A return of 2,600% in a span of two decades! See the top holdings of the best performing fund in the Philippines

When the great investors speak, the global investing community listens.

It’s no wonder why John Bogle, Warren Buffett, Seth Klarman, and Charlie Munger gain popularity and a lot of followers. Their long-term stock market outperformance has put weight and credibility into every word they say.

In the Philippines, there is one investor who often draws a lot of attention. He has become the go-to person for regular investors and professional money managers seeking investing advice and equity market wisdom.

He has earned his rightful column in one of the leading newspapers in the country.

From helping out in their family store back in the day, he is now managing the best performing fund in the country.

In addition to examining the fund he manages, we’re including a deeper look into one of the fund’s largest current holding, providing you with the current Uniform Accounting Performance and Valuation Tearsheet for that company.

Philippine Markets Daily:

Friday Uniform Portfolio Analytics

Powered by Valens Research

Wilson Sy is a board member of multiple publicly-listed companies such as A Brown Co., Basic Energy Corp., and Jollibee Food Corp. He also served as a chairman of the Manila Stock Exchange in 1994 and the Philippine Stock Exchange two years later.

However, he is most known for being referred to as the “Warren Buffett of the Philippines.” At one point, the Philequity Fund gained over 2,600% returns in a span of two decades, justifying the moniker.

Sy began his career in trading when he worked for the Bancom Group of companies in 1975, specifically in Barcelon Roxas Securities Inc.

In 1986, he established his very own stock brokerage firm, Wealth Securities. Thereafter, he and his friends founded the Philequity fund.

The fund’s investment objective is “to seek long-term capital appreciation through investing primarily in equity securities of listed Philippine companies while considering the liquidity and safety to manage risk.”

With Sy as its fund manager, the Philequity fund became the country’s longest-running and top performing mutual fund. As of November 2019, the Philequity fund totaled to PHP 11.3bn, greater than the industry average of PHP 7.7bn.

We get to peer into Wilson’s investment acumen through his book, “Opportunity of a Lifetime: Investment Secrets Behind the Success of Philequity Fund.”

Another way to peer into his investment philosophy is through the lens of Uniform Accounting.

Because if we rely on the as-reported Philippine Financial Reporting Standards-based (PFRS-based) financial statements, some of his portfolio holdings look ill-conceived.

Universally, relying on as-reported numbers misleads investors in determining whether or not a company is truly profitable. Its effects will be compounded when the asset allocation for any portfolio is based on as-reported accounting.

In order to gauge a company’s true earning power, the financial statements of companies must be restated to create a single, consistent set of global accounting standards called Uniform Adjusted Financial Reporting Standards (UAFRS) or Uniform Accounting.

The table below shows the top non-financial holdings of Philequity Fund along with their Uniform return on assets (ROA’), as-reported ROA, and ROA distortion—the difference between Uniform and as-reported ROA.

Looking solely at the as-reported ROA numbers, you may wonder why several of these companies were chosen since their returns look quite poor. Many are below global corporate average returns of 6%.

However, the Uniform ROA metric paints a different picture, showing robust returns ranging from 7% to 39%.

Contrary to what as-reported numbers suggest, these companies are actually quite profitable, with real earnings well above cost-of-capital levels.

As such, it should not be surprising that when analyzing the non-financial holdings of the Philequity Fund, the figure that stands out is the huge discrepancy between Uniform ROA and as-reported ROA.

While the difference in raw figures may not seem too distant, the distortion in percentage ranges from 7% to 460%, with International Container Terminal Services (ICT:PHL), Ayala Corporation (AC:PHL), and SM Investments Corporation (SM:PHL) having distortions greater than a hundred percent.

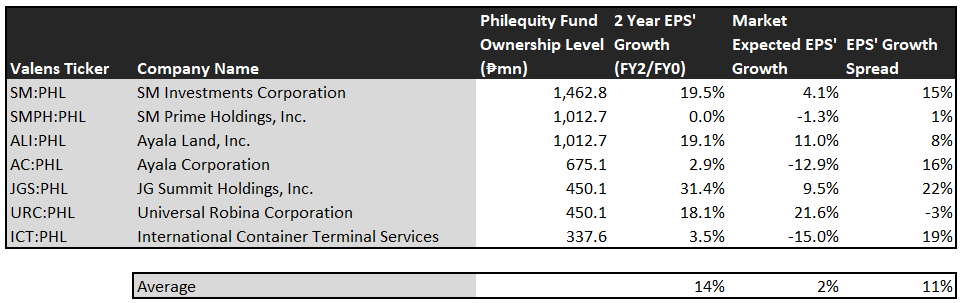

Looking at three interesting data points:

– The 2 year EPS’ growth is when we convert consensus analyst estimates to the Uniform Accounting framework. This represents the Uniform earnings growth the company is likely to have for the next two years

– The market expected EPS’ growth is how much the company’s Uniform earnings need to grow per year in the next two years to justify the current stock price of the company. This is the market’s embedded expectations for Uniform earnings growth

– The EPS’ growth spread is the difference between the 2 year EPS’ growth and market-expected EPS’ growth

On average, Philippine companies are expected to have 6% annual Uniform earnings growth over the next few years.

Philequity Fund’s top holdings are forecast to surpass that with 14% projected Uniform earnings growth in the next two years. Meanwhile, the market is seeing these companies grow by 2% a year, mispricing earnings growth by an average of 11% (difference due to rounding).

Among these companies, JG Summit Holdings, Inc. (JGS:PHL) has the highest Uniform earnings growth dislocation. Just last month, JGS and DHL entered into a joint venture to form DHL Summit Solutions Inc. to capitalize on the growing logistics needs of the Philippines.

Market is pricing this conglomerate to grow by 10% in the next two years. Meanwhile, the analysts are seeing robust 31% Uniform earnings growth.

Another company with understated earnings growth is ICT. The market is pricing the country’s leading port management company to shrink by 15% in the next two years.

However, analysts are seeing modest 4% Uniform earnings growth fueled by the firm’s capacity expansion efforts and new shipping contracts across the Oceania region.

Meanwhile, there is one company in the portfolio that Philequity may need to take a deeper review on—Universal Robina Corporation (URC:PHL).

The market is pricing URC to have 22% earnings growth moving forward. Analysts are a little more bearish, forecasting 18% growth annually.

With an average as-reported ROA of 6% and market-expected earnings growth of 2% annually, one might think that the Philequity Fund portfolio is weak.

However, through the lens of Uniform Accounting, for the most part, Philequity’s portfolio looks like a high-quality, undervalued set of stocks with businesses displaying strong earning power potential.

Ayala Corporation Tearsheet

Today, we’re highlighting one of the largest individual stock holdings in Philequity—Ayala Corporation.

As the Uniform Accounting tearsheet for Ayala Corporation (AC:PHL) highlights, Uniform P/E trades at 13.0x, well below market average valuations and slightly below its historical averages.

Low P/Es require low, and even negative, EPS growth to sustain them. In the case of Ayala Corp., the company has recently shown a modest 4% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for PFRS earnings and convert them to Uniform earnings forecasts. When we do this, Ayala Corp.’s sell-side analyst-driven forecast shows a 49% earnings growth into 2019, followed by a decline of 29% in 2020.

Based on the current stock market valuations, we can back into the required earnings growth rate that would justify PHP 752 per share. These are often referred to as market embedded expectations. Even if Ayala Corp.’s Uniform earnings shrinks by 17% over the next three years, they will meet their current market valuation levels.

What sell-side analysts expect for Ayala Corp.’s earnings growth is above what the current stock market valuation requires.

To conclude, Ayala Corp.’s Uniform earnings growth is above peer averages in 2020. Furthermore, the company is trading below average valuations of their peers.

The company has above average earning power—doubling corporate average returns—based on its Uniform ROA calculation. Together, this signals a low cash flow risk to the current dividend level in the future.

About the Philippine Market Daily

“Friday Uniform Portfolio Analytics”

Investors who don’t engage in the buying or selling of securities for a living oftentimes rely on professionals to manage their own investments within the scope of their investment policies.

With so many funds and managers out there, it can get confusing and difficult to decide which one best suits your needs as an investor.

Every Friday, we focus on one fund in the Philippines and take a deeper look into their current holdings. Using Uniform Accounting, we identify the high-quality stocks in their portfolio which may not be obvious using the as-reported numbers.

We also identify which holdings may be problematic for the fund’s returns that they would need to reconsider from a UAFRS perspective.

To wrap up the fund analysis, we highlight one of their largest holdings and focus on key metrics to watch out for, accessible in our tearsheets.

Hope you’ve found this week’s focus on the Philequity Fund interesting and insightful.

Stay tuned for next week’s Friday Uniform Portfolio Analytics!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com