The world’s best investors offer a secret on how to outperform the market in the long-run

The world’s most famous investors, from Benjamin Graham and Shelby Davis to Warren Buffet and Seth Klarman know that as-reported financial metrics are unreliable.

To be successful, they make adjustments to the financial statements to produce a true picture of economic reality, one that is otherwise obscured by arcane accounting principles. This allows them to find companies that exhibit three characteristics: high quality, strong growth potential, and low valuations.

Today, we highlight a top stock from our QGV 50, which emulates this investment strategy to produce outsized returns in excess of the market over long periods of time.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

Throughout financial market history, many of the world’s most successful investors have been candid in their belief that Generally Accepted Accounting Principles (“GAAP”) distort economic reality.

Take Warren Buffet for example, perhaps the most well known money manager of his generation, who said investors should “concentrate on the world of companies, not arcane accounting mathematics.”

Investors who neglect the very real issues with as-reported accounting can find themselves caught up investing with the crowd, blindly following hot “themes” without a thorough grasp of how to understand the businesses in question.

The only true way to focus on the “world of companies” as Buffet suggests investors do, is to present a clear picture of how a business operates, something that can only be done by adjusting financial statements to reflect the arbitrary nature of certain accounting rules that leave much to discretion.

The world’s best investors understand the need to make these adjustments, which allows them to focus not on picking out the most popular companies, but rather looking for great names in sleepy areas that the market isn’t paying much attention to. From there, the goal is to then identify quality companies with significant growth potential at reasonable prices.

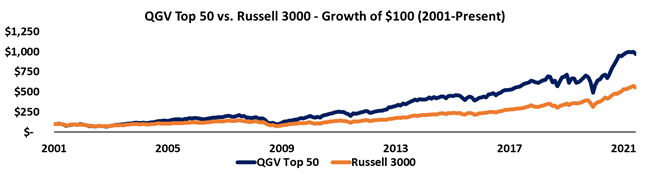

That’s exactly what we’ve set out to do with the QGV 50, our monthly list of 50 companies that rank at the top for quality, high growth, and low valuations.

This list has outperformed the market by 300bps per year for over 20 years now, effectively doubling the performance of the market by focusing on the real fundamentals and valuations of companies with our proprietary Uniform Accounting framework.

See for yourself below.

One of the top companies on this month’s list is Upland Software (UPLD), a provider of cloud-based work management solutions that allow businesses to successfully navigate the digital transformation.

The Austin, TX-based company’s software helps businesses in areas ranging from marketing and sales, to information technology and human resources, with innovative features like knowledge management, mobile application marketing, and Voice of Customer engagement.

This description of Upland is the long way of saying the company provides a plug-and-play set of solutions to help companies become smarter and more efficient.

In the future, less knowledge and fewer processes are going to be held by humans. Instead, more areas of everyday work flow will become reliant on automated systems, making Upland’s services especially critical for businesses to have at their disposal.

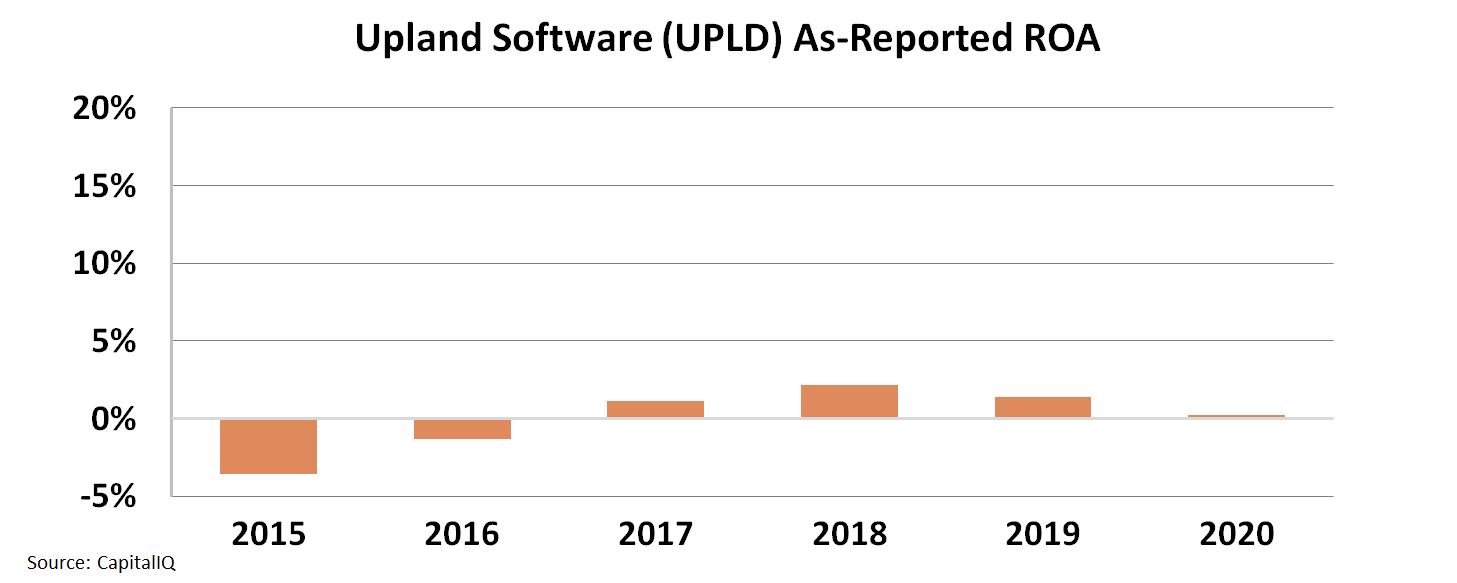

One would assume that a company empowering the digital transformation would be a high-return business. However, looking at the as-reported data, investors assume its offerings didn’t provide any value to customers. Upland Software had a 1% return on assets (“ROA”) in 2019 and near 0% ROA in 2020.

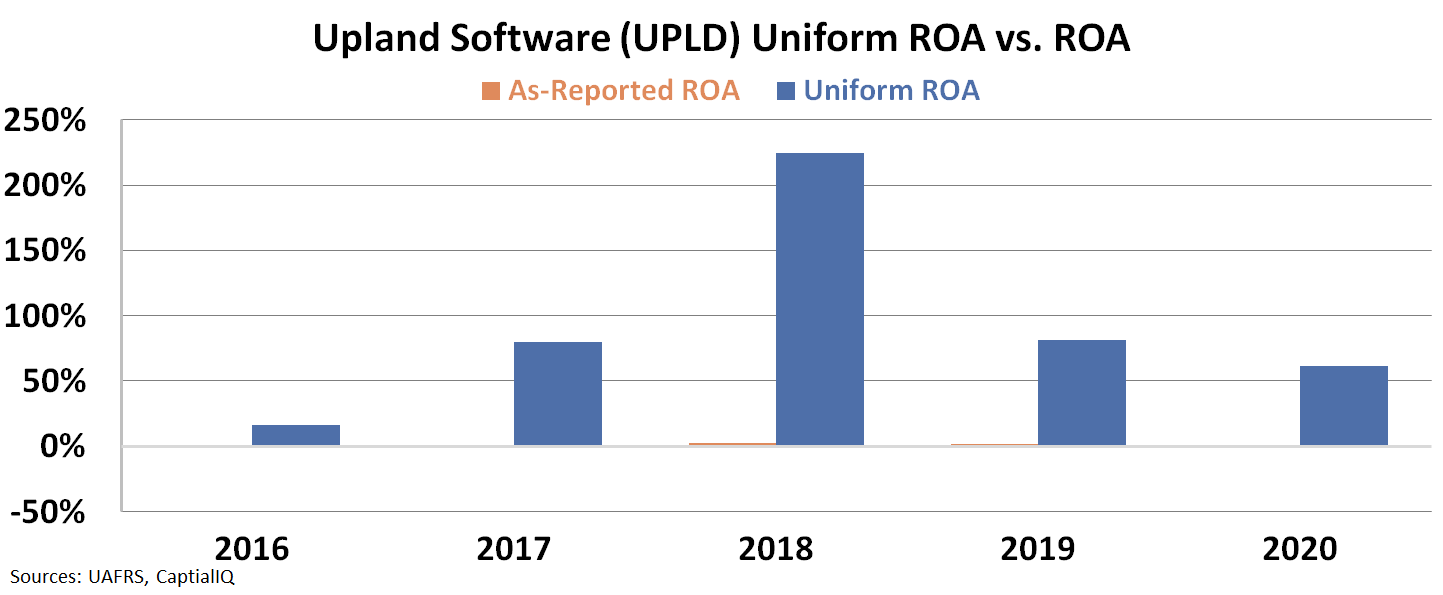

In reality, Uniform Accounting metrics show that Upland and its innovative software solutions do in fact provide tremendous value for customers, all while growing remarkably fast in what is a booming industry.

Thanks to strong demand for its solutions, Uniform ROA was actually 62% last year, not 0%. Not only that, the company has been re-investing in itself for the future, growing its asset base at a breakneck 144% pace in 2019 and a 55% rate in 2020.

With a Uniform price-to-earnings ratio (“P/E”) of 19.6x, this fast growing, highly profitable software business trades slightly below market averages as well, making it a compelling name checking off all the boxes of quality, growth, and value.

Looking at only the as-reported numbers, accounting distortions would lead investors to believe Upland is an unprofitable software business, despite what economic reality tells us. This creates scope for investors to miss a potentially great opportunity in an industry of the future.

Finding great companies with growth potential trading at favorable prices shouldn’t be this easy, especially in the current market environment. Yet, with Uniform Accounting it is, and that’s why the QGV 50 has had such tremendous success beating the market over the years.

To learn more about the QGV 50 and see the other 49 companies on the list, click here to get full access today.

SUMMARY and Upland Software, Inc. Tearsheet

As the Uniform Accounting tearsheet for Upland Software (UPLD:USA) highlights, the Uniform P/E trades at 19.6x, which is below the global corporate average of 24.3x but above its historical P/E of 17.9x.

Low P/Es require low EPS growth to sustain them. In the case of Upland, the company has recently shown a 1% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Upland’s Wall Street analyst-driven forecast is a 64% EPS shrinkage in 2021 and a 102% EPS growth in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Upland’s $34 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink 4% annually over the next three years. What Wall Street analysts expect for Upland’s earnings growth is above what the current stock market valuation requires in 2021 and below in 2022.

Furthermore, Upland’s earning power in 2020 is 10x the long-run corporate average. Moreover, cash flows and cash on hand are 4x its total obligations—including debt maturities and capex maintenance. However, intrinsic credit risk is 260bps above the risk-free rate. All in all, this signals a low dividend but moderate credit risk.

Lastly, the company’s Uniform earnings growth is near its peer averages and the company is trading around its average peer valuations.

Best Regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research