There is money in infrastructure if investors know where to look

With a huge increase of homes built and sold in 2020, one of the secondary effects has been the need for more infrastructure to support these homes.

Today’s company works to support this infrastructure construction. This is already a significant opportunity, and Biden’s infrastructure bill could only add more value to this business. Under as-reported metrics, it would appear today’s company has never been able to achieve real profitability.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

Over the past year, few industries have been able to shake off their traditional cyclicality to see prolonged booms like homebuilding and home sales.

Thanks to the transformations caused by the pandemic and At-Home Revolution, this space has been thriving.

Homebuilders have not even been able to keep up with the demand for new homes, as U.S. home inventory continues to fall. Traditionally, homebuilding has slowed in the winter months as moves are down. However, sales and building has continued unabated.

To keep up with this demand, homebuilders have needed to invest in building out full communities. This means roads, drainage systems, streetlights, and more all have to be planned out and built.

As a result, the United States in total needs more infrastructure built than a normal cycle.

On top of this, Biden’s new proposed infrastructure bill could account for roughly $900 billion to $2 trillion in spending for infrastructure.

While not all of this bill is allocated solely to infrastructure, the hope is infrastructure spending will stimulate the economy while investing in America’s future.

You can imagine that anyone who makes or supplies construction equipment will see massive opportunities from this development.

That even includes one of the largest players in the space, particularly in the heavy equipment rental business.

United Rentals (URI) offers rental equipment to construction and industrial companies, manufacturers, utilities, and government entities.

They dominate the industry with their sheer market share and array of product offerings.

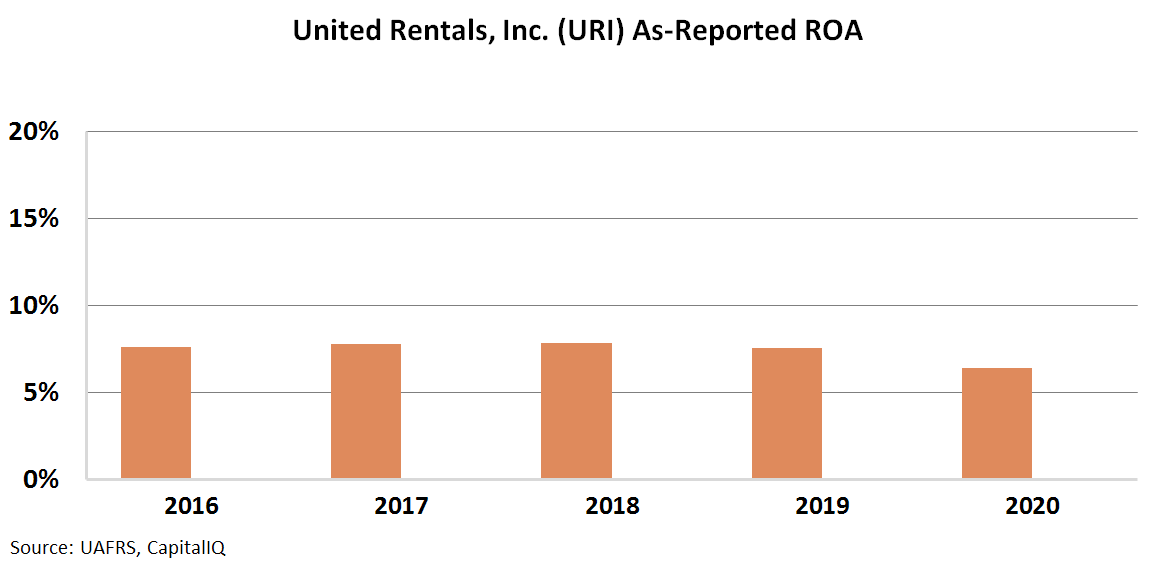

However, the as-reported metrics of the company highlight there is no money to be made in this market domination.

Specifically the company has generated return on asset (ROA) levels between 6% and 8% over the past five years.

This is well below the U.S. corporate average of around 12%. These profitability levels are not going to return a lot of capital to shareholders.

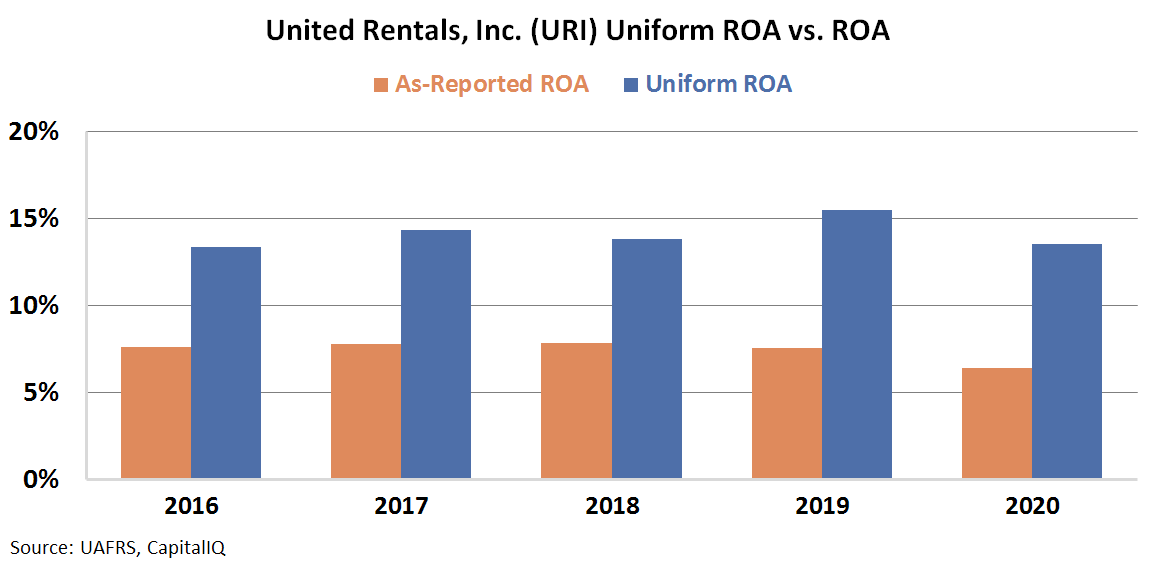

In reality, this is not an accurate picture of United Rental’s profitability.

The company is not generating returns below the corporate average. The company has actually generated returns of at least 13% every year since 2016.

When looking through a Uniform Accounting lens, it becomes clear the company’s dominance in the market has paid off.

By looking at better, cleaned up data, investors can realize the strong performance of United Rentals.

Even better, this strong historical performance in terms of profitability levels is before the surging demand coming into the works now with the increased infrastructure spend.

The company has great opportunities ahead given its positioning.

SUMMARY and United Rentals, Inc. Tearsheet

As the Uniform Accounting tearsheet for United Rentals, Inc. (URI:USA) highlights, the Uniform P/E trades at 21.4x, which is below the global corporate average of 23.7x, but above its own historical average of 16.2x.

Low P/Es require low EPS growth to sustain them. That said, in the case of United Rentals, the company has recently shown a 4% Uniform EPS contraction.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, United Rentals’ Wall Street analyst-driven forecast is a 6% EPS contraction in 2021 and 9% EPS growth in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify United Rentals’ $320 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 3% annually over the next three years. What Wall Street analysts expect for United Rentals’ earnings growth is below what the current stock market valuation requires in 2021, but way above that requirement in 2022.

Furthermore, the company’s earning power is 2x the long-run corporate average. Also, intrinsic credit risk is 170bps above the risk-free rate and cash flows and cash on hand are 1x above its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals an average dividend and credit risk.

To conclude, United Rentals’ Uniform earnings growth is below its peer averages and the company is trading in line with its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research