War won’t stand in the way of this company’s growth

The Israel-Hamas war has led to a variety of Israel-based companies being sold off. Investors fearing the crisis will affect these companies have slashed their share prices recently. This sell-off could be reasonable for some companies – they could have genuine supply-chain or operational disruptions.

However, there are others that are being grossly oversold.

InMode (INMD) looks like one of them.

Established in 2008 in Israel, InMode is a company focused on aesthetic beauty, known for developing and marketing medical aesthetic products that leverage its unique radiofrequency technologies.

The market thinks the war could hurt several parts of InMode’s business. However, InMode has been vastly profitable recently and analysts expect it to continue this trend.

Thus, InMode showed up on our screen. The company makes a great FA Alpha 50 name due to its potential for high returns and low expectations from the market.

Investor Essentials Daily:

Tuesday FA Alpha 50

Powered by Valens Research

Investors weren’t sure what to expect from Israeli companies when the Israel-Hamas war launched in early October.

Fears of potential supply-chain disruptions or a pullback in demand sent the Tel Aviv 125 Index down as much as 15% in the weeks after the war commenced.

Some companies were hit even harder… including InMode (INMD).

Established in 2008 in Israel, InMode is a company focused on aesthetic beauty, known for developing and marketing medical aesthetic products that leverage its unique radiofrequency technologies.

The company caters to a global market, including the U.S., offering a variety of treatments for skin, face, body, hair removal, and women’s health through its advanced equipment.

As a result of the Israel-Hamas conflict, InMode saw its shares fall 35% between the 10th of October and the 1st of November.

However, InMode is not concerned about it.

First, over 80% of InMode’s revenue is generated from the U.S. and Europe, with only about 1% coming from Israel, which has been affected by conflict. The company’s leadership has assured investors that the conflict will not majorly disrupt production processes.

Second, InMode is an essential player in a growing industry. The rapid expansion of the medical aesthetics market and growing interest in medical aesthetic treatments mean the company will see more demand going forward.

Moreover, InMode has carved out a unique market space for itself, sitting between traditional plastic surgery and laser treatments, an area where it faces little competition. This positions InMode with a significant competitive advantage in its field.

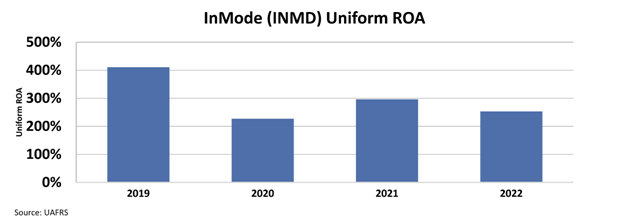

This has allowed InMode to generate outstanding returns in recent years. The company’s Uniform return on assets (“ROA”) has been above 200% in each of the last four years.

InMode’s management team isn’t worried that this will get worse. Not only are most of the company’s customers international, but it already has three quarters worth of inventory ready to sell. Plus, it doesn’t expect any production issues related to the war.

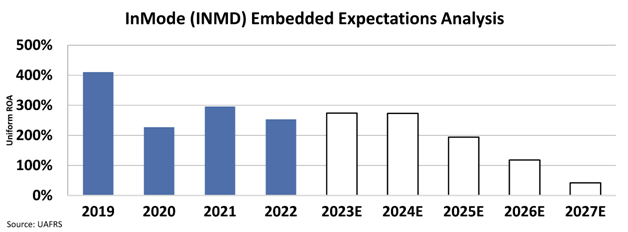

And yet, the market fails to recognize this opportunity. We can see this through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the market expects the company’s ROA to fall below 45%, assuming the demand will collapse.

Given the past profitability of the company, its minor relation to Israel, and its strong growth potential, these expectations seem overly pessimistic.

InMode has substantial potential to scale its operations and continue growing.

That is why InMode showed up on our screen. The company makes a great FA Alpha 50 name due to its potential for high returns and low expectations from the market.

Throughout financial market history, many of the world’s most successful investors have been candid in their belief that Generally Accepted Accounting Principles (“GAAP”) distort economic reality.

Warren Buffett, for example, once said investors should “concentrate on the world of companies, not arcane accounting mathematics.”

Investors who neglect the very real issues with as-reported accounting can find themselves caught up in investing with the crowd, blindly following hot “themes” without a thorough grasp of how to understand the businesses in question.

The only true way to focus on the “world of companies,” as Buffett suggests investors do, is to present a clear picture of how a business operates, something that can only be done by adjusting financial statements to reflect the arbitrary nature of certain accounting rules that leave much to discretion.

The world’s best investors understand the need to make these adjustments, which allows them to focus not on picking out the most popular companies but rather on looking for great names in sleepy areas that the market isn’t paying much attention to. From there, the goal is to then identify quality companies with significant growth potential at reasonable prices.

That’s exactly what we’ve set out to do with the FA Alpha, our monthly list of 50 companies that rank at the top for quality, high growth, and low valuations.

This list has outperformed the market by 300 basis points per year for over 20 years now, effectively doubling the performance of the market by focusing on the real fundamentals and valuations of companies with our proprietary Uniform Accounting framework.

See for yourself below.

To see the other 49 names on the list, click here.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research