Can a stock really be recession-proof? The maker of SPAM proves that it can come out of a financial crisis with even stronger ROAs than before!

In 2009, global markets and economies were shaken as credit crashed, and along with it, stocks.

However, not all industries came down with the fall. One industry, in particular, stood its ground fairly well: Consumer Staples.

Businesses in this industry typically sell the essentials: your toiletries, canned goods, and beverages. Demand for these products remains robust during recessions because people need them for everyday living.

Today, another threat of a recession looms over the horizon, this time over concerns about the impact of the coronavirus. Will portfolios stand to gain by adding consumer staple stocks to the mix?

This company is in the business of selling food products, including SPAM. It survived the 2008 recession with stock returns and profitability that climbed higher from pre-crisis levels, proving that stocks in this industry do have its advantages after all.

Though as-reported metrics may understate the true potential of their products, TRUE UAFRS-based (Uniform) analysis shows that this company can weather any economic crisis.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

“House Rejects Financial Rescue, Sending Stocks Plummeting,” a headline in 2008 reads.

The financial crisis in the late 2000s proved one thing true: the stock market will always take a plunge during a recession.

When the economy starts to weaken, unemployment goes up, capital spending is cut, general demand for goods and services falls, and debt lending tightens.

The combination of these factors contributes, broadly, to a decline in revenues, profits, and overall company growth. In other words, the operational future of businesses weakens and becomes even more uncertain.

With most valuation methods relying on future cash flows, you’d expect that stock prices would fall as calculated intrinsic values do the same.

But you might be wondering, “are any of the stocks in my portfolio safe?” If you’re holding recession-proof stocks, the answer is yes.

Although there are no guarantees about future performance, these stocks are generally resilient against financial market shocks.

One crucial characteristic of these is that they’re consumer essentials—people are going to buy their products regardless of the economic situation.

These businesses, often in the consumer staples and healthcare industry, will see their demand fall less, and in most cases, even rise, relative to everyone else.

Consumer staples are especially able to stand their ground against downturns.

This sector includes companies that focus on producing goods used on a daily basis such as household goods, personal hygiene goods, retail products, and self-care products.

People aren’t going to stop buying canned goods or using shampoo or toilet paper just because they’re in the middle of a crisis and are cutting costs.

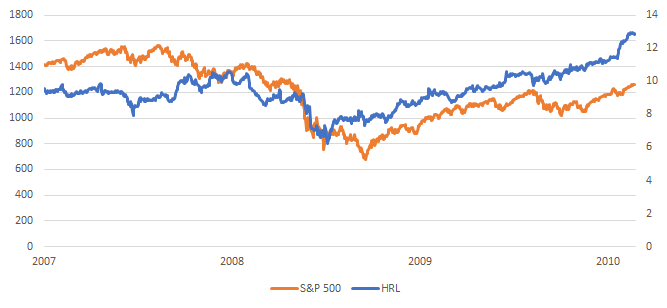

One such company, Hormel Foods Corp., did fairly well during the 2008 Financial Crisis.

While the S&P 500 lost almost 21% in the beginning of 2007 until the end of 2009, Hormel gained 1% over the same time period.

Including the pre- and post-recession periods, the stock gained over 32% from 2007-2010, when the market was crawling towards a recovery, while the S&P 500 returns were still in the negatives.

Hormel is a producer of packaged and refrigerated foods including well-known brands, SPAM and Skippy.

At a time when consumers’ budgets are slashed and costs are rising, people turn to inexpensive food options like SPAM.

Canned goods are particularly in demand during economic crises because of how affordable they can get. They become even more valuable during periods of greater uncertainty such as wartime, and more recently, a pandemic.

While governments are scrambling to contain the coronavirus, economies and financial markets are operating at a controlled rate.

To prevent the spread of COVID-19, some parts of the Philippines are already on lockdown, as well as other cities across the globe. Malls are closed. Office hours are limited. The streets are empty.

Over the past month, people have been going to the grocery stores to stock up on food because they’re afraid that if they don’t, they’ll starve.

In the food section, canned goods are obviously the first ones to go, with SPAM unsurprisingly flying off the shelves. That and other goods like corned beef and luncheon meat, which are also products of Hormel-Purefoods (now owned by San Miguel), are on people’s grocery lists.

The reasoning is simple: these products have an incredibly long shelf-life. This, coupled with inexpensiveness, are what drives the stability of product demand and revenues, and consequently, the company’s stock.

This is why it’s recession-proof.

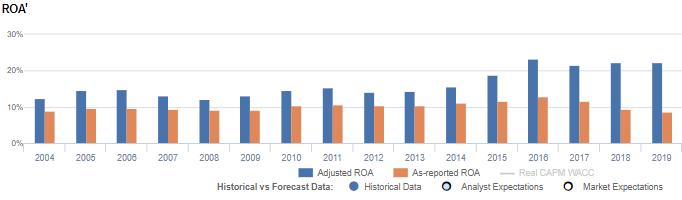

As proof, Hormel’s Uniform return on assets (ROA) during the peak of the recession in 2008 all the way up to the recovery period in 2010 increased from 12% to 15%.

Compare that to the performance of recession-sensitive companies like Winnebago (WGO), an RV manufacturer, or Builders FirstSource (BLDR), a supplier of building materials, who suffered massive drops in Uniform ROA during the same time period.

So the next time you’re building your stock portfolios, Hormel might be one to consider.

Hormel’s earning power is still actually more robust than you think

As-reported metrics significantly understate Hormel Foods Corporation’s (HRL:USA) profitability.

For example, as-reported ROA was 9% in 2019, far lower than Uniform ROA of 22%. Uniform ROA has been higher than as-reported ROA in the past sixteen years. As-reported ROA is making the company look like a weaker business than real economic metrics highlight, distorting the market’s perception of the firm’s historical profitability trends.

Moreover, as-reported ROA has decreased from 12% in 2017 to current 9% levels, while Uniform ROA remained flat at 22% levels over the same period, significantly distorting the market’s perception of the firm’s historical profitability trends.

Historically, Hormel has seen robust and generally improving profitability. Uniform ROA ranged from 12%-15% from 2004 to 2013. Since then, Uniform ROA has jumped to a peak of 23% in 2016 and slightly decreased to 22% in 2019.

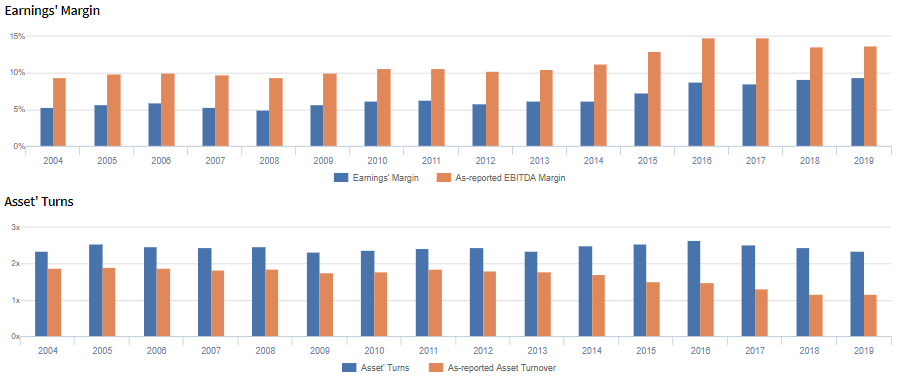

Hormel’s Uniform ROA is driven by robust Uniform asset turns but is offset by Uniform earnings margins

Trends in Uniform ROA have largely been driven by trends in Uniform asset turns offset by trends in Uniform earnings margins.

From 2014-2016, Uniform earnings margins improved markedly from 6% to 9%, before stabilizing to 9% levels in 2019. Meanwhile, after falling from 2.3x in 2013 to 2.7x in 2016, Uniform asset turns stabilized to 2.4x levels in 2019.

At current valuations, markets are pricing in expectations for both Uniform earnings margins and Uniform asset turns to climb to new peaks.

SUMMARY and Hormel Foods Tearsheet

As the Uniform Accounting tearsheet for Hormel Foods Corp. highlights, the Uniform P/E trades at 26.9x, which is above corporate average valuation levels and its own recent history.

High P/Es require high EPS growth to sustain them. In the case of Hormel, the company has recently shown a 4% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Hormel’s Wall Street analyst-driven forecast is a decline of 3% into 2020 that rebounds to 5% into 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Hormel’s $42 stock price. These are often referred to as market embedded expectations.

In order to justify current stock prices, the company would need to have Uniform earnings grow by 4% each year over the next three years. What Wall Street analysts expect for Hormel’s earnings growth is in line with what the current stock market valuation requires.

The company’s earning power is 4x the corporate average. Also, cash flows are about 2x their total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit risk and dividend risk.

To conclude, Hormel’s Uniform earnings growth is in line with peer averages in 2020. Also, the company is trading above average peer valuations.

About the Philippine Market Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com