Today’s firm appeared to be boxed out of the CRM space, but has executed on a niche risk avoidance strategy

Customer relationship management (CRM) is essential for most companies. As such, there are many firms in the space helping companies manage their relationships with clients. However, the Healthcare sector has its own unique problems most CRM platforms can’t cover. Today’s firm aims to solve those specific problems.

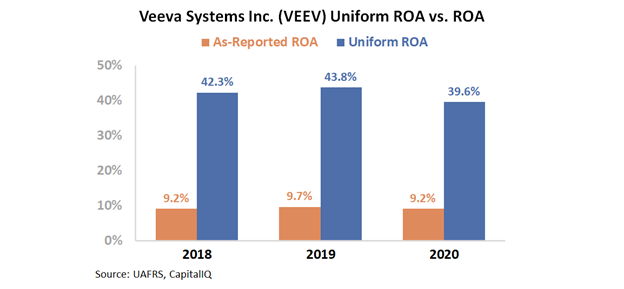

Looking at as-reported numbers might make investors think Healthcare CRM leads to low returns. Digging deeper, we can see the firm has stronger profitability than the market thinks.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

At the end of the day, a company’s most valuable asset is its customers. The entire company should be working to aid the customer, as this is where revenue is coming from.

Until someone invents a way to make money with no customers, most businesses will continue relying on customer relationship management (CRM) systems to manage their customers. The CRM market has been growing rapidly in recent years and is full of some of the biggest technology companies including Salesforce (CRM), Adobe (ADBE), Oracle (ORCL) and Microsoft (MSFT).

Businesses use these offerings to maintain robust sales funnels, perform life cycle analyses, and understand customers’ needs through consolidating and interpreting sales data. They also use them to observe how salespeople are performing and interacting with customers.

Although CRM is necessary in most sectors, it’s especially crucial in Healthcare. Specifically, pharmaceutical sales are subject to heavy regulation that changes frequently. It’s not just a matter of providing good customer service—pharmaceutical sales need to be handled correctly or they can become a massive liability.

Personally, I remember my father, who was a doctor, and my entire family being invited by a pharmaceutical sales rep for a boat trip on Lake George over 25 years ago.

Something like this would never fly today, as the risk/reward profile for pharmaceutical sales has drifted more towards the risk.

Should a concern for impropriety arise when a salesperson goes out, the risk to the drug manufacturer is material. Additionally, with more drug specialization and tailoring to specific needs, being able to track customer needs is essential for the company and regulators.

Salesforce’s stock CRM offerings simply won’t work for the Healthcare industry.

This is where Veeva (VEEV) saw an opportunity. Even with the CRM space being so crowded, Veeva saw the Healthcare sector needed its own service.

Veeva operates under two separate segments, Veeva Commercial Cloud and Veeva Vault. Veeva Commercial Cloud is the firm’s CRM service. This helps customers with CRM, data management, and regulated content and information management.

The firm’s other offering Veeva Vault allows customers to manage large amounts of content and data in one application.

With such useful services offered, it’s surprising to see as-reported metrics so poor for the firm. As-reported ROA appears to be below corporate average levels. Over the past three years, returns have stagnated between 9% and 10%.

However, this depiction of the firm’s performance is not accurate.

GAAP’s treatment of goodwill and intangibles, among other line items, is inflating Veeva’s asset base. This is suppressing as-reported ROA.

Uniform metrics shows the firm’s Uniform ROA has been more than triple as-reported ROA over the past three years.

Veeva has been able to take advantage of the Healthcare space and become a leader in CRM for the sector. Veeva provides its customers with a high return on investment, as is seen by how efficient the company can make its customers.

Veeva users see 90% faster assembly of supplemental history and source find data far quicker than without Veeva software. Additionally, a majority of drugs approved are launched with Veeva’s CRM, showing how widespread it is.

Veeva’s widespread usage is paired with its powerful subscription model. This provides recurring and regular revenue for the firm.

The company’s subscription model has driven a Uniform ROA between 40% and 44% over the past three years.

Veeva’s real returns are closer to what you might expect from such a unique and in-demand service.

Uniform Accounting is able to show how Veeva has taken advantage of its niche in the Healthcare space. Through its subscription model, the firm has been able to sustain high returns for years. As the Healthcare sector continues to grow, Veeva may be a stock to follow.

SUMMARY and Veeva Systems Inc. Tearsheet

As the Uniform Accounting tearsheet for Veeva Systems Inc. (VEEV:USA) highlights, the Uniform P/E trades at 84.0x, which is above the global corporate average valuation levels and its historical average valuations.

High P/Es require high EPS growth to sustain them. In the case of Veeva Systems, the company has recently shown a 13% growth in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Veeva Systems’ Wall Street analyst-driven forecast is a 13% and a 7% EPS growth in 2021 and 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Veeva Systems’ $264 stock price. These are often referred to as market embedded expectations.

The company needs to grow Uniform earnings by 37% each year over the next three years to justify current stock prices. What Wall Street analysts expect for Veeva Systems’ earnings growth is below what the current stock market valuation requires in 2021 and 2022.

Furthermore, the company’s earning power is 7x the long-run corporate averages. Additionally, cash flows and cash on hand are 11x its total obligations—including debt maturities and capex maintenance. Altogether, these signals a low credit risk.

To conclude, Veeva Systems’ Uniform earnings growth is above peer averages. Also, the company is trading in line with its peer average valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research