Yum China may be a surprising winner of a housing-led downturn in China

As the world painfully experienced in 2008, a crashing housing market can lead to economic hardship, particularly for those at the lower end of the income spectrum. When the economy enters a period of sluggish growth or even a recession, consumers typically look for ways to tighten their purse strings, which for industries like fast food, tends to mean higher sales.

With uncertainty surrounding the housing market in China, many are wondering if the country will see a significant slowdown in growth, which could leave certain restaurant chains operating in the country well-positioned relative to others.

Today, we use Uniform Accounting to dive into one of the primary operators in the Chinese fast food market and discover whether its past experiences with economic downturns suggest potential resilience in the future.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

Anyone who lived through the 2008 Great Recession, which nearly brought the world economy to its knees, knows that a real estate-driven credit crisis can have disastrous consequences.

What started as a bursting bubble in the U.S. housing market quickly developed into a full-blown financial crisis, as fear gripped Wall Street banks and other financial institutions, many of which were intricately connected to the subprime mortgage market that sparked the crisis in the first place.

The result was a dramatic credit crunch, with lending across the economy grinding to a halt. Even with massive infusions of government support, a sluggish recovery took nearly a decade to bring the economy back to pre-crisis levels of health.

With these past experiences in mind, investors are increasingly concerned about issues in China’s housing market, which has seen its largest property developer, Evergrande Group (3333:HKG), teetering on the brink of default in recent months, something we discussed in detail a few weeks ago.

In 2008, while the entire U.S. market, along with markets around the globe, was hit hard, one area recovered much faster than most others…companies catering to people on a budget, like dollar stores and fast food restaurants.

With many consumers hit hard by difficult economic conditions, they quickly responded by turning to places they could be a bit thriftier with their spending, lending a boost to fast food corporations and their restaurant chains around the world.

That’s why industry giants like Yum! Brands (YUM), which operates household names in the fast food industry such as KFC, Pizza Hut, and Taco Bell, saw their stock prices reach new highs by 2010, while the S&P 500 took another 3 years to fully recover.

If the Chinese economy does face some hangover from its current real estate woes, perhaps Yum! Brand’s former Chinese subsidiary, Yum China Holdings (YUMC), which now trades entirely independently on the New York Stock Exchange, might be well-positioned to fare better than others.

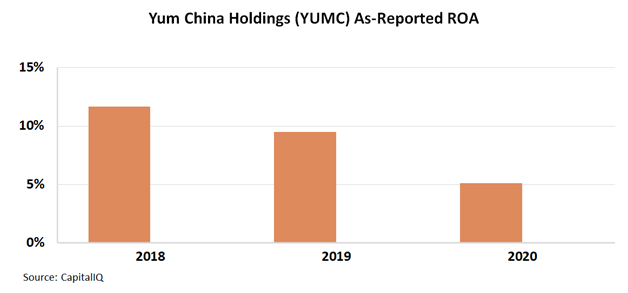

To see if the fast food resilience story contains merit in China, we can look at the actual data to gauge Yum China’s performance when the COVID-19 pandemic hit.

Based on as-reported metrics, it appears the underlying company is struggling, with as-reported return on assets (“ROA”) being cut in half from 10% in 2019 to 5% in 2020, as restaurants and other social-facing businesses dealt with strict government restrictions.

In reality, by using Uniform Accounting we can see that Uniform ROA only fell from 11% to 8%, much less of a decline than as-reported metrics suggest.

This suggests that Yum China’s restaurants were incredibly resilient, even in the midst of a devastating pandemic and some of the harshest lockdown restrictions in the world.

If the housing issues and growth slowdown fears in China actually play out over the next few years, Yum China may be better equipped to handle it than most.

SUMMARY and Yum China Holdings, Inc. Tearsheet

As the Uniform Accounting tearsheet for Yum China Holdings, Inc. (YUMC:USA) highlights, the Uniform P/E trades at 36.5x, which is above the global corporate average of 24.3x and its historical P/E of 35.1x.

High P/Es require high EPS growth to sustain them. In the case of Yum China, the company has recently shown a 32% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Yum China’s Wall Street analyst-driven forecast is a 50% and 15% EPS growth in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Yum China’s $60 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow 19% annually over the next three years. What Wall Street analysts expect for Yum China’s earnings growth is above what the current stock market valuation requires in 2021, but below that requirement in 2022.

Furthermore, the company’s earning power in 2020 is above the long-run corporate average. Moreover, cash flows and cash on hand are almost 4x its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals a low credit and dividend risk.

Lastly, Yum China’s Uniform earnings growth is above peer averages, while the company is trading in line with its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research