You still need to take care of your hygiene, even during economic downturns

In the first quarter of 2024, the U.S.’ economic growth slowed down, with the real GDP increasing by only 1.6%, a sharp drop from the 3.4% growth in the last quarter of 2023.

This slowdown is attributed to the Federal Reserve’s aggressive interest rate hikes, which began in March 2022 and sitting at a range of 5.25 to 5.50% currently, the highest since December 2000.

Despite these measures intended to curb high inflation, which remains at about 3.48%, the economy faces challenges such as reduced consumer purchasing power and increased household debt.

During economic downturns, investors often turn to safe havens like gold, treasury bills, and cash.

Within the stock market, companies like Colgate-Palmolive (CL), known for essential consumer staples, become attractive due to their ability to maintain steady sales through economic cycles, making them appealing for reducing portfolio risk during uncertain times.

Investor Essentials Daily:

Tuesday FA Alpha 50

Powered by Valens Research

The U.S. economy showed signs of slowing in the first quarter of 2024, with real gross domestic product (GDP) increasing at an annualized rate of 1.6%, according to advance estimates released by the Bureau of Economic Analysis.

This marked a sharp decline compared to the fourth quarter of 2023, when real GDP had grown 3.4%.

The slowdown in economic growth was largely due to the ongoing impact of the Federal Reserve’s aggressive interest rate hiking campaign to rein in high inflation.

The Fed had begun raising rates in March 2022 and by May 2024, had lifted the federal funds rate target range to 5.25 to 5.50% – the highest level since December 2000.

However, inflation as measured by the Consumer Price Index remains stubbornly high at around 3.48%. With prices continuing to rise sharply, eroding consumer purchasing power, the Fed signaled it still has more work to do and pushes back rate cuts further and further.

This aggressive tightening is having its intended effect of cooling demand, with GDP growth slowing sharply. It is also weighing on corporate margins as input costs rise and consumers spend less. Household debt loads have ballooned in recent years, exacerbating the economic drag from higher borrowing costs.

In environments where the economic outlook weakens due to factors like high-interest rates, investors typically rotate out of riskier assets and into safe havens thar are able to hold their value even during an economic downturn.

Some of the most common havens are gold, treasury bills, and cash due to their ability to retain or increase in value during times of market turbulence.

Within the stock market, defensive consumer staple companies offering essential products that consumers continue purchasing in both good and bad times are demonstrating similar characteristics.

One prime example is Colgate-Palmolive (CL), a leading producer of oral care and personal hygiene goods.

Its portfolio includes well-known brands such as Colgate, Palmolive, and Protex, which consumers rely on for basic hygiene needs.

This necessity-driven demand profile makes Colgate-Palmolive’s business highly defensive and resistant to economic downturns. While discretionary spending typically declines when the economy weakens, people still need to purchase basics like toothpaste, soap, and laundry detergent.

As a result, Colgate-Palmolive has historically delivered steady sales growth across market cycles without significant volatility.

Even in the face of macro headwinds like high inflation eroding consumer purchasing power and rising interest rates pressuring spending, Colgate-Palmolive has continued delivering strong top and bottom line results each quarter.

This is because the demand for its products is less dependent on discretionary income levels or consumer sentiment compared to more economically sensitive sectors.

This defensive quality makes Colgate-Palmolive an appealing choice for investors looking to reduce portfolio risk during times of economic uncertainty.

That is why it is a great FA Alpha 50 name.

Throughout financial market history, many of the world’s most successful investors have been candid in their belief that Generally Accepted Accounting Principles (“GAAP”) distort economic reality.

Warren Buffett, for example, once said investors should “concentrate on the world of companies, not arcane accounting mathematics.”

Investors who neglect the very real issues with as-reported accounting can find themselves caught up in investing with the crowd, blindly following hot “themes” without a thorough grasp of how to understand the businesses in question.

The only true way to focus on the “world of companies,” as Buffett suggests investors do, is to present a clear picture of how a business operates, something that can only be done by adjusting financial statements to reflect the arbitrary nature of certain accounting rules that leave much to discretion.

The world’s best investors understand the need to make these adjustments, which allows them to focus not on picking out the most popular companies but rather on looking for great names in sleepy areas that the market isn’t paying much attention to. From there, the goal is to then identify quality companies with significant growth potential at reasonable prices.

That’s exactly what we’ve set out to do with the FA Alpha, our monthly list of 50 companies that rank at the top for quality, high growth, and low valuations.

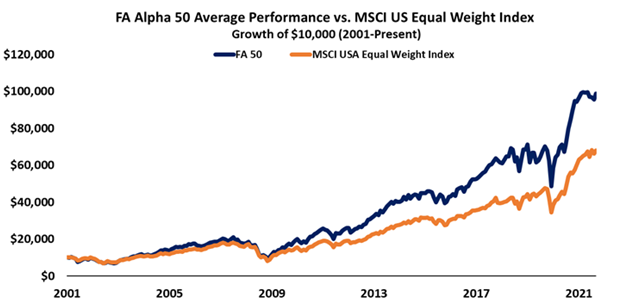

This list has outperformed the market by 300 basis points per year for over 20 years now, effectively doubling the performance of the market by focusing on the real fundamentals and valuations of companies with our proprietary Uniform Accounting framework.

See for yourself below.

To see the other 49 names on the list, click here.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research