Finding a diamond in the rough

Investing in the healthcare sector presents a formidable challenge. It requires a very specific kind of expertise and understanding. The complexities of this field are challenging to navigate.

One of the most daunting tasks is predicting whether newly developed drugs will pass the required tests and eventually emerge as successful products.

Thankfully, medical devices are easier to forecast, and therefore we can have more meaningful discussions about medical device makers under our Uniform Accounting framework. Today, we’ll take a look at one

Also below, is the company’s Uniform Accounting Performance and Valuation Tearsheet..

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

It is difficult to invest in the healthcare sector. It requires investors to have a lot more sector-specific competence than other sectors.

In some cases, one must understand if a newly developed drug is going to be able to pass tests and be approved to have an edge over other investors, which means years of experience in the sector.

The constant evolution of medical science and the rigorous approval processes compound the difficulties. In essence, to make a successful investment in healthcare, one needs not only financial acumen but also an in-depth comprehension of medical and regulatory landscapes.

Even when companies launch successful products and dominate markets, some don’t get the attention they deserve simply because they operate in the healthcare sector.

Zynex (ZYXI), for instance, is one of these companies. It develops medical devices to treat chronic and acute pain and activate muscles for rehabilitative purposes with electrical stimulation.

Zynex’s electrotherapy business warrants special attention. Its consumable model has led to a high recurring revenue stream more resilient to sudden economic changes.

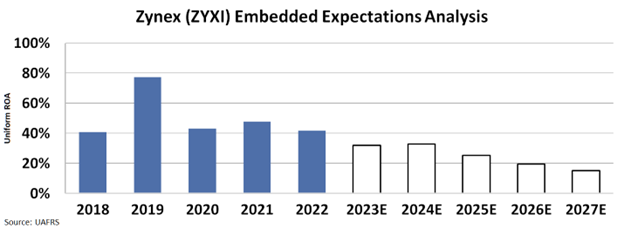

These attributes make Zynex a highly profitable and stable company, and it can also be seen from its profitability. The company managed to keep its Uniform return on assets (“ROA”) around 40% for the last three years, consistently delivering strong financial performance.

Take a look…

This shows the company has successfully built a stable business, even against troubling times like the pandemic.

And yet, the market doesn’t seem to understand the company’s value as a next-generation medicine company.

We can see this through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the market expects the company’s ROA to fall to 15%, which would be the lowest in recent years.

The market has a pessimistic viewpoint about Zynex. Such skepticism, though, overlooks the strides Zynex has made since then, disregarding its evolving strategies and performance.

Furthermore, the market seems to assume the worst regarding the company’s future innovation and differentiation. This is where the market’s perception diverges from the company’s capabilities and potential.

Zynex’s commitment to innovation is evident through its distinct products and strategic decisions, a fact that escapes the market’s notice.

While the market remains skeptical, the evidence suggests that Zynex is undervalued. It might be an opportunity for investors to take.

SUMMARY and Zynex, Inc. Tearsheet

As the Uniform Accounting tearsheet for Zynex, Inc. (ZYXI:USA) highlights, the Uniform P/E trades at 18.1x, which is around its corporate average of 18.4x and its historical P/E of 18.5x.

Average P/Es require average EPS growth to sustain them. In the case of Zynex, the company has recently shown a 20% growth in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Zynex’s Wall Street analyst-driven forecast is a 4% EPS growth in 2023 and a 30% EPS growth in 2024.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Zynex’s $8.33 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 2% annually over the next three years. What Wall Street analysts expect for Zynex’s earnings growth is above what the current stock market valuation requires through 2024.

Furthermore, the company’s earning power is 7x its long-run corporate average. Moreover, cash flows and cash on hand are 2.5x its total obligations—including debt maturities, capex maintenance, and dividends. Also, the company’s intrinsic credit risk is 170bps above the risk-free rate.

All in all, this signals average credit risk.

Lastly, Zynex’s Uniform earnings growth is in line with its peer averages and its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research