This oil and gas giant may just be starting a decade with high profitability

Energy has been a complicated field since the beginning of 2022 when the war in Ukraine began.

As prices surged and European countries looked for different suppliers, U.S. companies found themselves in an advantageous position.

One of these companies was Exxon Mobil (XOM). Its profitability increased immensely last year, and it seems sustainable with the current energy space and the company’s plans to ramp up investments.

The market does not recognize this sustainable trend, causing this name to be undervalued.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

We have seen interesting stories play out in the energy space.

Russia’s invasion of Ukraine changed supply and demand dynamics, as Europe stopped the energy imports from Russia and prices surged faster than imagined.

We have talked before about how U.S. energy companies could benefit from this and supply the demand in Europe.

As prices rose, the shale resources of the U.S. became easier to extract and made more sense economically.

This can be the beginning of a new shale renaissance. Looking at some of the companies, we see that it might already have started.

One of the biggest companies in the space is signaling this kick-off with its rising profitability.

That is none other than Exxon Mobil Corporation (XOM)…

The company explores and produces crude oil and natural gas in the U.S. and operates through both upstream and downstream segments.

Last month, it reported bumper profits and historically high earnings that surprised analysts and investors alike.

The earnings per share came in nearly 4% more than the consensus, and the $95 billion revenue was 5% higher than the estimations.

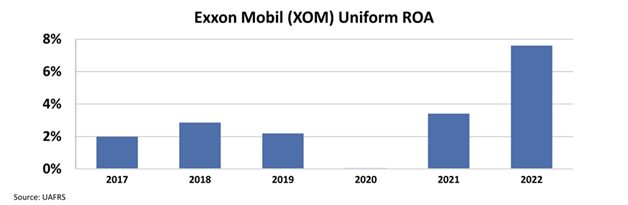

When we look at the return on assets (“ROA”) of the company, we see that it has jumped immensely last year, after the difficult times during the pandemic.

The ROA fell from 3% in 2018 to nearly 0% in 2020, as the demand for oil crashed.

In the past two years, the market was not only recovering, but prices skyrocketed particularly because of the war in Ukraine.

That had a very positive impact on Exxon’s profitability. The ROA has jumped from those 0% levels in 2020 to nearly 8% in 2022.

Now the main question is the sustainability of these returns, and what the market thinks about it.

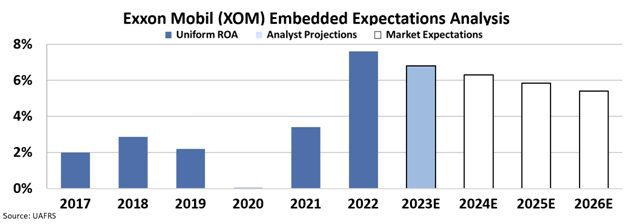

By utilizing our Embedded Expectations Analysis (“EEA”) framework, we can see what is expected from Exxon Mobil using its current valuation.

Our EEA starts by looking at the company’s current stock price. From there, we can calculate how the market thinks the company will perform in future years. Then, we can see if those expectations make sense or not.

We see that at $111 per share, the market expects Exxon’s ROA to fall below 6%. That is still higher than in past years but not as high as in 2022.

The market does not think that these high returns will be sustainable.

However, we have reasons to think otherwise. Shale renaissance is just starting, and it looks like U.S. resources will continue to be important imports for European countries.

Also, the management of Exxon made an interesting comment about how these high earnings are going to be used.

The company is not looking to grow its share buybacks further. In fact, it is open to reinvesting more in assets, highlighting we could see higher Capex going forward.

The market is not pricing in much growth, or for stronger ROAs for longer. It may be wrong thanks to the company’s willingness to ramp up investment and the overall macro environment.

SUMMARY and Exxon Mobil CorporationTearsheet

As the Uniform Accounting tearsheet for Exxon Mobil Corporation (XOM:USA) highlights, the Uniform P/E trades at 17.6x, which is around the corporate average of 18.4x but below its historical P/E of 458.3x.

Moderate P/Es require moderate EPS growth to sustain them. In the case of Exxon, the company has recently shown a 11,177% shrinkage in Uniform EPS to negative earnings.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Exxon’s Wall Street analyst-driven forecast is a 152% growth in 2022 and a 12% EPS shrinkage in 2023.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Exxon’s $119 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 11% annually over the next three years. What Wall Street analysts expect for Exxon’s earnings growth is above what the current stock market valuation in 2022 but below its requirement in 2023.

Furthermore, the company’s earning power is below its long-run corporate average. Moreover, cash flows and cash on hand are 1.5x its total obligations—including debt maturities, capex maintenance, and dividends. Also, the company’s intrinsic credit risk is 30bps above the risk-free rate.

All in all, this signals low dividend risk.

Lastly, Exxon’s Uniform earnings growth is in line with its peer averages but above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research