Acquiring and reviving an old mine is a part of this company’s growth strategy, and its returns are higher than the reported below cost of capital!

The coronavirus pandemic sent China’s economy tumbling early this year when lockdowns and travel bans restricted business activities. The government focused on swiftly addressing the health crisis so that by April, people and companies started returning to pre-pandemic operations.

While the Chinese stock market has rebounded from its lows in the first half of the year, one particular commodity has hit all-time highs.

This company has taken advantage of the prospects that come with these all-time highs, as reflected by its recent acquisition efforts. However, as-reported metrics look at this company as a weak business, with return on assets (ROA) below cost of capital. Uniform Accounting, on the other hand, shows there is gold in the company’s strategies.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Wednesday Uniform Earnings Tearsheets – Asia-listed Focus

Powered by Valens Research

Warren Buffett once said that “gold is basically a way of going long on fear.” That makes sense, especially since gold has long been considered a safe haven investment. When economic crises occur, most investors jump to invest into something they can physically hold and attach value to, like gold.

Last week, we talked about the cultural significance of gold in China, which paved the way for the country to become the largest consumer of gold as well as its largest producer. Although that ranking has not changed, the gold industry was not safe from the negative effects of the pandemic, despite gold being a safe haven.

During the first three months of 2020, the country’s GDP contracted by 6.8% from the same period last year, its biggest drop in almost three decades. China’s economy shrank due to the piling up of unsold inventories, lower store traffic with people staying at home, and the plunge in the country’s exports as overseas consumer demand dropped.

By Q2 2020, the country’s GDP grew by 3.2% compared to a year ago as the government prioritized the containment of the coronavirus outbreak and reopened the economy. This recovery is seen with the soaring sales of construction vehicles, increases in rail freight volume, spike in daily electricity generation, and increase in car sales.

China’s gold consumption shrank by 38% in the first half of the year amid the pandemic and the high prices, according to the China Gold Association. Moreover, the use of gold in jewelry and consumer spending in gold coins and bars both fell by 42% and 32%, respectively.

Even as China’s economy recovered, demand for gold remained muted. However, as mentioned earlier, when investors get worried, they tend to shift to investing in safe haven investments, with gold as the top option.

Gold has commonly been seen as a “bet against inflation and extreme conflicts.” Even if demand for physical gold weakened, gold trading volumes and prices started rising to all-time highs and people began to invest in gold-linked products, such as gold exchange traded funds (ETFs).

Among one of the gold companies taking advantage of the higher gold prices is Chifeng Jilong Gold Mining Co., Ltd.

Since the company became publicly listed in 2012, Chifeng Gold has made multiple mergers and acquisitions that expanded both its scale and industrial chain. Some of its most recent acquisitions include the USD 275 million Sepon mine in Laos and the USD 257 million MMG Laos Holdings Limited, in November 2018 from MMG Ltd.

Gold production at the Sepon mines was halted in December 2013 under MMG Ltd. because of low reserves and lower profitability and margins compared to copper. This year, Chifeng Gold revived the processing of gold ore in the Sepon mine in Laos, with its first stream of gold produced in June.

After years of focusing on copper in the aforementioned mine, oxide copper reserves then started to deplete, which resulted in the company renovating some of its plant and infrastructure used in processing copper to produce gold ore.

This revamp of gold production is a manifestation of Chifeng Gold’s strategy of achieving growth through three parallels: (1) the parallel production of gold and copper, (2) the parallel processing of oxide and primary ores, and (3) the parallel mining of both open cut and underground mines.

For a mine that hadn’t produced gold in almost seven years, it now continues gold production ahead of schedule.

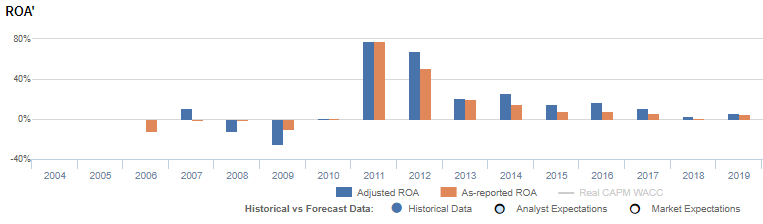

Even though Chifeng Gold has remained committed to its growth strategy and has leveraged on high gold prices, the company’s as-reported returns are still muted. Since 2011, Chifeng’s as-reported ROA has been declining and is currently at 5% in 2019.

This is a misrepresentation of the company’s profitability. Chifeng Gold’s real economic profitability is better reflected with Uniform Accounting adjustments, which show its TRUE earning power.

One metric that causes distortions in as-reported ROAs is its massive amortization expense.

Amortization expense is generated from the company’s use of intangible assets in a given reporting period. As such, it is a non-cash expense that is spread throughout the intangible asset’s useful life. As a non-cash expense, it does not represent an actual cash outflow.

Deducting amortization expense from the company’s revenues distorts its profitability because there is no actual cash flow that happens when amortization is charged.

Adding back amortization expense is necessary to convert the company’s net income into actual cash flows.

After amortization expense and other significant adjustments are made, we can see that Chifeng Gold has better profitability than what as-reported metrics show. Although it has also been declining, the company’s Uniform ROA is stronger at 6% in 2019, compared to as-reported ROA of 5%.

Chifeng Gold’s valuations are above corporate averages

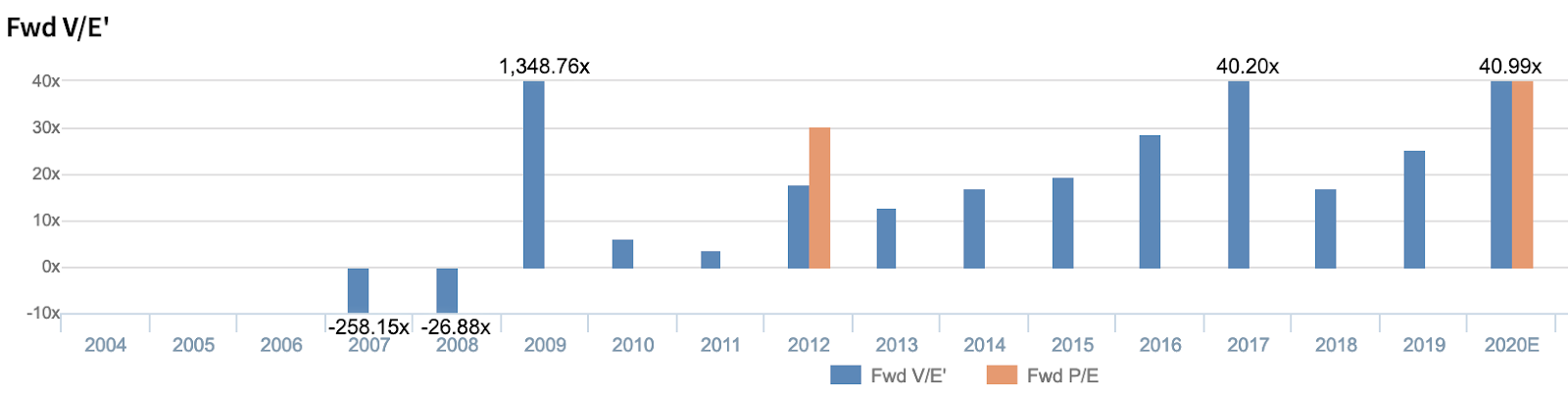

Chifeng Jilong Gold Mining Co., Ltd. (600988:CHN) currently trades above corporate averages at a 41x Uniform P/E (blue bars), but below its as-reported P/E of 47.8x (orange bars).

At these levels, the market is pricing in expectations for Uniform ROA to decrease to 4% in 2024, accompanied by 39% Uniform asset growth going forward.

Analysts have bullish expectations, projecting Uniform ROA to rise to 9% in 2021, accompanied by a 18% Uniform asset growth.

Chifeng Gold’s profitability is much better than you think it is

As-reported metrics are distorting the market’s perception of the firm’s profitability.

If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics highlight.

Chifeng Gold’s as-reported ROA has been lower than its Uniform ROA in the past eight years. For example, Uniform ROA is 6% in 2019, higher than the as-reported ROA of 5%. When Uniform ROA was at 68% in 2012, as-reported ROA was only 51%.

The company’s Uniform ROA for the past eight years has ranged from 3% to 68%, while as-reported ROA ranged only from 2% to 51% in the same time frame.

From 11% in 2007, Uniform ROA fell to negative levels in 2008-2009, before reaching peak 78% in 2011. Then, Uniform ROA slid to 6% in 2019.

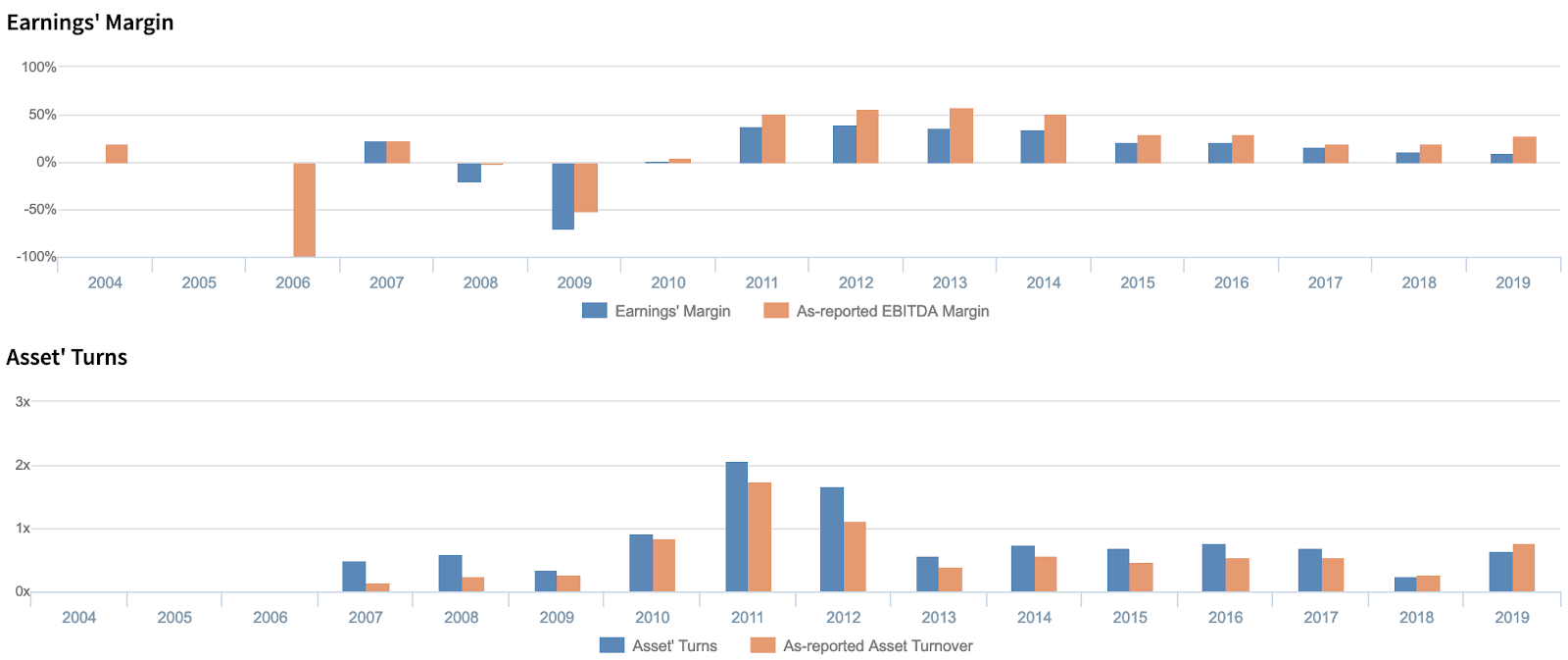

Chifeng Gold’s Uniform earnings margins are weaker than you think but its Uniform asset turns have historically made up for it

Volatility in Uniform ROA has been driven by trends in both Uniform earnings margins and Uniform asset turns, with peaks and troughs lining up historically with that of Uniform ROA.

From negative levels in 2008-2009, Uniform earnings margins rose to 41% in 2012 before gradually decreasing to 10% in 2019.

Meanwhile, Uniform asset turns increased from 0.4x in 2009 to a peak of 2.1x in 2011, before falling to 0.6x in 2013. It then remained at 0.7x-0.8x levels in 2014-2017, before sliding to 0.2x in 2018 and slightly rising back to 0.6x in 2019.

SUMMARY and Chifeng Jilong Gold Mining Co., Ltd. Tearsheet

As the Uniform Accounting tearsheet for Chifeng Jilong Gold Mining Co., Ltd. (600988:CHN) highlights, its Uniform P/E trades at 41x, which is above corporate average valuation levels and its own recent history.

High P/Es require high EPS growth to sustain them. In the case of Chifeng Gold, the company has recently shown a 267% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Chinese Accounting Standards (CAS) earnings and convert them to Uniform earnings forecasts. When we do this, Chifeng Gold’s sell-side analyst-driven forecast is a 61% earnings shrinkage in 2020, followed by a 250% earnings growth in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Chifeng Gold’s CNY 18.05 stock price. These are often referred to as market embedded expectations.

In order to justify current market expectations, Chifeng Gold would need to have Uniform earnings grow by 19% each year over the next three years. What sell-side analysts expect for Chifeng Gold’s earnings is below what the current stock market valuation requires in 2020, but well above that requirement in 2021.

The company’s earning power is a little higher than the corporate average. Additionally, cash flows and cash on hand are above its total obligations. Together, this signals a low credit risk.

To conclude, Chifeng Gold’s Uniform earnings growth is below its peer averages in 2020. However, the company is trading above its peer valuations.

About the Philippine Market Daily

“Wednesday Uniform Earnings Tearsheets – Asia-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one company listed in Asia that’s relevant to the Philippines and that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on an Asian company interesting and insightful.

Stay tuned for next week’s Asia company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com