This data storage firm could have saved itself from being an ‘ice cube’ by looking at the correct accounting data

Data storage has become increasingly complex in recent years. Today, a simple smartphone has more power and storage than some of the most complex computers in the world decades ago.

Today’s company is a hard disk drive manufacturer and data storage firm. The firm has struggled to adapt to changing technology in the storage space.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

We’ll sometimes call a company a melting ‘ice cube’ when its core business is slowly shrinking away with no clear solution. Generally, the company will trade at low multiples as investors price in this decline. When management teams realize they’re guiding an ice cube, they have two options to preserve shareholder value.

The first option is to let the core business fade away. Here, management should actively return cash to shareholders while sustaining the business as long as possible. Returning cash often comes in the form of stock buybacks or share repurchases, since there are few investment opportunities.

The second option is to innovate, breathing new life into the business. This means investing in a new end market through either R&D or M&A.

Western Digital (WDC), a hard disk drive (HDD) maker, is a classic example of this. HDDs are the old-school hard drives you typically think of—loud, warm, and with spinning parts. HDDs are slowly being replaced by solid state drives (SSD). SSDs have no platters or arms, storing data in integrated circuits much like a large flash drive.

SSDs are much faster and more efficient than HDDs, rendering the HDDs to legacy technology status. While HDDs are cheaper at the moment, SSDs have seen their price steadily drop in recent years.

As-reported returns show Western Digital as a clear example of a melting ice cube. The HDD market appears to be in terminal decline, taking legacy providers of this technology down with it.

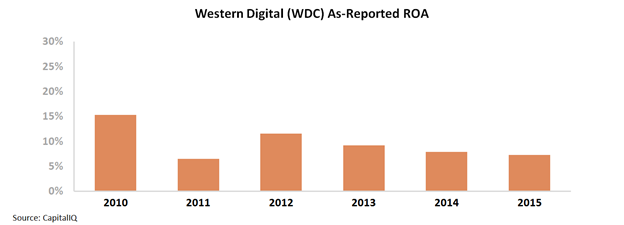

Western Digital’s as-reported return on assets (ROA) was on a strong decline from 2010 to 2015. As-reported ROA fell from 15% in 2010 to 7% in 2015.

Western Digital saw these declining returns and panicked, buying SSD maker Sandisk in 2015. This was an effort to get out of the legacy HDD space in which it appeared to be struggling.

However, this picture of Western Digital’s performance was not accurate. This is due to distortions in as-reported accounting. These include the treatment of goodwill and other distortions. Wall Street was missing the firm’s profitability.

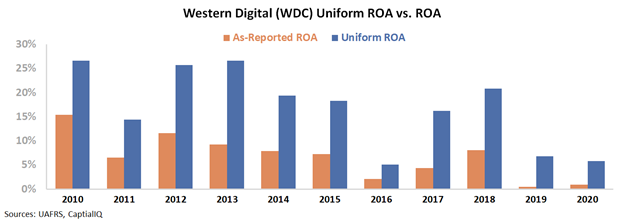

Uniform ROA was 27% in 2010 and only fell to 18% in 2015. There was no doubt the business was not as strong as it once was, but as-reported ROA exaggerated the decline.

Western Digital was still a high performing business before the Sandisk acquisition.

The firm saw a surge in demand following the acquisition until 2018. Western Digital then overinvested in its inventory to try and fuel this growth, but demand did not follow suit.

Uniform ROA thus subsequently cratered from a high of 21% in 2018, to 6% in fiscal year 2020. If the company had been looking at the right Uniform numbers all along, it would have seen its healthy Uniform ROA before the 2015 acquisition.

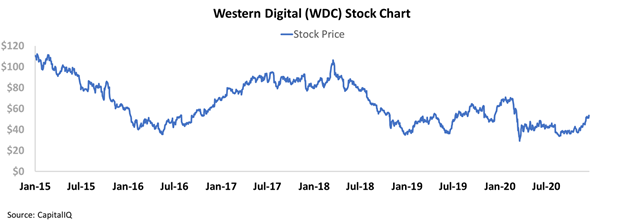

In response to this misstep, Western Digital has seen its stock fall from around $120 in 2015 to just $60 today.

Without Uniform Accounting, investors would miss the whole story of this HDD and SSD provider. They might see Western Digital as a firm that made an unsuccessful acquisition to try and stave off declining returns. Instead, the firm made an unnecessary purchase, when it should have focused on the returns of its core business.

Ultimately, Western Digital may have been able to prevent its severe stock price declines if it had been using Uniform Accounting. This story highlights the importance of looking at the right numbers before making business decisions.

SUMMARY and Western Digital’s Company Tearsheet

As the Uniform Accounting tearsheet for Western Digital Corporation (WDC:USA) highlights, the Uniform P/E trades at 22.6x, which is around the global corporate average valuation levels and its own historical average valuations.

Average P/Es require average EPS growth to sustain them. In the case of Western Digital, the company has recently shown an 18% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Western Digital’s Wall Street analyst-driven forecast is a 27% EPS decline in 2021 and a 165% EPS growth in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Western Digital’s $53 stock price. These are often referred to as market embedded expectations.

The company would need to grow its Uniform earnings by 2% per year over the next three years to justify current stock prices. What Wall Street analysts expect for Western Digital’s earnings growth is below the valuation requirements in 2021, but above that requirement in 2022.

Furthermore, the company’s earning power is around the corporate average. In addition, its intrinsic credit risk is 100bps above the risk-free rate. Together, this signals average credit risk.

To conclude, Western Digital’s Uniform earnings growth is below its peer averages, but the company is trading above peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research