This company is driving Frontier Communications out of business

Frontier Communications rebranded in 2008, and since then they have been focused on a market that no one else wants. They have been focusing on rolling up the local phone companies throughout the United States.

This is a dying business. Frontier has been rewarded for the company’s trouble by seeing the stock drop from above $230 in mid 2007 to $1 today. A cool 99.5% drop in the company’s stock price.

Frontier’s goal hasn’t just been to buy up a declining business and hope for the best through cost cutting. They’ve been rolling up these businesses and focus on selling incremental services to their customers. In particular their business customers. Solutions like Voice over IP (VoIP), managed Wi-Fi and IT solutions, Ethernet services, among others.

But they’ve had limited success with getting clients interested in those other services, because there are better pure-play offerings for all those other services. And because of that, Frontier continues to see their customer base and revenue shrink. It’s because of this that the company’s 2020 bonds currently trade at 55 cents on the dollar. It’s also the reason their 2024 bonds, due in just 5 years have a 29% yield to worst, and are trading at 48 cents on the dollar.

One of those pure-play companies that Frontier is losing their shirt to is Vonage. Vonage started in 2000 as a VoIP company, and you may remember them best for their own failed capital market event, their IPO which was heavily sold to customers, and performed poorly post-public offering.

But Vonage has evolved significantly since then. Vonage offers a range of solutions to businesses around communication and connectivity that meet the needs, and more, that Frontier is trying to offer. And they have built their business from the ground up, in a systematic and connected fashion that reduces the friction those same clients might have with the amalgamation that Frontier offers.

The market has rewarded Vonage’s successful transformation, with the stock up 83% since 2016.

With the stock already having moved higher, investors may think the move has already happened, and the market already figured out what has happened. On the other hand, our Uniform Accounting analysis shows market expectations are still not excessive, and there may be more fundamental room for the stock to run. Not only are the fundamentals strong, management is showing confidence about fundamental drivers that may enable them to continue to exceed market expectations.

The 2020 Bull-Bear Market Forecast – Event next Friday in Chicago

We regularly get questions from clients in terms of where we are in the macro cycle, especially considering our Market Phase Cycle™ macro analysis has been spot on so many times over the past six years.

On next Friday, there are a limited seats available for an update I’m giving in Chicago on our macro outlook.

The 2020 Bull-Bear Market Forecast.

The event is on October 25th, at 9am CST, in downtown Chicago at the Daley building at DePaul’s Driehaus College of Commerce.

There are limited seats available, so please only register if you’re sure of your availability.

To register, and read more, click here.

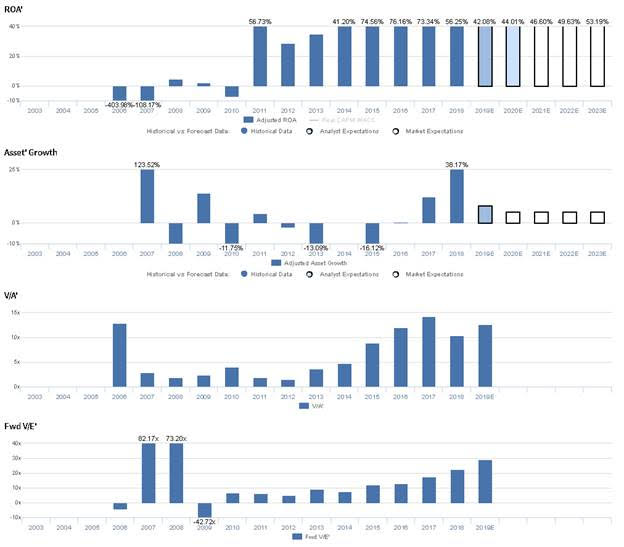

Market expectations are for Uniform ROA decline, but management is confident about growth, cloud adoption, and product offerings

VG currently trades above recent averages relative to UAFRS-based (Uniform) Earnings, with a 29.0x Uniform P/E. However, even at these levels, the market is pricing in expectations for Uniform ROA to decline from 56% in 2018 to 53% in 2023, accompanied by 5% Uniform Asset growth going forward.

However, analysts have more bearish expectations, projecting Uniform ROA to fall to 44% through 2020, accompanied by 8% Uniform Asset growth.

Vonage has seen volatile but improving profitability, with Uniform ROA improving from substantially negative levels prior to 2008 to a peak of 56% in 2011. Thereafter, Uniform ROA fell to 29% in 2012, before rising to an all-time high of 76% in 2016, and falling to 56% in 2018. Meanwhile, VG has seen volatile Uniform Asset growth, positive in six of the past 12 years and ranging from -16% to 38%.

Performance Drivers – Sales, Margins, and Turns

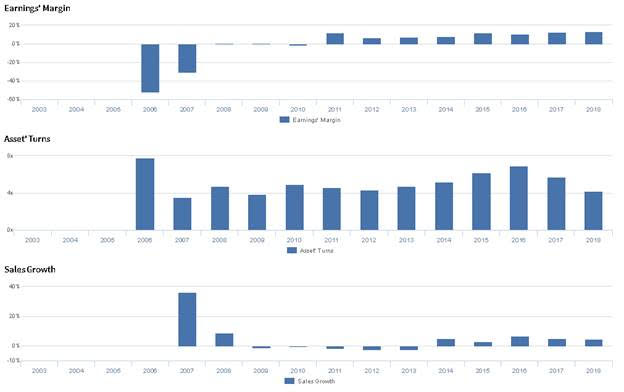

Overall improvements in Uniform ROA have been driven primarily by improvements in Uniform Earnings Margin, while recent compression has been driven by Uniform Asset Turns. Uniform Earnings Margin improved from -52% in 2006 to 12% in 2011, before falling to 7% in 2012 and subsequently improving to 14% in 2018. Meanwhile, Uniform Asset Turns initially fell from 7.8x in 2006 to 3.5x in 2007 before improving to peak 6.9x levels in 2016 and declining back to 4.2x in 2018. At current valuations, markets are pricing in expectations for Uniform Margins to remain stable, coupled with continued declines in Uniform Asset Turns.

Earnings Call Forensics

Valens’ qualitative analysis of the firm’s Q2 2019 earnings call highlights that management is confident their Tel Aviv engineering team is focused on leveraging AI to deliver customer value and that growth will continue to improve. Furthermore, they are confident larger companies are moving to the cloud, and they are confident globalization is driving increased interest in their integrated contract center product.

However, they may be concerned about the sustainability of their consumer subscriber lines and about further declines in gross margin. Furthermore, they may lack confidence in their ability to minimize their leverage.

UAFRS VS As-Reported

Uniform Accounting metrics also highlight a significantly different fundamental picture for VG than as-reported metrics reflect. As-reported metrics can lead investors to view a company to be dramatically stronger or weaker than real operating fundamentals highlight. Understanding where these distortions occur can help explain why market expectations for the company may be divergent.

As-reported metrics significantly understate VG’s profitability. For example, as-reported ROA for VG was near 4% levels in 2018, materially lower than Uniform ROA of 59%, making VG appear to be a much weaker business than real economic metrics highlight. Moreover, as-reported ROA has improved from -7% to 56% from 2010 to 2018, while as-reported ROA has fallen from 21% to 4% over the same period, directionally distorting investors’ perception of the firm’s historical profitability.

Today’s Tearsheet

Today’s tearsheet is for Nestle. Nestle trades at a premium to market average valuations. However, at current valuations, the market is pricing in Uniform EPS growth to be in line with recent trend and with near-term forecast Uniform EPS growth. The company’s earnings growth is forecast to be above peers, and they trade at the lower end of peer valuations, signaling the strength of the company’s fundamentals.

Regards,

Joel Litman

Chief Investment Strategist