You can’t have the At-Home Revolution without the cloud, and this company is taking the cloud to the next level

Companies across the world have been forced to go digital so employees can work from home. For many companies, this step is well outside of their core competence. This company is making itself more valuable by supporting this now essential service.

Additionally, the cleaned up Uniform Accounting metrics highlight a more compelling story than investors might suspect from an initial glance.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

Here at Valens we often talk about how big changes in society can lead to radically different spending habits over time. For example, the work-from-home movement has accelerated demand for speakers, cars, and boats.

Families spent plenty on their homes before, but in 2020, the home became one of the only things to spend money on.

Twenty years ago, working from home on this scale would have been impossible. Employees would struggle to communicate ideas and share work. Services like Slack (WORK), Zoom (ZM), and Microsoft Teams (MSFT) make remote communication possible.

To help employees share their work seamlessly, companies are now turning to the cloud. Along with its many other benefits, the cloud enables individuals to perform numerous tasks remotely.

While the cloud has existed for several years now, 2020 saw corporate adoption of cloud services spike.

With the advancements of cloud technology and its increasingly valuable offerings, data centers have become more prevalent than ever before. As the cloud is someone else’s computer accessed from the internet, these platforms have to exist somewhere.

Arista Networks (ANET) is one of the key suppliers to data centers. The company is a critical provider of systems that enable the cloud to run efficiently.

In addition, Arista is a prominent provider of networking hardware and software. It is able to differentiate itself through creating tailored networking solutions for any data center size.

Investors might assume this company generates robust returns, as data centers are powering this societal transition to the cloud.

However, on an initial look using as-reported metrics, it looks like the firm hasn’t been able to differentiate itself from market returns.

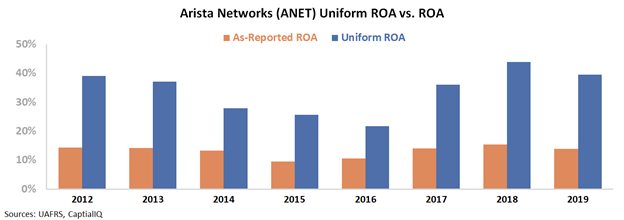

Diving deeper into the as-reported metrics, Arista Networks’ return on assets has remained consistent—around corporate averages over the past eight years. Specifically, ROA declined from 14% in 2012 to 10% in 2015. Since then, ROA has risen back to 14% levels in 2019.

Investors might see Arista’s returns and assume that without a competitive advantage, Arista is only able to see returns hover right around the corporate average of 12%.

Looking through a Uniform Accounting lens, it becomes clear that the firm’s business model is even better than it appears. Due to distortions around excess cash and R&D in GAAP accounting, profitability has been artificially suppressed.

Specifically, Uniform ROA has been at least two times greater than the as-reported metrics since 2012.

Once we make the necessary Uniform Accounting adjustments, we can see Arista Networks has in fact generated returns well above the as-reported numbers.

While Uniform ROA faded from 39% in 2012 down to 26% in 2015, since then, it peaked at 44% in 2018 before settling around 40% in 2019. This can be attributed to the firm’s surging demand. Arista is currently in the enviable position of supplying a booming market.

Without Uniform Accounting, investors are unable to understand the context of macro trends to invest in, such as the At-Home Revolution. The bedrock of investing is understanding a company’s fundamentals. With such distortions in a name like Arista Networks, any GAAP powered analysis will be no better than guesswork.

SUMMARY and Arista Networks, Inc. Tearsheet

As the Uniform Accounting tearsheet for Arista Networks, Inc. (ANET:USA) highlights, the Uniform P/E trades at 35.4x, which is above the global corporate average of 25.2x and its historical average of 23.8x.

High P/Es require high EPS growth to sustain them. In the case of Arista Networks, the company has shown an 8% Uniform EPS growth in the previous year.

Wall Street analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Arista Networks’ Wall Street analyst-driven forecast is a 28% EPS shrinkage in 2020, followed by an 11% EPS growth in 2021.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Arista Networks’ $323 stock price. These are often referred to as market embedded expectations.

The company would need to grow its Uniform earnings by 8% per year over the next three years to justify current stock prices. What Wall Street analysts expect for Arista Networks’ earnings growth is below what the current stock market valuation requires in 2020, but above that requirement in 2021.

Furthermore, the company’s earning power is 7x the long-run corporate averages. Also, cash flows and cash on hand are over 9x its total obligations—including debt maturities and capex maintenance. Together, this signals a low credit risk.

To conclude, Arista Networks’ Uniform earnings growth is below its peer averages, but the company is trading above peer average levels.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research