Data is the real digital currency, and today’s company has some of the best data on the planet

Data and data analytics have become essential tools for all modern companies.

No place is this more obvious than in the insurance industry, where a company’s ability to analyze data directly connects to its profitability.

Today’s company helps other companies make better investment decisions by leveraging innovative data analytics.

When looking through a Uniform Accounting lens, it becomes clear the surge in opportunity within this space has not gone unnoticed.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

The insurance industry is one of the only industries in the world where a company does not know its cost of goods sold when the products are sold.

When an insurance company sells a policy, it is not sure what it will have to pay out to the consumer.

Instead, it has to rely on projections for its COGS. In the past, insurance companies used the historical loss ratio—the percentage of the premiums collected that is paid out as insurance claims—to determine what the future loss ratio would be.

However, in an increasingly data driven world, complex modeling is being used to determine expected loss ratios and to determine the insurance risk right at the point of sale.

Before they even sell a policy, insurance companies can use data to predict the likelihood of having to pay a claim.

Since an insurance company’s profitability directly depends on its loss ratios, leveraging data to better price insurance risk is extremely important.

The data and data analytics of an insurance company drives its profitability, and having a better predictive model than the competition leads to meaningfully better performance.

Moreover, the insurance industry is just one example of the power of data and data analytics—there are countless other industries that can leverage this technology to improve investment decisions and manage risk.

Enter Verisk Analytics (VRSK), one of the biggest platforms for helping insurance companies, energy companies, and financial service companies make sense of their data to improve decision making.

Verisk Analytics uses proprietary models and industry expertise to provide predictive analytics. They offer a range of services such as improved underwriting models, fraud detection, and natural disaster prediction.

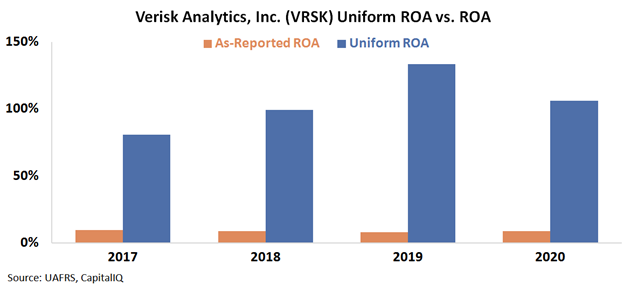

One would assume that a cutting edge data company at the forefront of innovation would generate above average profitability, but looking at as-reported results , Verisk appears to be generating lackluster returns.

The company’s return on assets (ROA) stayed below 10% from 2017 to 2020, which is extremely underwhelming for a cutting edge, asset light technology company.

See for yourself below.

However, Verisk Analytics is far more profitable than as reported metrics would indicate. As-reported financial metrics dramatically overstate the company’s net asset base, due to the impact of goodwill and intangibles, which understates its ROA.

In reality, the company is not generating average profitability, and Instead it is delivering nearly triple digit returns.

Specifically, Verisk Analytics had a Uniform ROA of 100% or more in 2018, 2019, and 2020.

This 100%+ Uniform ROA is the third highest of its direct 20 company peer group.

These discrepancies are material, and show how uniform accounting metrics are crucial to understanding the true value of a company.

On an as-reported basis, investors would be led to view Verisk Analytics as an uninspiring, low return business.

However, with Uniform Accounting metrics investors can see the company’s strong profitability.

SUMMARY and Verisk Analytics, Inc. Tearsheet

As the Uniform Accounting tearsheet for Verisk Analytics, Inc. (VRSK:USA) highlights, the Uniform P/E trades at 33.4x, which is above the global corporate average of 23.7x, but around its own historical average of 31.6x.

High P/Es require high EPS growth to sustain them. In the case of Verisk, the company has recently shown an 18% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Verisk’s Wall Street analyst-driven forecast is a 6% shrinkage in 2021 and 10% EPS growth in 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Verisk’s $175 stock price. These are often referred to as market embedded expectations.

The company needs to have Uniform earnings grow 11% per year over the next three years in order to justify current stock prices. What Wall Street analysts expect for Verisk’s earnings growth is below what the current stock market valuation requires in 2021, but in line with that requirement in 2022.

Furthermore, the company’s earning power is 18x the long-run corporate average. Also, cash flows and cash on hand are slightly above its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals a low credit and dividend risk.

To conclude, Verisk’s Uniform earnings growth is below its peer averages while the company is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research