The risk of this stable telecommunications network is overstated due to its inaccurate high-yield classification

The crossover between investment grade and high-yield bonds provides interesting opportunities for well-versed credit investors. Many companies on the cusp of being classified as investment grade cannot be traded by investment grade portfolios due to their high-yield nature.

Today’s company is a mobile network operator seen as a high yield credit name by the rating agencies.

Below, we show how Uniform Accounting restates financials for a clear credit profile. We also provide the equity tearsheet showing Uniform Accounting-based Performance and Valuation analysis of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Not all data sets lend themselves to simple regression analysis. Some datasets have an issue known as a “spline”. A spline is when in a dataset, there are really two separate sets of data. Because of this, charting and analyzing the data all at once leads to faulty insight and analysis.

To correctly identify and analyze trends for the two datasets, they need to be treated independently.

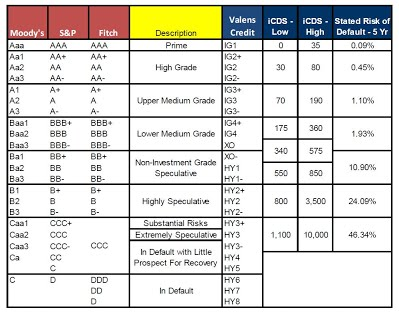

A practical application of this concept can be seen in the risk of defaults for the credit world. Default risk is not linear, as there is a clear spline between the low-risk credits and high-risk. As the risk of default shows here, once you cross from the low-end of investment-grade (Baa/BBB) to the high end of junk bonds (Ba/BB), the default risk shoots up.

The stated five-year risk of default jumps from 2% at the bottom of investment grade credits to 11% for a top quality high-yield debt. As such, crossing from one credit rating group to another is a big signal for investors.

That being said, the reality is businesses on the cusp of each rating classification begin to break the traditional mold. This is why at Valens we don’t just talk about high-yield or investment grade, but also crossover names.

The names include shooting stars (high-yield rising to investment grade) or fallen angels (investment grade falling to high-yield). These names can often trade like an investment grade or a high-yield no matter which side of the demarcation zone they are on, meaning they should be categorized all on their own.

While we recognize this, the rest of the credit markets appear stuck in their ways with the two large classifications. This can sometimes present some pretty interesting opportunities.

One such example is the steady business of United States Cellular Corporation (USM). U.S. Cellular operates the fourth-largest telecommunications network in the United States, with nearly 5 million customers.

U.S. Cellular is currently a Ba1 credit (high-yield), meaning any investment grade portfolio cannot own it. Thus it trades at nearly a 4.0% yield to worst, implying significant credit risk. However, when we look at it from a Uniform Accounting perspective, we can see the true credit risk of the business.

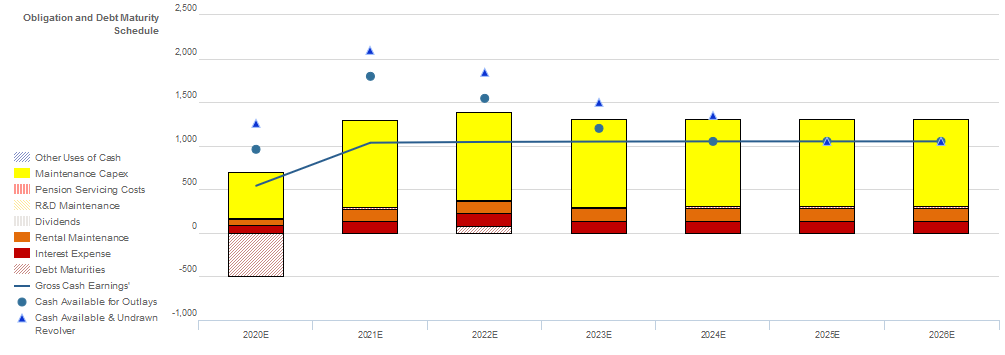

Looking at U.S. Cellular’s Credit Cash Flow Prime (CCFP), it is clear the firm will have no issues servicing its obligations in the near term with cash on hand up until 2023. Even as U.S. Cellular’s cash falls below obligations in 2023, the firm should be able to manage its capex spend to service obligations.

Additionally, U.S. Cellular has a robust 350% recovery rate and a sizable market capitalization, meaning it should have continued access to credit markets to refinance if necessary.

This is why we rate the firm as a safer XO (Baa3) rating. Although it is just one notch higher, it crosses the spline in the data, leading to a large yield difference. This is why the intrinsic yield on the bonds should be closer to 2.3%.

Ultimately, Uniform Accounting and Valens’ classification of bonds helps investors see through the flawed ratings and paint a more accurate picture of U.S. Cellular. After looking at the company’s CCFP, it is clear U.S. Cellular is less of a credit risk than what rating agencies believe.

The firm will be able to meet obligations through 2023 and has significant capex flexibility to meet obligations in the following years.

Only when looking at the Uniform numbers can we understand the real strength of U.S. Cellular’s credit profile.

Tightening of Cash Bond Spreads Likely Going Forward with USM’s Robust Recovery Rate

Cash bond markets are materially overstating USM’s credit risk with a YTW of 3.928% relative to an Intrinsic YTW of 2.258%, while CDS markets are accurately stating risk with a CDS of 153bps relative to an Intrinsic CDS of 159bps.

Furthermore, Moody’s is accurately stating the firm’s fundamental credit risk, with its Ba1 rating only one notch lower than Valens’ XO (Baa3) credit rating.

Fundamental analysis highlights that USM’s cash flows would fall short of operating obligations in each year going forward. However, the combination of the firm’s cash flows and cash on hand after its most recent debt issuance would be able to service all obligations, including debt maturities, through 2022.

Moreover, the firm has material capex flexibility to free up liquidity, and the firm’s robust 350% recovery rate on unsecured debt and moderate market capitalization should allow it to continue to access credit markets to refinance, if necessary.

Incentives Dictate Behavior™ analysis highlights mixed signals for credit holders.

Management’s compensation framework incentivizes them to focus on all three value drivers: top-line growth, margins, and asset efficiency, which should lead to Uniform ROA expansion. Moreover, management members have low change-in-control compensation, suggesting they are not incentivized to seek or accept a buyout or sale of the firm, reducing event risk.

However, management is not punished for overleveraging the balance sheet to drive growth. In addition, management members are not material owners of USM equity relative to their annual compensation, suggesting they may not be well-aligned with shareholders in terms of long-term value creation.

Earnings Call Forensics™ of the firm’s Q2 2020 earnings call (8/7) highlights that management may lack confidence in their prepaid business and their ability to act more community focused. Moreover, they may be exaggerating their 5G capabilities, how valuable their assets are, and the growth opportunities in providing fixed wireless broadband connections.

In addition, management may be concerned about their ability to keep customer churn low, monetize excess capacity, and fund growth. Furthermore, management may have concerns about continued weakness in accessory sales and may be exaggerating their ability to help customers in areas of low service.

Management may also be concerned about their ability to deploy millimeter wave spectrum technology next year and to control cash expenses. Finally, they may lack confidence in the sustainability of increased adjusted operating income.

A robust recovery rate and healthy post-debt issuance liquidity suggest that cash bond markets are overstating credit risk. As such, a tightening of cash bond spreads is likely going forward.

SUMMARY and United States Cellular Corporation Tearsheet

As the Uniform Accounting tearsheet for United States Cellular highlights, the company trades at a -282.5x Uniform P/E, which is far below global corporate average valuation levels and its own historical average valuations.

Negative P/Es imply negative EPS growth. That said, in the case of United States Cellular, the company has recently shown a 2% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, United States Cellular’s Wall Street analyst-driven forecast projects an 22% Uniform EPS contraction in 2020, before a 140% growth in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify United States Cellular’s $29.54 stock price. These are often referred to as market embedded expectations.

The company needs to have its Uniform earnings grow by 87% each year over the next three years to justify current prices. What Wall Street analysts expect for United States Cellular’s earnings growth is below what the current stock market valuation requires in 2020, but above its requirement in 2021.

Furthermore, the company’s earning power is below the corporate average. Also, cash flows and cash on hand are below total obligations—including debt maturities and capex maintenance. Together, this signals average credit risk.

To conclude, United States Cellular’s Uniform earnings growth is below peer averages, and the company is trading far below average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research