This dominant work-from-home leader has used its follower status to unlock massive returns that are only apparent using Uniform Accounting

During the pandemic, people have had to adapt to new working and learning environments. This includes the use of video conferencing to replace the in-person interactions that occurred prior to the pandemic.

Today’s company was a late entrant to the competitive video conferencing industry, but has taken massive share to great success this year.

UAFRS (Uniform) based analysis shows the firm’s real performance, with investors looking at bad data and missing the profitability of the firm.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

The iPhone was not the first smartphone on the market. That distinction belongs to IBM (IBM) when it unveiled the world’s first smartphone in 1992—15 years earlier than Apple. The phone only sold 50,000 units and had just an hour of battery life.

Similarly, when Microsoft released Windows, it was largely inspired by the interface developed by Apple. Years of court cases ultimately settled in Microsoft’s favor, paving the way for its industry-leading position.

Likewise, Edison was not the first person to invent the lightbulb. He merely optimized it by including longer lasting filaments that made it a viable commercial option.

Oftentimes, the most successful players in a particular space are not the first movers, but rather the followers, and not even just the “fast” followers.

These companies or people sit back and wait for others to face initial struggles, before figuring out how to make a better product. The technology for a proper smartphone simply was not there in 1992 when IBM first released one, but Apple had over a decade to learn from mistakes and optimize the product.

This also will often lead to higher profitability, as there is less R&D costs and marketing spent on getting users familiar with the product. The company doesn’t have to play the role of “evangelist” as aggressively.

One company with a meteoric rise as a follower in recent months is teleconferencing company Zoom (ZM). Its founder, Eric Yuan, previously worked at Cisco (CSCO), which has long had its own widely embraced video communication platform WebEx.

While at Cisco, Yuan pitched a smartphone-friendly video conferencing system that was rejected by management. Yuan learned from the mistakes at WebEx before leaving to launch his own solution. Zoom was intended to be more simplistic and user-friendly, building off the work of previous video conferencing platforms.

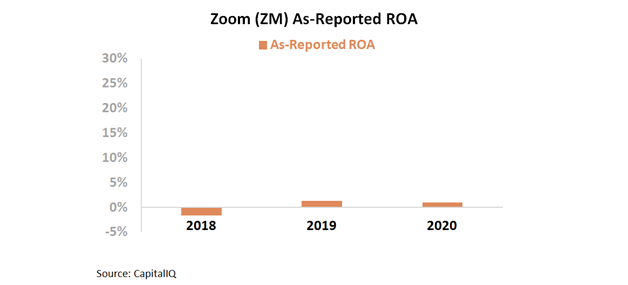

However, only looking at as-reported metrics, Zoom appears to have failed to capitalize on its impressive adoption rates and widespread use—from businesses, schools, all the way to the “zoom weddings.”

The firm’s as-reported return on assets (ROA) have been between -2% and 1% over the past 3 years. As Zoom has clearly seen wide success over the past year, investors only looking at as-reported metrics are scratching their heads as to how these fundamental tailwinds haven’t translated into profitability.

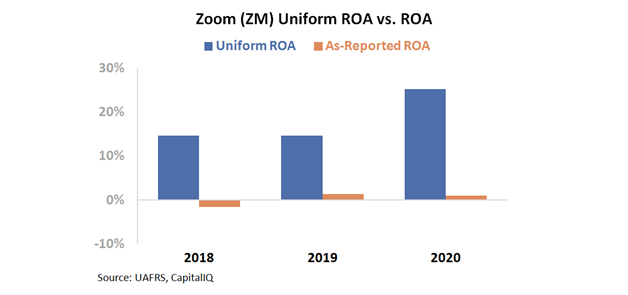

However, this picture of Zoom’s performance is inaccurate, pulled down by distortions in as-reported accounting. Due to the GAAP treatment of stock option expense and excess cash, among other distortions, as-reported reporting has failed to capture the success of the firm.

The Uniform ROA for Zoom was in fact more than 10x as-reported figures over the past 3 years. Uniform ROA was 25% in 2020, not the 1% as-reported figure.

However, understanding how strong historical returns have been does not explain if the stock is undervalued or overvalued.

To understand if the firm can continue to create value for shareholders, we can use the Embedded Expectations Framework to easily understand market valuations.

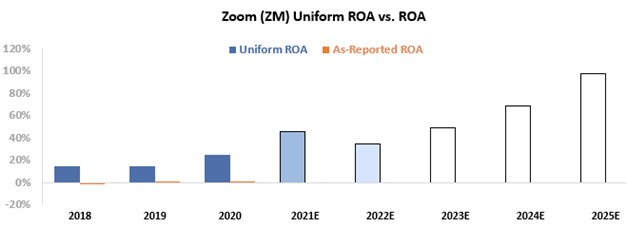

The chart below explains the company’s historical corporate performance levels, in terms of ROA (dark blue bars) versus what sell-side analysts think the company is going to do in the next two years (light blue bars) and what the market is pricing in at current valuations (white bars).

As you can see, both analysts and the market expect returns to grow well beyond current levels. Market expectations are for returns to expand to 100% in 2025, which is 4x higher than current levels.

Clearly, Zoom has established itself as the dominant player in the video space, and currently holds a 43% market share. That being said, while this has proven to be a successful business, expecting such sustained pronounced growth may be unsustainable.

As people begin to return to work and the classroom, the need for video conferencing may decrease, or at least is unlikely to continue to grow at the rates it has during the pandemic.

Only looking at as-reported accounting, investors would be puzzled by the returns of this video communications company in 2020. Uniform Accounting shows why the market is so excited for this video conferencing company. And yet, while Zoom has done incredibly well in the past, it will need to continue to grow returns by almost four times to meet market expectations.

Zoom Video Communications, Inc. Embedded Expectations Analysis – Market expectations are for a material Uniform ROA expansion, but management may have concerns about the Zoom platform, growth, and their ability to handle increased usage

ZM currently trades at a historical high relative to Uniform earnings, with a 175.3x Uniform P/E (Fwd V/E’). At these levels, the market is pricing in expectations for Uniform ROA to expand from 25% in 2020 to a peak of 100% in 2025, accompanied by 55% Uniform asset growth going forward.

However, analysts have less bullish expectations, projecting Uniform ROA to jump to 66% in 2021 driven by macro tailwinds, before falling to 37% in 2022, accompanied by 127% Uniform asset growth.

Historically, as a video communications platform in an increasingly virtual working world, ZM has seen stable, robust profitability. After declining from 22% in 2017 to 15% levels in 2018-2019, Uniform ROA rebounded to 25% in 2020 following its IPO.

Meanwhile, as a recent startup, Uniform asset growth has been robust and positive in each year, while ranging from 99%-155%.

Performance Drivers – Sales, Margins, and Turns

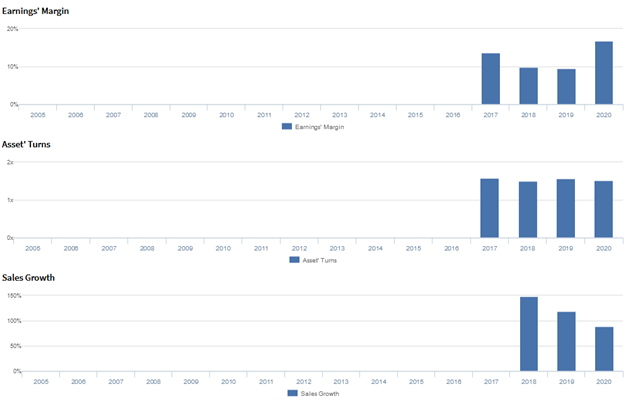

Trends in Uniform ROA have been driven by trends in Uniform earnings margins and stability in Uniform asset turns.

Uniform margins compressed from 14% in 2017 to 9% in 2019, before jumping to a peak of 17% in 2020. Meanwhile, Uniform turns have remained at 1.5x-1.6x levels since 2017.

At current valuations, the market is pricing in expectations for a material expansion in both Uniform margins and Uniform turns.

Earnings Call Forensics

Valens’ qualitative analysis of the firm’s Q1 2021 earnings call highlights that management may lack confidence in their ability to maintain operating cash flow growth, meet revenue guidance, and grow Zoom Phone similar to Zoom Video.

However, they are also confident last year’s scheduled spring activity was pushed back to mid-summer due to significant snowfall in April and that Q1 2019 was followed by an unusually wet selling season, resulting in higher-than-anticipated year-end inventory.

Furthermore, they may be concerned about the potential of Zoom’s built-in chat feature and the use cases of their prosumer model.

Moreover, they may lack confidence in their ability to sustain the usage growth of Global 2000 customers and meet the capacity needs of the surge in Zoom usage.

Additionally, they may be exaggerating Zoom’s ability to integrate well with Slack and Microsoft Teams, the progress of their salespeople hirings, and the potential of Zoom 5.0’s new security features.

Also, they may have concerns about their ability to leverage the resources of top security firms for Zoom’s security functionality, the sustainability of growth from customers with more than 10 employees, and the costs of the services of public cloud providers.

In addition, they may lack confidence in their ability to sustain their annualized meeting minutes run rate and execute on their Dropbox partnership.

Finally, they may be concerned about macro pressures to their churn rate expectations, and they may be exaggerating their focus on video and voice service.

UAFRS VS As-Reported

Uniform Accounting metrics also highlight a significantly different fundamental picture for ZM than as-reported metrics reflect.

As-reported metrics can lead investors to view a company to be dramatically stronger or weaker than real operating fundamentals highlight. Understanding where these distortions occur can help explain why market expectations for the company may be divergent.

As-reported metrics significantly understate ZM’s margins, a key driver of profitability. For example, as-reported EBITDA margin was 5% in 2020, materially lower than Uniform earnings margin of 17%, making ZM appear to be a much weaker business than real economic metrics highlight.

Moreover, since 2019, as-reported EBITDA margin has maintained 4%-5% levels, while Uniform margins have improved from 9% to 17%, directionally distorting the market’s perception of the firm’s recent profitability trends.

SUMMARY and Zoom Video Communications, Inc. Tearsheet

As the Uniform Accounting tearsheet for Zoom Video Communications, Inc. (ZM:USA) highlights, its Uniform P/E trades at 175.3x, which is above global corporate average valuation levels and its historical average valuations.

High P/Es require high EPS growth to sustain them. In the case of Zoom, the company has recently shown a 54% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Zoom’s Wall Street analyst-driven forecast an EPS growth of 400% and a decline by 1% in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Zoom’s $383 stock price. These are often referred to as market embedded expectations.

The company needs to have Uniform earnings grow by 113% each year over the next three years to justify current prices. What Wall Street analysts expect for Zoom’s earnings growth is above what the current stock market valuation requires in 2021 but below its requirement in 2022.

Furthermore, the company’s earning power is 4x the corporate average. Also, cash flows are 10x higher than its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit and dividend risk.

To conclude, Zoom’s Uniform earnings growth is way above peer averages. Therefore, as is warranted, the company is also trading above average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research