This week’s market chaos may have revealed the winner of this Wall Street giants’ feud

When one of the greatest macro and thematic traders ever tells you that your big macroeconomic bet is wrong, you probably want to pay attention.

Blackrock will never publicly tell George Soros he was right. But Monday’s market chaos, stemming from the realization that the Chinese real estate market is overexposed to default, made it clear that Soros had a point when he told Blackrock to stay away from Xi Jinping’s China.

Let’s use Uniform Accounting to audit George Soros’ portfolio, to see if his own stark avoidance of Chinese equities has set him up for success.

In addition to examining the portfolio, we’re including a deeper look into the fund’s largest current holding, providing you with the current Uniform Accounting Performance and Valuation Tearsheet for that company.

Investor Essentials Daily:

Friday Uniform Portfolio Analytics

Powered by Valens Research

On Monday, the market opened significantly lower as news sites were flooded by headlines highlighting bad Chinese housing debt.

Our longtime readers may find connections to many of the themes we frequently discuss. Chiefly, debt drives markets. Also, an unfavorably regulated economy comes with high investment risks to anyone hoping to ride the Chinese growth wave.

And yet, American investment dollars continue to pour into China. Every investor seems to have an opinion on where China is going over the long term.

A spurt of gasoline got added to the already fiery debate when the infamous activist investor George Soros published an opinion piece in the Wall Street Journal early this month putting Blackrock’s China plans under the microscope.

Blackrock, the largest asset manager in the world with $8.4 trillion in assets under management, recently announced a massive bet on China. Just weeks after recommending investors triple their China allocation, the firm launched a set of brand new China-only mutual funds.

In fact, Blackrock is now the only entirely-foreign-owned mutual fund provider in China. This is significant because foreign actors typically need to partner with a Chinese firm to do business in China. While Blackrock’s skirting of this rule gives them total ownership over their Chinese dealings, it also exposes them to more risk.

In his piece, Soros made it clear that these risks are plentiful. He says President Xi Jinping doesn’t view public markets as a protected tool for growth, and will intervene in ways that put investor capital at risk.

This doesn’t just concern foreign investors like Blackrock and those who buy into the new funds, but also Chinese investors. For example, innovation that upsets the status quo in a way that could be unfavorable to major state-run companies is frequently stopped dead in its tracks by Chinese government officials.

Ultimately, all these matter to Blackrock not just because of direct investment risks, but it also darkens the macroeconomic Chinese outlook.

Blackrock fired back at Soros, citing increased trade between the United States and China.

China also made its voice heard. The Beijing Global Times, a state-run media enterprise, called Soros a “global economic terrorist” for his words about Blackrock’s strategy.

But as Soros points out, the top-of-mind political concern for Xi comes with the October 2022 20th Party Congress, where he will either step into an unprecedented third term (after abolishing term limits three years ago), or he will be replaced. Soros stipulates that Xi is trying to erode the power of anyone who could realistically challenge him, namely influential Chinese businessmen.

Said otherwise, Soros believes investor confidence in China is grossly irrational.

He has learned to identify situations like these over a storied 65-year career in finance. It was using that same understanding of how and when markets are irrational, that they can build on their core beliefs, seeing confirmation bias and groupthink fuel markets in one direction.

Then inevitably, when the data becomes too impossible to ignore, the markets can react aggressively in the opposite direction in an effort to normalize, which generally overshoots.

He has coined a term for this: Reflexivity. The focus of reflexivity is the feedback loops that occur in investor biases until they are broken.

His belief in this framework is what fueled his confidence in his trade to break the Bank of England in 1992, where he bet against the pound believing it was overvalued. He understood that investors’ belief that the Bank would stand behind the peg had caused the overvalued peg to become too extended. By pushing on it, he eventually broke it, causing a windfall.

His deep understanding of macroeconomic undercurrents has also enabled his funds to return investors roughly 20% each year since he opened his door as a money manager in the 1970s.

Looking at the positions held by Soros Fund Management, you can clearly see Soros’ avoidance of Chinese companies despite the fund’s global strategy. This is in contrast to most of the funds we review in this Friday portfolio review series, which all have some degree of Chinese exposure.

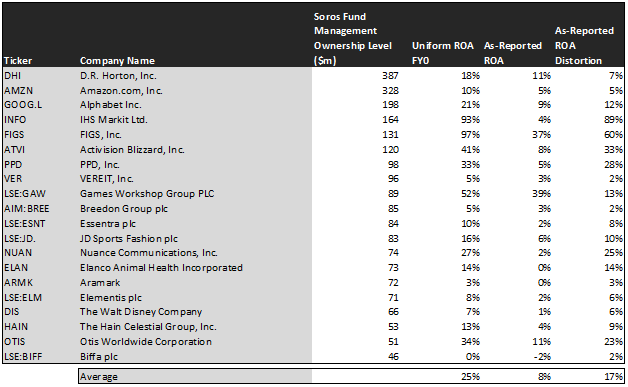

Using Uniform Accounting, we’ve conducted a detailed portfolio review of Soros Fund Management’s 20 largest holdings. Take a look below:

Soros’ fund invests in more than just stocks, but also ETFs and private companies. The 20 holdings listed above are those Soros’ largest holdings that Valens is able to apply its Uniform accounting adjustments.

Those looking only at the as-reported financials of these companies would see an average return on assets of only 8%. While this is above the cost of capital, it wouldn’t catch anyone’s interest.

This would be a very distorted way of looking at not just this portfolio, but finance and investing as a whole. The Generally Accepted Accounting Principles (GAAP) and the International Financial Reporting Standards (IFRS) are full of nonsensical rules that make companies incomparable.

Our team at Valens makes over 100 adjustments to the financial statements so the numbers you see actually represent economic profitability.

Once we make these adjustments, we see that Uniform ROA isn’t a lackluster 8%, but actually a robust 25%, double the U.S. corporate average.

For example, take a look at research firm IHS Markit (INFO), of which Soros controls $164 million. Most would see ROAs of only 4%, which would suggest the investment dollars that finance the company’s operations cost more than the resulting profits. In reality, the company’s asset base is overinflated with goodwill and intangibles, making it appear far less profitable than it really is, and actually boasts fantastic 93% Uniform ROAs.

Similarly, look at the videogame making Activision (ATVI). While most investors would see lackluster ROAs of 8%, the use of Uniform metrics shows robust 41% ROAs.

However, to find alpha in the marketplace, investors need to do more than just find strong performers. It needs to find strong performers that the audience hasn’t yet discovered: Companies that are priced to perform far worse than can be reasonably expected.

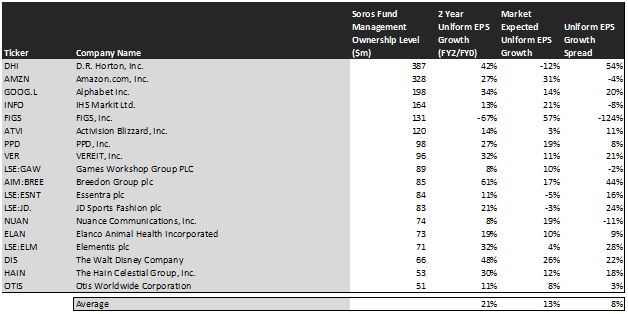

For this, we can use our embedded expectations analysis. Take a look:

This chart shows three interesting data points:

– The first datapoint is what Uniform earnings growth is forecast to be over the next two years, when we take consensus Wall Street estimates and we convert them to the Uniform Accounting framework. This represents the Uniform earnings growth the company is likely to have, the next two years.

– The second datapoint is what the market thinks Uniform earnings growth is going to be for the next two years. Here, we are showing how much the company needs to grow Uniform earnings in the next 2 years to justify the current stock price of the company. If you’ve been reading our daily and our reports for a while, you’ll be familiar with the term embedded expectations. This is the market’s embedded expectations for Uniform earnings growth.

– The final datapoint is the spread between how much the company’s Uniform earnings could grow if the Uniform Accounting adjusted earnings estimates are right, and what the market expects Uniform earnings growth to be.

Based on current valuations, the market is expecting these companies to grow their earnings base by 13% over the next two years. Analysts, however, see earnings growing by 21% over the same period.

Although not a massive dislocation, this shows that the fund is modestly undervalued.

For example, take a look at homebuilder D.R. Horton (DHI), of which Soros owns $387 million. While the market is pricing in earnings to shrink by 12%, analysts are expecting earnings to grow by nearly 50%, in part due to the massive backlog it is experiencing.

The effect can go the other direction as well. Take a look at healthcare apparel maker Figs (FIGS), which is priced to expand its earnings by 57% over the next two years. Analysts, however, have a more bearish view, and expect earnings to shrink by 67%.

The most notable feature of this portfolio is its lack of Chinese exposure. Soros’s deep understanding of macroeconomic undercurrents has led him to avoid doing business with the second largest economy on earth.

That sort of conviction is what investors need in order to thrive in this environment. Macroeconomic research, however, takes time and a dedicated workforce. Some hedge funds have the wherewithal to build their own macroeconomic research team. But they do everything in their power to keep that research away from the general public.

Unfortunately, most funds, financial advisors, and retail investors don’t have those resources. Here at Valens, we’ve done the research for you.

That is why hedge funds and even the Pentagon turn to Valens for our deep macroeconomic insights. We pack those insights into our flagship macroeconomic report: The Market Phase Cycle.

It is the most detailed, accurate, and actionable macroeconomic research report in circulation. Learn more about how to get access here.

SUMMARY and D.R. Horton, Inc. Tearsheet

As Soros Fund Management’s largest individual stock holdings, we’re highlighting D.R. Horton, Inc.’s tearsheet today.

As the Uniform Accounting tearsheet for D.R. Horton, Inc. (DHI:USA) highlights, its Uniform P/E trades at 7.4x Uniform P/E, which is below the global corporate average of 23.7x and its historical P/E of 8.7x.

Low P/Es require low, and even negative, EPS growth to sustain them. In the case of D.R. Horton, the company has recently shown a 45% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for International Financial Reporting Standards (IFRS) earnings and convert them to Uniform earnings forecasts. When we do this, D.R. Horton’s sell-side analyst-driven forecast is for EPS to grow by 77% and 14% in 2021 and 2022, respectively.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify D.R. Horton’s $91 stock price. These are often referred to as market-embedded expectations.

The company’s earnings power is 3x the long-run corporate averages. Furthermore, cash flows are around 6x total obligations—including debt maturities, capex maintenance, and dividends. Additionally, intrinsic credit risk is 40bps above the risk-free rate. Together, these signal low credit and dividend risks.

Lastly, D.R Horton’s Uniform earnings growth is above its peer averages, but the company is trading in line with its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research