With backup power getting more important by the day, investors and rating agencies think this battery maker is riskier than it is

100 years ago, electric power was a luxury for many city or suburban dwellers to power lights. Today, constant access to power is a necessity as employees work from home, students learn from home, and more.

This firm’s services are indispensable as the backbone to providing constant energy as the power grid goes green.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Computers and connectivity have revolutionized the workplace. This has caused work to move from analog to digital to the cloud in a matter of years.

As digital infrastructure has become a necessity in the workplace, it cannot afford to shut down or lose power.

Whether it’s data centers hosting billions of transactions a second or broadband home WiFi for individuals across the globe, the global economy simply needs these systems to function.

“Always on” systems are a robust technical challenge. As more systems and devices are connected through the internet, the more reliant humans become on the entire network.

Additionally, disruptive power solutions such as renewable power have become more developed and widely used over the years.

While these alternative power solutions are a positive impact on our environment, wind and solar power do not generate steady output, requiring batteries to guarantee the lights stay on.

This means battery storage systems are becoming a vital part of the smart grid. Any firms offering battery storage solutions will see surging demand going forward.

One company that will be at the forefront of this surge in demand is EnerSys (ENS).

EnerSys manufactures and sells back-up battery power solutions. The company splits its efforts between two main battery product lines.

The first of these are standalone mobile batteries designed to go into electric vehicles. EnerSys also makes battery bank solutions designed to hold overflow power from solar and wind.

Despite its valuable products and potential for solid growth going forward, credit rating agencies are skittish when rating EnerSys’s debt. Specifically, Moody’s gives EnerSys a non-investment grade speculative Ba2 rating, with the implied assumption of a 25%+ risk of default over the next five years.

This seems overly pessimistic given the potential for booming demand in the industry.

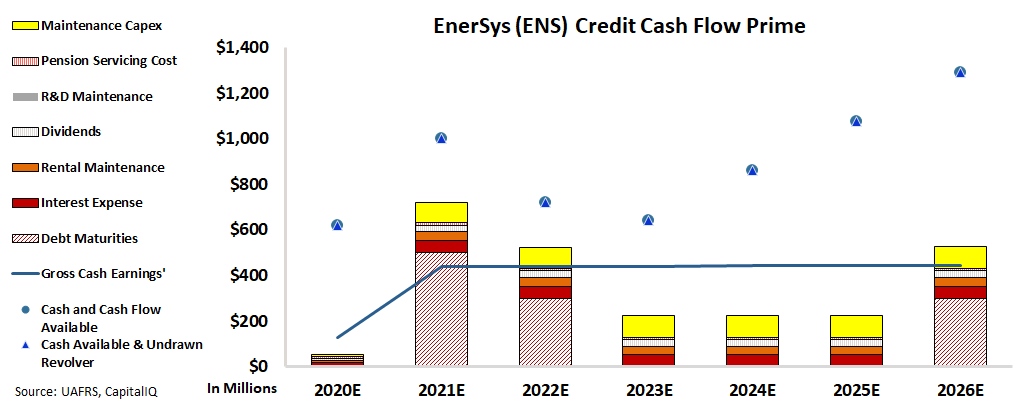

Our Credit Cash Flow Prime (CCFP) analysis is able to get to the heart of the firm’s true credit risk and shows a different picture than the rating agencies bearish outlook.

In the below chart, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

On a fundamental level, EnerSys gross cashing earnings are strong enough to match all operating obligations for the company, despite facing more challenges in 2021. When including debt maturities over the next five years, the firm’s cash flows do fall short of obligations in a few years. However, Enersys has ample access to cash and the undrawn revolver.

As a result of this massive cash on hand and strong cash flows EnerSys has a much safer credit profile than rating agencies suspect.

Rather than a name in distress, EnerSys is actually a solid operator in a growing space. This is why Moody’s Ba2 high yield rating, with a 25%+ risk of default expectation does not make sense.

Using the CCFP analysis, Valens rates EnerSys as an investment grade IG4+ rating. This rating corresponds with a default rate below 2% within the next five years, a more realistic projection once a holistic understanding of the company’s risk is taken into account.

Ultimately, Uniform Accounting and the Credit Cash Flow Prime analysis highlights how EnerSys’s credit risk profile is much safer than what rating agencies believe. Using just GAAP metrics and rating agency’s calls, investors would be afraid to invest in the future.

SUMMARY and EnerSys’ Tearsheet

As the Uniform Accounting tearsheet for EnerSys (ENS:USA) highlights, the Uniform P/E trades at a 18.9x, which is below the corporate average valuation of 25.2x, but above its own historical valuation of 15.8x.

Low P/Es require low EPS growth to sustain them. In the case of EnerSys, the company has recently shown a 4% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, EnerSys Wall Street analyst-driven forecasts are for a 10% EPS shrinkage in 2021 and a 29% EPS growth in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify EnerSys’ $91.3 stock price. These are often referred to as market embedded expectations.

EnerSys is currently being valued as if Uniform earnings were to grow 1% annually over the next three years. What Wall Street analysts expect for EnerSys’ earnings growth is below what the current stock market valuation requires in 2021, but well above that requirement in 2022.

Furthermore, the company’s earning power is twice the corporate average. Cash flows and cash on hand are also twice its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low dividend and moderate credit risk.

To conclude, EnerSys’ Uniform earnings growth is slightly below its peer averages, and their valuations are trading in line with peer average levels.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research