Calling all investors! Think this blue chip stock is cheap? The P/E is not 12x, it’s really nearly double that.

First mover advantage is not so much an advantage to the firm who has it, as it is a testing ground for everyone else interested in entering the market.

Firm size is not an indicator of the quality of earnings that they produce.

Market share is not necessarily a barometer of a firm’s stock performance.

Here’s a company that has been considered one of the Philippines’ favorite blue chip stocks, especially with their 7% dividend yield, that is actually trading at more expensive levels based on Uniform ROA.

Philippine Markets Daily:

Tuesday Uniform Earning Tearsheets – Philippine-listed Focus

Powered by Valens Research

In 1928, phone networks in the Philippines worked only within a limited radius, usually only within the barangay or city. If anything were to happen within that city, it was difficult to call for help.

In November 1928, the need to be well-connected among cities became even more apparent.

The most severe typhoon in the Philippines at the time hit the Eastern Visayas region, causing extensive damage to property and life.

Telephone networks couldn’t reach other areas of the Philippines… There was little that could be done to get aid to the area as quickly as possible.

It was then that this 90-year old company was incorporated and given rights to establish and then manage the telephone services in the whole country, under the NY-based firm General Telephone and Electronics Corp. (GTE).

40 years later, Ramon Cojuangco and other Filipino businessmen bought GTE’s stake in the firm, making the company Filipino-controlled.

The Filipino owners sought to achieve one milestone after another, getting into cellular phones and even the early innings of the internet era.

30 years later, First Pacific Co. Ltd., headed by Manuel V. Pangilinan, bought a 17.5% stake in PLDT. He then replaced the president and CEO, who became the chairman of the board.

From 2004, when MVP assumed the chairman of the board seat, until 2008, the stock was up over 270%. Shareholders were enjoying the results of the firm’s investments in wireless telecom and next generation network.

Under this new management style, PLDT looked poised to give back significant returns to their shareholders.

But stock price performance in the last five years shows that their investments in assets may not be entirely paying off.

Diving into the notes of the financial statements pays off, particularly when Uniform Accounting is sending signals that something seems off.

A quick depreciation analysis shows that over the past 12 years, the estimated useful lives for PLDT’s as-reported tangible assets were revised at least 10 times.

Companies can legally adjust asset lives, usually to lengthen the time it takes for the asset to be considered fully depreciated in accounting.

A longer depreciation period means lower depreciation expense per year, which overstates earnings in those years, overstating returns.

The firm is reporting better returns because its depreciated expense is spread out through more years, increasing each year’s reported earnings. On the asset side, as-reported depreciation fails to account for inflation.

Instances of estimate revision have gone down in recent years, but in 2018, the estimated useful life of PLDT’s buildings suddenly doubled up to 50 years. This may be a sign of further legal earnings manipulation in the future, especially when the company is struggling to perform above cost of capital levels.

From the SEC and PFRS perspective, there’s nothing wrong with that.

But from a Uniform Accounting perspective, it’s clear as day that there’s no connection between reported returns and the firm’s REAL profitability.

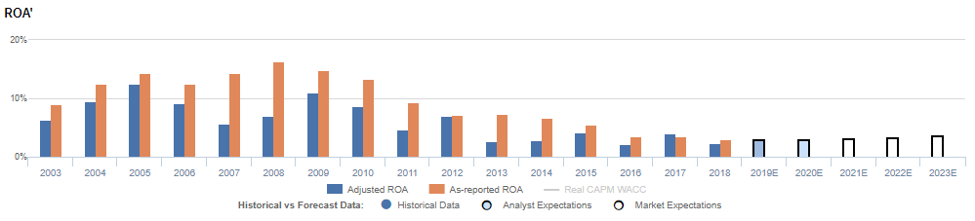

PLDT Inc. Embedded Expectations Analysis – Market expectations are for Uniform ROA to improve slightly to 4%, assuming insignificant Asset’ growth

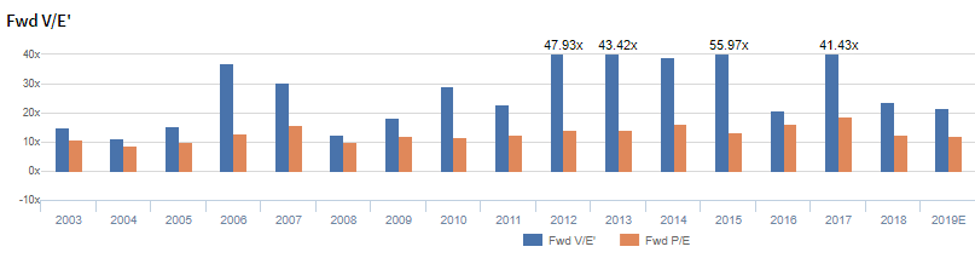

PLDT’s P/E is actually more expensive than you think

PLDT is currently trading at a 21.8x Uniform P/E (blue bars), which is near the low end of historical levels.

Despite valuations having come down from recent highs, PLDT is still not as cheap as the as-reported metrics (orange bars) would lead investors to believe.

At this multiple, the market is pricing in expectations for slight improvement of Uniform ROA, from 2% in 2018 to 4% in 2022, accompanied by 2% Uniform Asset growth.

Analysts have similar expectations, projecting Uniform ROA to increase to 3% in 2019, accompanied by 1% Uniform Asset shrinkage.

PLDT’s earning power is worse than you think

Historically, PLDT has seen volatile profitability, with Uniform ROA ranging from a high of 13% to a low of 2.1% over the past 16 years.

From 2003 to 2012, Uniform ROA remained above cost of capital, ranging from 5% to 13%. As-reported ROAs would have you believe that the company’s most profitable year was 2008, when in reality, that was the poorest quality year during the period.

Earning power then declined to 3% levels in 2013, when the company expanded their asset base and established a fiber-optic network.

Since then, Uniform ROA failed to recover and continued to decline to 2% in 2018.

Meanwhile, Uniform Asset growth has historically been volatile: positive in 11 of the past 16 years, while ranging from -18% to 24%.

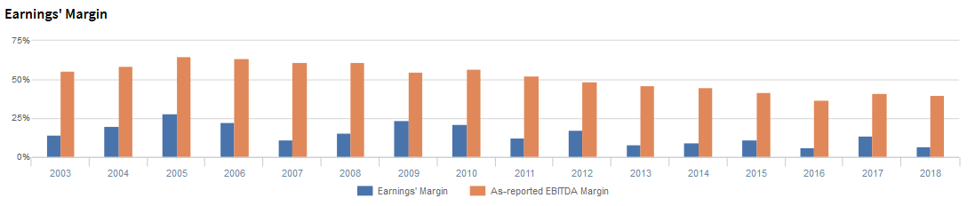

PLDT’s margins are a lot worse than you think

As-reported metrics overstate PLDT margin, one of the main drivers of profitability.

For example, the as-reported EBITDA margin for PLDT was 40% in 2018, far higher than the Uniform Margin of 7%, making PLDT appear to be a much stronger business than real economic metrics highlight.

Moreover, as-reported EBITDA margin has been at least 30% higher than Uniform Margins, significantly distorting the market’s perception of the firm’s historical profitability levels.

PLDT Inc. Tearsheet

As our Uniform Accounting tearsheet for PLDT Inc. highlights, PLDT trades around market average valuations. The company has recently had -70% Uniform EPS growth, which is forecast to increase to 88% in 2019, and 3% in 2020. At current valuations, the market is pricing the company to see earnings grow by 5% a year going forward.

to increase to 88% in 2019, and 3% in 2020. At current valuations, the market is pricing the company to see earnings grow by 5% a year going forward.

The company’s earnings growth is forecast to be above peers in 2019, but the company is trading only in line with peer average valuations. The company has low returns relative to current corporate averages, but has cash flow risk to their strong dividend.

About the Philippine Market Daily

“Tuesday Uniform Earning Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing himself, Benjamin Graham.

Warren Buffett and Charles Munger of Berkshire Hathaway; David Sanford Gottesman of First Manhattan Co.; Walter Schloss of WJS Partners; William Ruane of Ruane Cuniff, Sequoia Fund; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios.

But what sets them apart from everyone else who also uses financial statements and valuation to choose their investments?

These great investors don’t rely on as-reported numbers.

“… although accounting is the starting place, it’s only a crude approximation.” – Charlie Munger

“… the net earnings figure… it really is not representative of what’s going on in the business at all.” – Warren Buffett, Opening Remarks, the 2018 Berkshire Hathaway Annual Shareholders Meeting

“GAAP rules… I’ve warned you about the distortions. The bottom line figures… totally capricious. It’s really a shame.” – Warren Buffett, Opening Remarks, the 2019 Berkshire Hathaway Annual Shareholders Meeting

“Generally Accepted Accounting Principles are not truth or reality.” – Marty Whitman

Due to the multiple distortions and miscategorizations in Philippine Financial Reporting Standards (PFRS), investors are often unable to properly analyze companies in an apples-to-apples comparison.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

The goal of UAFRS is to create more reliable and comparable reports of corporate financial activity.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com