Using accurate data and the right peer group proves how this firm has totally outclassed its industry

Industry classification systems can be a simple way to identify a company’s peers. Investors need to tread lightly, though. While industry groups should provide useful peer groups, that’s not always the reality.

Today’s company is a semiconductor firm that looks like another struggling chip manufacturer on paper. Using Uniform Accounting, it becomes clear how the firm has actually bucked the trend.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

Industry classification systems are imperfect.

At times, they can be a valuable shortcut for investors. For instance, if you are looking at casino stocks or mobile telecommunications companies, those listed in the sub-industry can be quickly compared. With similar business models, any outliers in performance can be picked out and studied.

For many other sub-industries, the classifications can be misleading. The companies within them may have materially different business models, which makes any cross-company insight you might uncover pointless to compare.

In these scenarios, investors must do extra research to parse out which companies are actual peers.

For instance, it’s easy to run into this issue in the pharma and biotech industries. If investors don’t match companies based on the type of medical issues they treat, they end up comparing companies with completely different end markets, product cycles, or economics.

This will lead to faulty analysis.

Similarly, systems software companies run into the same problem. Systems software is a blanket term used to describe an array of companies, from tech mega-giant Microsoft (MSFT), to security software company Palo Alto (PANW), and small ERP software providers such as Progress Software (PRGS).

Each of those companies have a totally different product cycle. The firms all market and sell their products to completely different clients and end users.

Typically, people think of semiconductor companies as a lock-step industry. In other words, it ‘should’ move up and down in unison. This would mean comparing semiconductor companies against each other shouldn’t be a problem.

However, this is yet another example of an industry that is far from homogenous.

The semiconductor industry contains solar panel companies, CPU companies, cell phone chip companies, memory chip companies, and GPU chip companies that have end markets ranging from games to artificial intelligence to crypto mining.

Furthermore, there are chip manufacturers that make chips to power IoT devices, store audio files, be used in analog devices, or facilitate digital data transformation for industrial purposes.

With all those different company focuses, it becomes clear just how diverse the semiconductor industry is. All those companies have different drivers, different product cycles, and different profitability trends.

Within this broad industry, Analog Devices (ADI) is one of the companies focused on the data conversion and industrial functions side of the market.

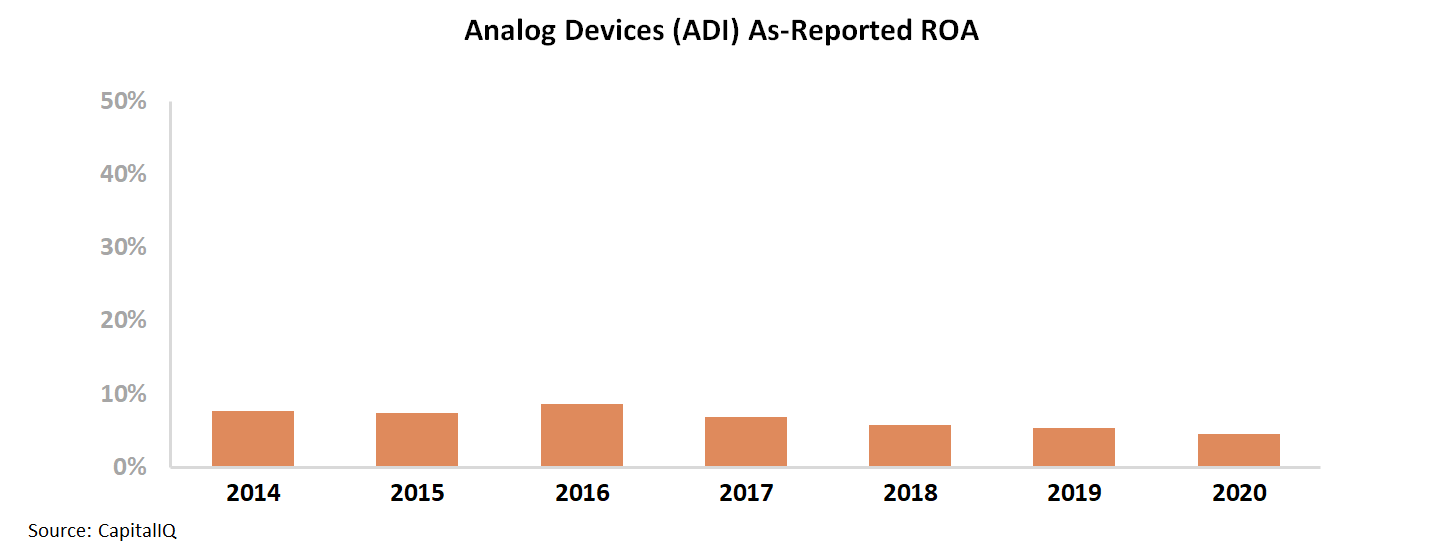

Using as-reported metrics, investors couldn’t be blamed for thinking of the company as yet another in a long line of generic, low-performing, and struggling semiconductor firms.

Since 2014, the company has seen its as-reported ROA consistently dwindle from 8% to 5%.

In reality, Analog Devices’ ROA hasn’t declined. When as-reported accounting distortions are removed, it becomes clear that the company has seen an impressive inflection in profitability.

Uniform ROA has risen from 14% in 2014 to 28% in 2020. This improvement is especially impressive, given that the firm saw a sizable dip due to the ongoing pandemic.

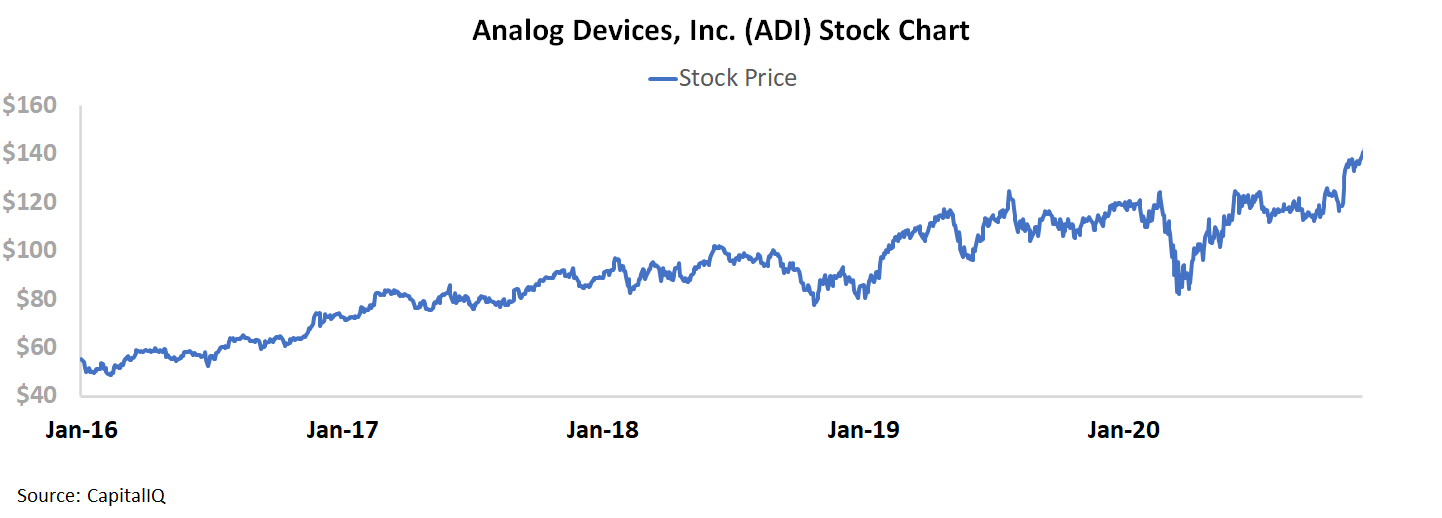

It’s no wonder that over the past five years, Analog Devices has been rewarded handsomely in the stock market for its performance.

Investors seeing this meteoric rise while only looking at as-reported metrics might be baffled by this consistent stock appreciation. An investor with bad data may even view Analog Devices as an attractive short option.

However, when a Uniform Accounting lens is applied to the firm it becomes clear the market is clued into the firm’s turnaround. Only through using Uniform Accounting can investors understand the context of stock movements.

SUMMARY and Analog Devices’ Company Tearsheet

As the Uniform Accounting tearsheet for Analog Devices, Inc. (ADI:USA) highlights, the Uniform P/E trades at 26.7x, which is above the global corporate average valuation levels and its historical average valuations.

High P/Es require high EPS growth to sustain them. In the case of Analog Devices, the company has recently shown a 16% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Analog Devices’ Wall Street analyst-driven forecasts are 17% and 13% EPS growth in 2021 and 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Analog Devices’ $158 stock price. These are often referred to as market embedded expectations.

The company would need to grow its Uniform earnings by 8% per year over the next three years to justify current stock prices. What Wall Street analysts expect for Analog Devices’ earnings growth is above what the current stock market valuation requires in 2021 and 2022.

Furthermore, the company’s earning power is 5x the corporate average. Also, cash flows and cash on hand are almost 2x its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit and dividend risk.

To conclude, Analog Devices’ Uniform earnings growth is in line with its peer averages, and their valuations are also traded in line with its average peers.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research