As-reported financials are missing this Amazon competitor’s impressive recovery

Amazon and today’s company have been in a constant battle over online digital retail, and so far Amazon has been the dominant winner.

Looking at as-reported financial metrics, the global pandemic only furthered Amazon’s dominance, but Uniform metrics tell a much different story.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

For the last 10 years, one of the worst kept secrets in retail was how Walmart (WMT) has been losing its shirt to Amazon (AMZN). For much of the last decade, Walmart struggled to build an online and delivery presence that could compete with Amazon.

Walmart has struggled to grow its online presence because it has failed to identify a differentiator for Amazon.

It carries effectively the same inventory at the same price as Amazon, but consumers shopping online often defaulted to simply buying the product from the online brand they knew.

While Walmart faltered, Amazon ran away with the e-commerce industry, with its gross merchandise value rising to nearly 50% of all U.S. online sales in 2021.

Furthermore, the pandemic only seemed to strengthen Amazon’s position, because consumers did not want to deal with waiting in long lines outside a Walmart to get in and get what they wanted.

Consumers stuck at home under lockdown were often hesitant to go into a physical retail store. It was much easier to simply go online and order from Amazon.

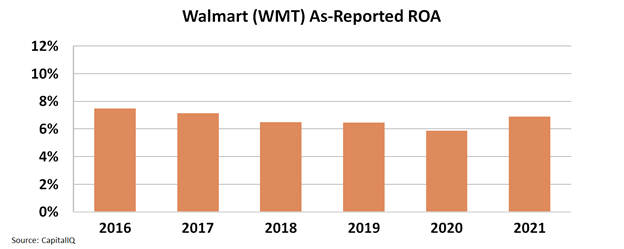

As-reported numbers reflect this competitive pressure too, as Walmart’s ROA declined from 8% in fiscal year 2016 to 6% in fiscal year 2020, with just a slight recovery to 7% in 2021.

The as-reported metrics seem to confirm the narrative surrounding Walmart versus Amazon.

Walmart did struggle for most of the last decade against Amazon, but the pandemic did not accelerate this decline. Instead, it was just the opportunity Walmart needed.

Historically Walmart’s problem has been attracting customers to its e-commerce platform. The pandemic was the perfect opportunity for Walmart to get its customers comfortable using its online platform, while also promoting order online and pick up in store.

Across the board, the pandemic accelerated the shift to e-commerce by five years, and Walmart was no exception to this trend.

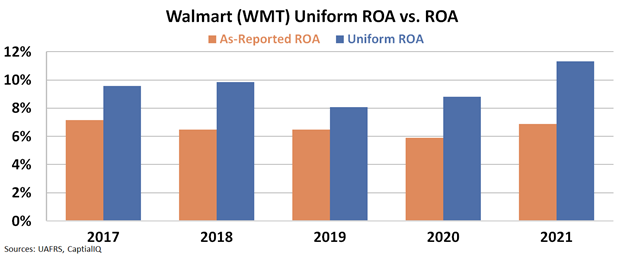

When looking at the Uniform financial metrics, the fiscal year 2021 boost from the pandemic becomes crystal clear. Walmart’s Uniform ROA, which had cratered from 13% in fiscal year 2011 to 9% in fiscal year 2020 bounced back to 11% levels in fiscal year 2021.

While Walmart has consistently struggled to keep up with Amazon, the pandemic might have been just the opportunity Walmart needed.

Yet, GAAP financials completely miss the fiscal year 2021 recovery and make it seem like another year of declining returns, while the company gets out competed by Amazon.

Only by using Uniform Accounting metrics can investors see how Walmart is successfully starting to make progress in turning around the competitive balance against its usurper.

SUMMARY and Walmart Inc. Tearsheet

As the Uniform Accounting tearsheet for Walmart Inc. (WMT:USA) highlights, the Uniform P/E trades at 27.9x, which is above the global corporate average of 23.7x and its own historical average of 25.6x.

High P/Es require high EPS growth to sustain them. That said, in the case of Walmart, the company has recently shown a 37% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Walmart’s Wall Street analyst-driven forecast is a 14% EPS decline in 2022, followed by a 16% EPS growth in 2023.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Walmart’s $145 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow 2% annually over the next three years. What Wall Street analysts expect for Walmart’s earnings growth is below what the current stock market valuation requires in 2022 but above that requirement in 2023.

Furthermore, the company’s earning power in 2021 is 2x the long-run corporate average. Also, cash flows and cash on hand are almost 4x its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals a low credit and dividend risk.

To conclude, Walmart’s Uniform earnings growth is below its peer averages, and the company is also trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research