This consulting firm’s underfunded pension has the rating agencies panicked, for all the wrong reasons

Many companies are phasing pensions out of their benefit plans due to the high costs. Many other firms have left these pensions underfunded, leading them to be labeled as higher credit risks.

Today’s company is an information technology firm with a massively under-funded pension that has the credit markets concerned.

Below, we show how Uniform Accounting restates financials for a clear credit profile. We also provide the equity tearsheet showing Uniform Accounting-based Performance and Valuation analysis of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

One of the most famous lines in the movie Wall Street is Gordon Gecko’s manifesto statement scene: “Greed is good!”

However, in understanding investing, an equally impactful scene is when Charlie Sheen’s character Bud Fox realized he has served up his father’s company.

He helps Gecko in a hostile takeover. He then finds out Gecko planned to raid the company’s overfunded pension before breaking up the company. Fox’s father would lose his pension as would thousands of other employees.

In the modern investing world, this strategy of raiding an overfunded pension is rare. This is because pensions are rarely overfunded, as companies look to cut back on costs and run a lean operation.

A far more common occurrence are underfunded pensions. This means the retirement plan has more money owed to its retirees than assets to pay them. The money needed to cover the current and future payments is not readily available.

One such company with an underfunded pension is Unisys Corporation (UIS). Unisys is a global information technology firm that provides IT services, software, and technology solutions to governments, banks, and commercial markets.

Unisys has over $1.6 billion in unfunded pension liabilities, which looms over its $670 million market cap. This has led rating agencies to rate Unisys as a high-yield credit, headed for bankruptcy.

However, the rating agencies are missing a key issue. Pension plans do not drive companies into bankruptcy.

At first glance, it appears there have been multiple auto and airline firms forced into bankruptcy thanks to their pensions. However, these firms were not pushed into bankruptcy, but chose to do so to clean up their pension plans and other debts.

There is no incentive for a pension plan to push a company into bankruptcy because it significantly reduces the chances of pensioners to ever get paid. Additionally, Unisys is reliant on U.S. government contracts, making it even less likely to declare bankruptcy to wipe out its pension obligations and risk political blowback.

Not to mention, Unisys has over $800 million in cash on the balance sheet, giving the firm the ability to fund the pension if it really needed to.

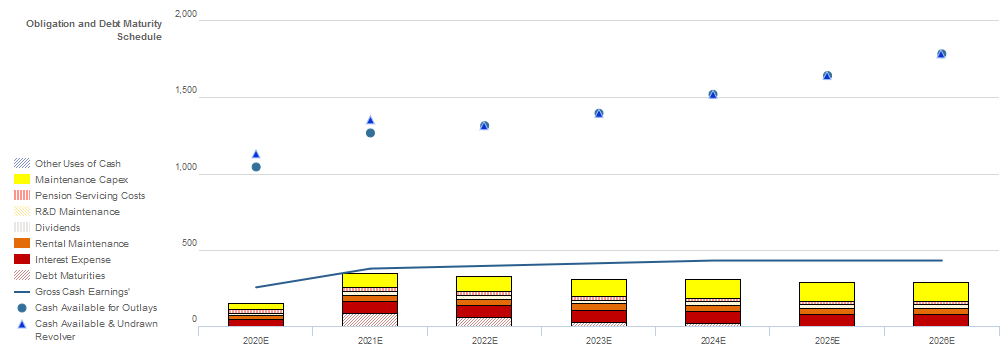

Looking at the firm’s Credit Cash Flow Prime (CCFP), it highlights the safety of the firm’s credit.

Cash flows will be sufficient to meet all obligations through 2026. In addition, Unisys has a mountain of cash that is providing a safety net for the firm’s credit.

Moody’s rates the firm as a highly speculative B2 investment. This would imply the firm is at risk of bankruptcy, despite its strong liquidity position.

Factoring in its strong liquidity position, Valens rates Unisys as a much safer investment-grade IG3 (A2) credit.

Ultimately, Unisys is seen as a credit risk because rating agencies are utilizing traditional metrics and are misunderstanding pension risk. However, when looking at Unisys’ CCFP from a Uniform Accounting perspective, the firm’s true minimal credit risk can be seen.

Unisys should have sufficient cash flows to pay off all obligations including pension servicing costs while still maintaining a large cash balance. Thus, the company is a safer credit risk than what Moody’s gives it credit for.

UIS’ Credit Risk Remains Overstated by Moody’s Despite Healthy Liquidity Levels

CDS markets are grossly understating credit risk with a CDS of 168bps relative to an Intrinsic CDS of 525bps. However, Moody’s is grossly overstating UIS’ fundamental credit risk with their highly speculative, high-yield B2 credit rating 9 notches below Valens’ IG3 (A2) rating.

Fundamental analysis highlights that UIS’ cash flows should exceed operating obligations in every year going forward. Moreover, the combination of the firm’s cash flows and sizable expected cash build would far exceed all obligations—including debt maturities—going forward.

However, the firm’s lackluster 40% recovery rate on unsecured debt, minimal market capitalization, and substantial $1.6 billion pension obligation may inhibit their ability to access credit markets to refinance, if necessary.

Incentives Dictate Behavior™ analysis highlights positive signals for credit holders, as UIS’ compensation framework should drive management to focus on all three value drivers, likely leading to Uniform ROA expansion and increased cash flows available for servicing obligations.

Furthermore, management members have low change-in-control compensation, which implies that they are less incentivized to seek a sale or accept a buyout of the company, limiting event risk for creditors. That said, management members are not material owners of UIS equity relative to their average annual compensation, indicating that they may not be well-aligned with shareholders for long-term value creation.

Earnings Call Forensics™ analysis of the firm’s Q2 2020 earnings call (8/5) highlights that management is confident in their ability to increase their win rate for contracts.

However, they may be exaggerating the rebound in ticket volumes and the strength of their Net Promoter score. They may also lack confidence in the sustainability of demand for their digital transformation and cybersecurity offerings and in their machine learning functionality.

Moreover, they may also be concerned about their full year outlook, and about the potential for continued decline in their Adjusted EBITDA margin. Finally, they may lack confidence in their plan to utilize traditional debt to mitigate their pension deficit and may be concerned about the cash charge they will take after reassessment of their real estate portfolio.

While UIS’ lackluster recovery rate and minimal market capitalization indicate that CDS markets are understating credit risk, their robust cash flows and healthy liquidity levels indicate Moody’s is overstating fundamental credit risk. As such, a widening of CDS spreads and a ratings improvement are likely going forward.

SUMMARY and Unisys Corporation Tearsheet

As the Uniform Accounting tearsheet for Unisys Corporation (UIS:USA) highlights, the company trades at a 21.1x Uniform P/E, which is below global corporate average valuation levels, but slightly above its own historical average valuations.

Low P/Es require low EPS growth to sustain them. That said, in the case of Unisys, the company has recently shown a 57% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Unisys’ Wall Street analyst-driven forecast projects a 45% EPS contraction in 2020, before a 6% growth in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Unisys’ $10.69 stock price. These are often referred to as market embedded expectations.

The company can have its Uniform earnings shrink by 1% each year over the next three years and still justify current prices. What Wall Street analysts expect for Unisys’ earnings growth is far below what the current stock market valuation requires in 2020, but above its requirement in 2021.

Furthermore, the company’s earning power is 2x the corporate average. That said, intrinsic credit risk is 480 bps above the risk-free rate. Together, this signals an average credit risk.

To conclude, Unisys’ Uniform earnings growth is far below peer averages, and the company is also trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research

View All