Charged by the power of Goku and the Power Rangers, this company’s earning power is stronger than the below corporate average reported!

In the Philippines, kids and kids at heart get entertained with superheroes and anime series, as they are shown on our local TV networks in almost all days of the week.

This company produced the biggest Japanese superhero and anime series that may have been a part of our childhood. Most of us continue to patronize these shows today.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Wednesday Uniform Earnings Tearsheets – Asia-listed Focus

Powered by Valens Research

They say you shouldn’t fix something that isn’t broken. That’s why in the media content industry, you’ll see reboots and rehashes of stories and characters that have enjoyed tremendous success in their respective areas.

If a movie or a series became immensely popular and profitable, other companies scramble to buy the rights to distribute or produce similar content, banking on its potential to recreate this success in another market.

A great example of this is Power Rangers. This American TV franchise owes its success to the success of another show.

Power Rangers has been around since 1993 and is still being aired on television. Most millennials will say that this is one of the first shows they have followed as a kid.

What a lot of people don’t know is that it is actually based on a Japanese series called Super Sentai, a show about a team of ordinary people who transform into superheroes and save the world against monsters.

The show’s popularity is undeniable, having more than 40 series since 1975, and new episodes are still being produced today. The latest series, Mashin Sentai Kiramager, began airing last Sunday, March 8, 2020.

What made this series stand out is its filming style, called tokusatsu, that heavily uses special effects. This kind of entertainment is commonly ideal for fantasy, science fiction, and horror genres.

When Saban Entertainment, known for localizing Japanese shows for Western audiences, produced Power Rangers, they bought the rights from Toei to use Super Sentai’s footage, especially for the tokusatsu combat scenes.

As evidenced by the popularity of the show, this move was a complete success.

Decades passed and the Power Rangers franchise had been bought and passed on from one company to another a couple of times.

These companies have been riding on the success of the original tokusatsu maker and creator of Super Sentai.

Toei does not only produce tokusatsu, but they also produce animated films and series, collectively known as “anime.”

Some of the most popular animes produced by Toei are Mazinger Z, Saint Seiya, Sailor Moon, Dragon Ball, and One Piece.

In fact, Toei’s total number of productions exceeds 10,000 episodes, which makes them the largest anime library holder in Japan, and one of the largest in the world.

In producing their animes, their goal is to encourage kids around the globe to hope and dream. This is one of the main reasons why they strive to create animated content that’s better than ever.

As a result of high-quality content, they were able to transform their production business to one that earns a lot from licensing their content all over the world.

Among Toei’s top-earner anime is Dragon Ball.

Son Goku started his adventure on TV in 1986, but until now, Toei is still producing sequel after sequel of his quests. The latest series is called Dragon Ball Super.

This classic anime never lost its ability to charm viewers. Dragon Ball Super’s domestic licensing between April 2018 and March 2019 earned ¥8.55 billion. Its overseas film sales came in at ¥3.52 billion in the same time frame.

Other top-selling animes overseas by Toei are One Piece and Saint Seiya.

Toei’s success in selling the rights and licenses of their live-action tokusatsu and animated series is reflected in their Uniform earning power.

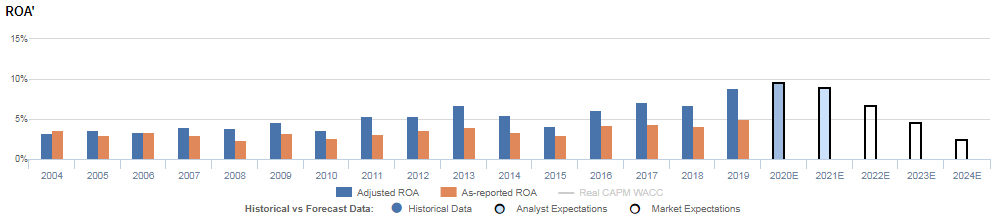

The company’s Uniform ROA has been consistently higher than as-reported ROA in the past 15 years. Toei’s Uniform ROA is 9% in 2019, stronger than the as-reported ROA of 5%.

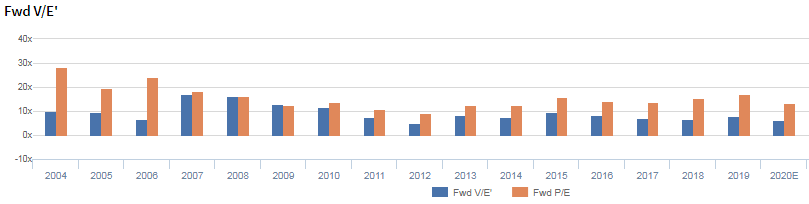

Toei Company is cheaper than you think

Toei Company, Ltd. (9605:JPN) currently trades well below corporate and around historical averages with a 6.6x Uniform P/E (blue bars), which is below the as-reported P/E of 13.8x (orange bars).

At these levels, the market is pricing in expectations for Uniform ROA to decline to 3% in 2024, accompanied by a 5% Uniform asset growth going forward.

However, analysts project Uniform ROA to remain at 9% levels in 2021, accompanied by a 1% Uniform asset shrinkage.

Toei Company’s profitability is actually better than you think it is

Toei Company’s Uniform ROA ranged from 3% to 9% over the past 16 years.

After remaining at 3%-5% levels from 2004-2012, Uniform ROA rose to 7% in 2013, before slowly decreasing to 4% in 2015. Afterwards, Uniform ROA rose to 7% again in 2018, before peaking at 9% in 2019.

Meanwhile, Uniform asset growth has been positive for seven of the past 16 years, while ranging from -13% to 28%.

As-reported metrics are understating Toei Company’s profitability.

For example, as-reported ROA was 5% in 2019, materially lower than Uniform ROA of 9%, making the company look like a weaker business than real economic metrics highlight.

Moreover, Uniform ROA has been higher than as-reported ROA for the past 15 years, significantly distorting the market’s perception of the firm’s historical profitability trends.

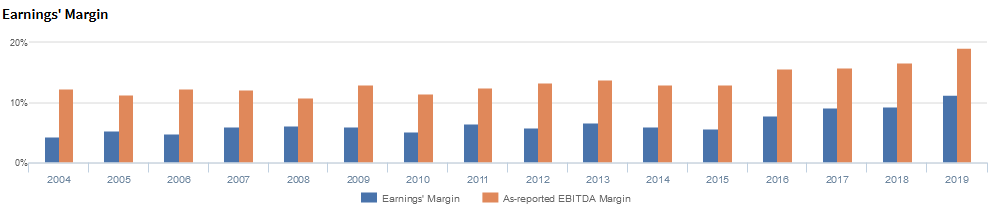

Toei Company’s margins are weaker than you think

Cyclicality in Uniform ROA has been driven primarily by trends in Uniform EBITDA margin, with peaks and troughs lining up historically with that of Uniform ROA.

Uniform EBITDA margin increased from 4% in 2004 to 7% in 2011, before falling to 6% in 2015. Thereafter, Uniform EBITDA margin rose to a historical high of 11% in 2019.

Summary and Toei Company Tearsheet

As the Uniform Accounting tearsheet for Toei Company highlights, they are trading at 6.6x Uniform P/E, which is well below market average valuations and around historical average levels.

Low P/Es require low EPS growth to sustain them. In the case of Toei Company, the company has recently shown a 31% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Japan’s Modified International Standards (JMIS) earnings and convert them to Uniform earnings forecasts. When we do this, Toei Company’s sell-side analyst-driven forecast is for Uniform earnings to grow by 13% in 2020 and shrink by 11% in 2021.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify JPY 12,580.00 per share. These are often referred to as market embedded expectations.

In order to meet the current market valuation levels of Toei Company, the company would have to have Uniform earnings shrink by 20% each year over the next three years. What sell-side analysts expect for Toei Company’s earnings growth is well above what the current stock market valuation requires.

To conclude, Toei Company’s Uniform earnings growth is below peer averages in 2020. However, the company is trading around peer average valuations.

The company’s earning power, based on its Uniform return on assets calculation, is greater than corporate average returns. Furthermore, with cash flows and cash on hand consistently exceeding obligations, Toei Company has low credit and dividend risk.

About the Philippine Market Daily

“Wednesday Uniform Earnings Tearsheets – Asia-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one company listed in Asia that’s relevant to the Philippines and that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on an Asian company interesting and insightful.

Stay tuned for next week’s Asia company highlight!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com