens rates the company as an investment grade IG3+ rating. This rating corresponds with a default rate below 1% within the next five years, a more realistic projection once a holistic understanding of the company’s risk is taken into account.

Ultimately, Uniform Accounting and the Credit Cash Flow Prime analysis highlights how Ultra Clean Holdings’ credit risk profile is much safer than what rating agencies believe.

SUMMARY and Ultra Clean Holdings, Inc. Tearsheet

As the Uniform Accounting tearsheet for Ultra Clean Holdings, Inc. (UCTT:USA) highlights, the Uniform P/E trades at 15.8x, which is below the global corporate average of 23.7x, but above its historical average 11.1x.

Low P/Es require low EPS growth to sustain them. That said, in the case of Ultra Clean Holdings, the company has recently shown a 117% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Ultra Clean Holdings’ Wall Street analyst-driven forecast is an EPS growth of 25% and 21% in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Ultra Clean Holdings’ $56.33 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 3% annually over the next three years. What Wall Street analysts expect for Ultra Clean Holdings’ earnings growth is above what the current stock market valuation requires in 2021 and 2022.

Furthermore, the company’s earning power is 4x the corporate average. Also, cash flows and cash on hand are almost 6x above its total obligations—including debt maturities, and capex maintenance. However, intrinsic credit risk is 600bps above the risk-free rate. Together, this signals a high credit risk.

To conclude, Ultra Clean Holdings’ Uniform earnings growth is below peer averages and the company is trading below average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research