ViacomCBS shows competing in ‘red oceans’ is sometimes the right call

When introducing new products to a market, companies have to first strategize where they are expanding.

Companies can try to penetrate highly competitive markets with stiff players, or take the alternative route in expanding into markets with little to no competition at all.

Despite what most professors preach, some of the best companies often take the former option.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

When companies are looking to expand and penetrate new markets, they often base their decisions off of “red oceans” and “blue oceans.”

Simply put, red oceans are highly competitive markets, and blue oceans are uncharted territories.

Business school professors often tell students to go after the blue ocean for opportunities since there is no competition.

However, the reality is that most companies are perpetually focused on the red oceans of competitive waters.

The past six months of streaming headlines revolving around legacy content providers is a classic example of this idea.

This industry is saturated with giants competing with each other to gain further market share and dominate the space.

Specifically, after Netflix (NFLX) created the streaming market when it first entered, it has faced fierce battles from other following giants such as Amazon (AMZN), Disney (DIS), and WarnerMedia’s HBOMax.

This has led to many takes on winners and losers. It has also led to many failed and retired strategies that have allowed for massive mergers and acquisitions.

Take the recent merger of WarnerMedia and Discovery for example, amongst many others.

In fact, anyone who watched the Super Bowl earlier this year was probably reminded of all the other media groups’ efforts to rebrand their current streaming platform.

An example of this event would be ViacomCBS (VIAC) and its work to rebrand its CBS All Access service to Paramount+ last March 2021.

Considering its great efforts, investors might assume that CBS was previously unsuccessful with its streaming services and that is why the company decided to rebrand its name.

To gain better insight into these decisions, let’s take a look at the numbers.

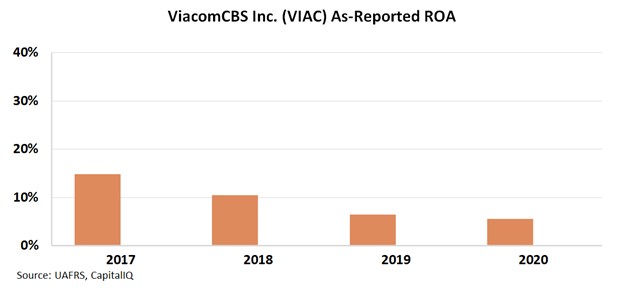

By looking at ViacomCBS’s as-reported metrics, investors can see the numbers lined up with the thought that CBS streaming services were not doing well.

Specifically, the company’s as-reported ROA levels faded from all-time highs of 15% in 2017 to 5+ year lows of 6% in 2020.

See for yourself below.

However, this is actually not an accurate picture of ViacomCBS’s profitability.

The company is not generating returns below the U.S. corporate average. In reality, ViacomCBS is posting robust returns.

For example, the company’s returns in 2017 were at 33% levels, and then faded to just 29% levels in 2020.

The Uniform Accounting data highlights ViacomCBS’s decision to rebrand CBS did not come from a place of desperation. It actually came from a position of strength.

ROA levels were still near the highest levels, and the company was just trying to concentrate on continuing to compete.

SUMMARY and ViacomCBS Inc. Tearsheet

As the Uniform Accounting tearsheet for ViacomCBS Inc. (VIAC:USA) highlights, the Uniform P/E trades at 13.8x, which is below the global corporate average of 23.7x, but around its own historical average of 13.0x.

Low P/Es require low EPS growth to sustain them. In the case of ViacomCBS, the company has recently shown a 12% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, ViacomCBS’s Wall Street analyst-driven forecast is a 7% EPS shrinkage in 2021 and 2% EPS growth in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify ViacomCBS’s $40 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink 8% annually over the next three years. What Wall Street analysts expect for ViacomCBS’s earnings growth is in line with what the current stock market valuation requires in 2021 and above that requirement in 2022.

Furthermore, the company’s earning power is 5x above the long-run corporate average. Also, cash flows and cash on hand are 3x its total obligations—including debt maturities, capex maintenance, and dividends. Meanwhile, intrinsic credit risk is 120bps above the risk-free rate. All in all, this signals a low dividend and moderate credit risk.

To conclude, ViacomCBS’s Uniform earnings growth is above its peer averages, and the company is trading in line with its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research