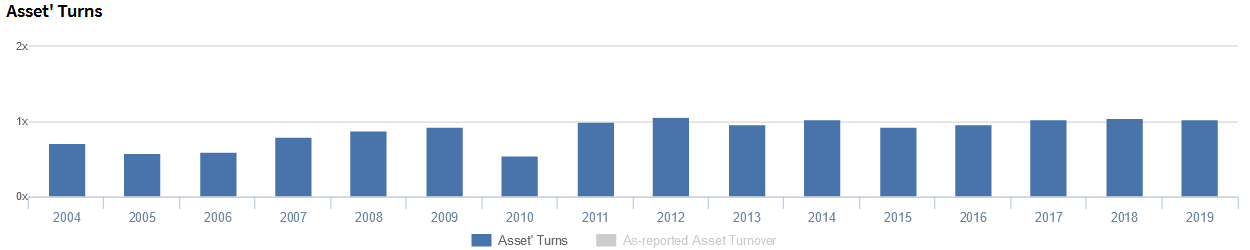

An ambitious management has made this conglomerate more efficient with TRUE asset turnover of 1.0x, not just the 0.7x as-reported metrics see.

Since the implementation of the quarantine, no company has arguably generated more headlines than this industrial conglomerate, in terms of both business and non-business news.

Much of the attention received has been due to the efforts undertaken by the company’s President & Chief Operating Officer.

However, as-reported metrics are downplaying how efficient the business continues to be, leading to an understatement of the firm’s TRUE economic profitability.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

San Miguel Corporation (SMC:PHL) has generated a lot of positive media attention in recent weeks.

The company has guaranteed full compensation with benefits for its more than 66,000 workers. In addition, San Miguel’s medical donations have helped double the country’s COVID-19 testing capacity.

The company even brought back its phased out Nutribun, a nutrient rich bread product, to combat malnutrition and hunger during the pandemic.

Under the directive of its President & COO Ramon Ang, the cost of all of San Miguel’s donations has reached an astonishing PHP 13 billion.

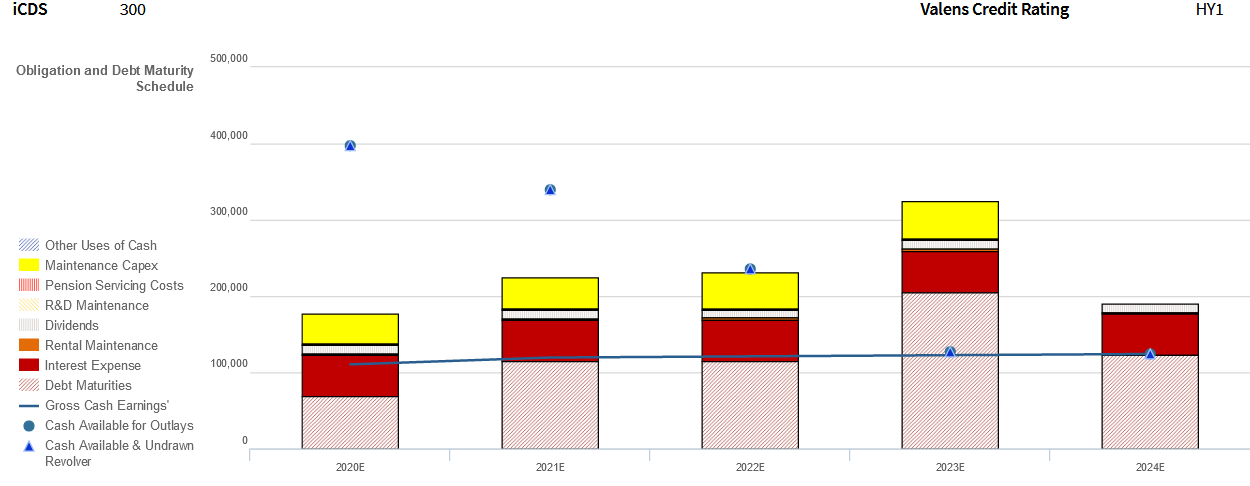

However, many investors and creditors are worried whether the company can sustain further aid. Though the company presently has substantial cash on hand, it does have significant debt obligations within the next five years.

In particular, its 2023 PHP 200 billion debt headwall may be difficult to pay off unless the company refinances its debt. In other words, if San Miguel’s creditors approve the postponement of its debt repayment, the company should have little trouble paying its other obligations in the near term.

Both equity and credit investors have another reason to be concerned about San Miguel’s performance. The company has recently experienced hurdles in its business interests in infrastructure, mainly in its failure to take over Holcim Philippines, Inc. (HLCM:PHL), the Philippine unit of Swiss-based building materials company LafargeHolcim Ltd. (LHN:CHE).

While the acquisition would have raised San Miguel’s debt levels even further, it would have also strengthened its oligopoly in the cement markets of Metro Manila and Central and Northern Luzon.

The major players in these markets are Holcim, Northern Cement, and Eagle Cement (EAGLE:PHL). Northern Cement is separately owned by San Miguel Chairman Eduardo “Danding” Cojuangco Jr., while San Miguel President Ramon Ang also separately serves as the chairman of Eagle Cement.

This has not been the first of COO Ramon Ang’s bold initiatives for San Miguel. Under his tenure, the company has expanded its operations from a mainly food and beverage company into a well-diversified business conglomerate.

The past decade alone has been eventful for San Miguel.

In 2010, the company acquired a majority control of Petron Corporation (PCOR:PHL), which is now the largest petroleum company in the country and San Miguel’s largest source of revenue.

In 2012, San Miguel tested the airline industry by purchasing a 49% stake of PAL Holdings, Inc. (PAL:PHL), only to relinquish its stake two years later.

In 2015, it entered into talks with Australia’s largest telecommunications provider, Telstra Corporation Limited (TLS:AUS), in the hopes of becoming the third largest telecom player in the Philippines. However, both sides couldn’t come to an agreement and San Miguel would later exit the industry by selling its own telecom assets to the other major players.

In 2019, the company made a bid for the PHP 735 billion construction contract of New Manila International Airport. It remains to be seen whether the project would continue as planned, considering construction has already been delayed.

San Miguel investors would have probably gone through a rollercoaster of emotions holding its shares in the past 10 years.

With the company’s half-succeeding and half-failing ventures, one might think that San Miguel has just been burning cash all this time.

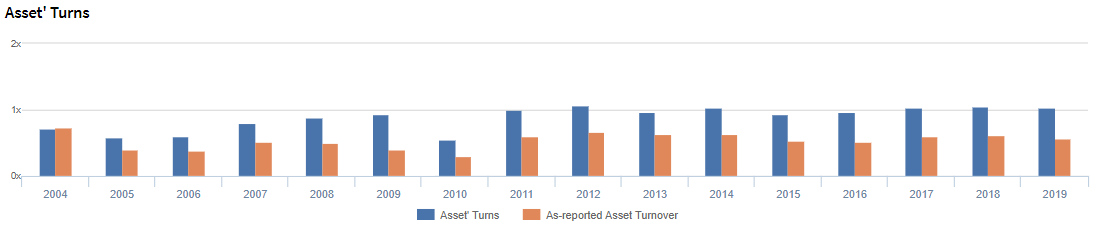

When looking at its as-reported asset turnover, the company doesn’t seem to have improved. In 2019, as-reported asset turnover was at 0.6x, slightly below 2004 levels of 0.7x.

Yet on a Uniform basis, San Miguel’s TRUE asset turns have actually improved, rising from 0.7x in 2004 to 1.0x in 2019.

Furthermore, the company has actually been remarkably consistent following the Petron acquisition, with Uniform turns ranging from 0.9x-1.1x since 2011.

The main reason for such different asset efficiency trends is in its treatment of goodwill. With the multiple acquisitions it has made, San Miguel has accumulated a lot of goodwill, all of which is purely accounting-based and is not actually used in the company’s operations.

In 2019 alone, the firm is holding PHP 130 billion worth of goodwill in the balance sheet, falsely making the company seem less efficient than it actually is.

After removing this item from San Miguel’s asset base and with the many other adjustments Valens makes, we arrive at a 1.0x Uniform asset turns for 2019.

San Miguel is a more efficient business than you think

Historically, as-reported metrics have significantly understated the firm’s asset efficiency.

In 2019, as-reported asset turnover was 0.6x compared to Uniform asset turns of 1.0x, making the company appear to be a less efficient business than real economic metrics highlight.

Moreover, as-reported asset turnover has been lower than Uniform turns each year since 2005.

After falling from 0.7x in 2004 to 0.4x in 2005, as-reported asset turnover slightly recovered to 0.5x in 2007-2008 and subsequently fell to a trough of 0.3x in 2010. As-reported asset turnover then expanded to 0.7x in 2012, before fading to 0.5x-0.6x levels through 2019.

Meanwhile, Uniform asset turns only compressed from 0.7x in 2004 to 0.6x in 2005-2006. Thereafter, Uniform turns steadily improved to 0.9x-1.1x levels from 2008 to 2019, excluding a 0.5x underperformance in 2010.

As-reported asset turnover has been distorting the market’s perception of the firm’s historical asset efficiency levels for more than a decade.

San Miguel’s earning power is stronger than you think

Since asset turnover is a key driver of profitability, as-reported metrics have also understated San Miguel’s profitability.

As-reported ROA was only at 4% in 2019, materially lower than Uniform ROA of 7%, making the company appear to be a less profitable business than what real economic metrics reveal.

Furthermore, as-reported ROA fell from 5% in 2018 to 4% in 2019, whereas Uniform ROA rose from 6% to 7% over the same period. As-reported metrics are directionally distorting the firm’s recent profitability trends.

SUMMARY and San Miguel Corporation Tearsheet

As our Uniform Accounting tearsheet for San Miguel highlights, Uniform P/E currently trades at 19.3x, which is below the market average but near the company’s historical average.

Low P/Es require low EPS growth to sustain them. In the case of San Miguel, the company has recently shown a 51% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for PFRS earnings and convert them to Uniform earnings forecasts. When we do this, San Miguel’s sell-side analyst-driven forecast calls for 52% Uniform earnings growth in 2020, followed by 21% Uniform earnings decline in 2021.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify PHP 96.00 per share. These are often referred to as market embedded expectations.

The company’s Uniform earnings could shrink by about 4% in each of the next three years and it will still meet current market valuations.

What sell-side analysts expect for the company’s earnings growth is significantly above what the current stock market valuation requires.

To conclude, San Miguel’s Uniform earnings growth is the highest among peers in 2020, while the company is trading above peer average valuations.

About the Philippine Markets Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com