This Company Employs the Nurses Taking Care of You, that You Don’t See at Your Bedside

If you’ve ever been in a hospital, whether your memory of the visit was good or bad, you probably remember your nurses.

Nurses are the front line of healthcare, managing patient care, acting as the face and main touchpoint at any hospital. They are often the first person a patient sees if they’re in the hospital overnight, as they come in to check their vitals and bring their medications, and the last person they see at night.

Nurses’ position on the front lines, and their position as first and foremost a patient’s advocate in their healthcare, is the reason they are listed in many surveys as the most trusted profession in the world.

But what if I told you that for every nurse you’ve seen taking care of you at a hospital, there is another nurse that is just as dedicated to your health and wellness, tracking you every day at the hospital, but you just never met her or him? In fact, there are several.

It is ironic that one of the least trusted businesses in America, health care insurance companies, are some of the largest employers of nurses. UnitedHealth Group (UNH) employees 23,000 nurses – it is one of the largest employers of nurses in the US.

And those nurses don’t just stop taking care of patients once they join the insurance company.

UnitedHealth and the other HMOs employ nurses in many roles, including utilization review. These are the nurses, from both the healthcare facility or the HMO, that track a patient’s journey through their care, making sure they are getting the care they need, and helping them arrive at the medical outcomes they want. “The right care, at the right time, in the right place.”

You may never see them when you’re at the hospital, but they are in active contact with the nurses and other staff at a hospital, tracking your care.

Without them, bills wouldn’t get paid, your journey from your hospital visit to homecare or to a rehab facility may not ever occur, and any number of things might break down. They help patients move through the system.

UnitedHealth doesn’t just employ nurses in utilization review, they employ nurses throughout their organization. This includes in their Optum organization, where UnitedHealth innovates around technology and innovation to drive better healthcare outcomes. Nurses and other health care professionals work throughout this division around value-based care initiatives, in the company’s data and analytics and innovation, and in other initiatives.

Optum has become a massive part of what UnitedHealth does. It now contributes almost 50% of UnitedHealth’s profit as of 2018, and it has made United much less exposed to regulatory risks in US healthcare.

That’s important as at current valuations, the market is pricing UnitedHealth like they are an HMO that is waiting to get disrupted by the various healthcare initiatives that are being discussed in the current presidential election. In reality, thanks to Optum, UnitedHealth is as much a healthcare technology company as they are an HMO.

And with management showing confidence about their initiatives in both their HMO and new innovative businesses, it appears that the markets may need to start to realize that UnitedHealth is not going to see the operational pressures investors appear to be concerned about.

We just saw a recession warning sign fire, do we need to be worried? Register for our webinar this Friday to find out

One of the most important indicators of the recessionary risk is access to credit in the market.

A key indicator we monitor around access to credit just inflected negatively. But does that mean we need to be concerned about a recession this quarter, next year, when does that mean?

You are invited to attend a webinar to hear about the latest macro insights on the markets.

Valens Market Phase Cycle™ uses a framework powered by better financial and market metrics, to be able to simplify the signals the market is seeing. By starting with market cycles, and drilling down into equity and credit valuations and market sentiment in a consistent repeatable way, we can help you see better short-term and long-term signals for client asset allocation.

Our Director of Research will be reviewing this month’s Market Phase Cycle, our systematic macro analysis, discussing how looking at a consistent framework and cleaned-up analytics is so important for investors, and giving a quick introduction to using our platform, the Valens Research app.

The webinar will be Friday, 11/22, at 12pm EST, and will be less than 30 minutes

If you are interested in attending, please register below.

Register for this 30-minute webinar on using superior macro research.

Friday, November 22nd, 2019

12:00pm to 12:30pm

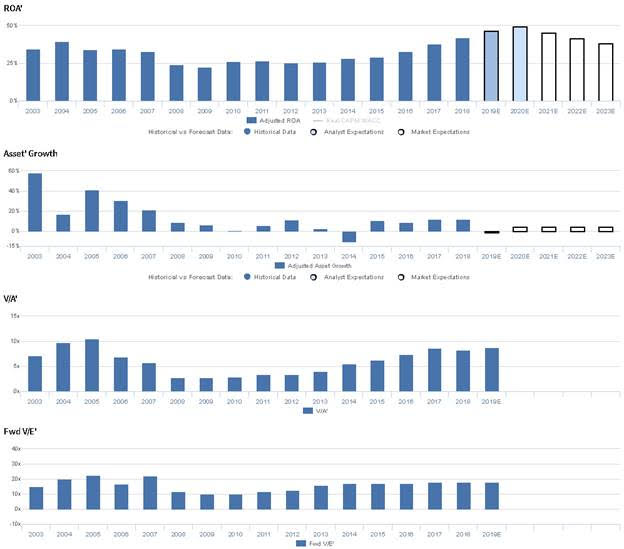

Market expectations are for declining Uniform ROA, but management is confident about their net promotor score, costs, and bed days

UNH currently trades below recent averages relative to UAFRS-based (Uniform) Earnings, with a 17.9x Uniform P/E. At these levels, the market is pricing in expectations for Uniform ROA to contract from 42% in 2018 to 39% in 2023, accompanied by 4% Uniform Asset growth going forward.

Meanwhile, analysts have bullish expectations, projecting Uniform ROA to improve to 50% by 2020, accompanied by 1% Uniform Asset shrinkage.

Historically, UNH has seen robust, somewhat cyclical profitability. Prior to 2007, Uniform ROA ranged from 33% to 40% levels, before falling to 22% in 2009. Subsequently, profitability jumped to 29% in 2010, before expanding to peak 42% levels in 2018. Meanwhile, Uniform Asset growth has been much more volatile, positive in 15 of the past 16 years, while ranging from -10% to 58%.

Performance Drivers – Sales, Margins, and Turns

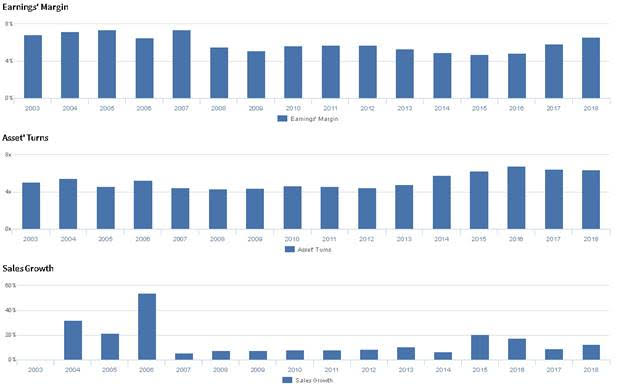

Robust profitability has been driven by offsetting trends in Uniform Earnings Margin and Uniform Asset Turns. After sustaining 7% levels from 2003 to 2007, Uniform Margins fell to 5%-6% levels through 2017 before improving back to 7% in 2018. Meanwhile, Uniform Asset Turns improved from 5.0x in 2003 to 5.5x in 2004, before declining to just 4.4x by 2008. Afterwards, Uniform Turns steadily improved to peak 6.8x levels in 2016, before falling to 6.4x in 2018. At current valuations, markets are pricing in expectations for recent Uniform Margin expansion to reverse, coupled with further declines in Uniform Turns going forward.

Earnings Call Forensics

Valens’ qualitative analysis of the firm’s Q3 2019 earnings call highlights that management is confident their recent net promoter score has shown positive improvement, and they are confident in their ability to provide higher-quality outcomes at a lower cost. Furthermore, they are confident they are working to bring together their ambulatory assets to reduce cost, and they are confident they will continue to see flat to declining bed days and admissions.

However, management may lack confidence in their ability to seamlessly integrate pharmacy into their services and sustain recent cash flow improvements. Furthermore, they may be concerned about market demand for their Bind, NexusACO, and All Saves products, and they may lack confidence in their ability to drive growth through their distribution network. Finally, they may be exaggerating expectations for potential savings from their automation efforts, and they may be concerned about their competitors’ pricing.

UAFRS VS As-Reported

Uniform Accounting metrics also highlight a significantly different fundamental picture for UNH than as-reported metrics reflect. As-reported metrics can lead investors to view a company to be dramatically stronger or weaker than real operating fundamentals highlight. Understanding where these distortions occur can help explain why market expectations for the company may be divergent.

As-reported metrics significantly understate UNH’s asset utilization, a key driver of profitability. For example, as-reported asset turnover for UNH was 1.5x in 2018, substantially lower than Uniform Turns of 6.4x, making UNH appear to be a much weaker business than real economic metrics highlight. Moreover, as-reported asset turnover has been at 1.4x-1.5x levels since 2008, while Uniform Turns have risen from 4.4x to 6.4x during the same period, directionally distorting the market’s perception of asset efficiency trends for over a decade.

Today’s Tearsheet

Today’s tearsheet is for SAP SE. SAP trades at a premium to market average valuations. The company has recently had robust Uniform EPS growth, and after a dip in 2019 is forecast to see that continue in 2020. At current valuations, the market is expecting the company to grow in line with analyst forecasts for the next 2 years, implying the market may correctly understand SAP’s fundamentals. The company’s earnings growth for 2019 is below peer average levels, but the company trading at peer average valuations. The company has strong returns, with no risk to their dividend.

Regards,

Joel Litman

Chief Investment Strategist