Crafting its business through acquisitions and a spin-off made this food company achieve Uniform ROAs of 40%+

Companies often engage in mergers and acquisitions in the hopes of capturing synergies that would increase firm value. This company made an acquisition, which it eventually spun off, and a merger deal that made it the fifth largest food business in the world.

Both of these transactions significantly expanded the brand portfolio and the market reach of its snacks business and its core grocery foods business.

However, while as-reported data suggests that the merger and acquisition have only destroyed company value, Uniform Accounting shows that the firm has actually achieved the synergies it was expecting, with returns having gone up to new highs of 40%.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

Maximizing shareholder wealth has long been the fundamental pillar of corporate finance. However, not a lot of management teams do that. Some misspend capital that could potentially be used for higher value-generating projects, and some even misspend to the point of value destruction.

This is where activist investors come in.

Activist investors purchase a significant stake in the company they perceive as undervalued and pressure management into implementing their value-creating strategies. These strategies could take the form of share buybacks, mergers, acquisitions, divestitures, or even downright just selling the company.

There have been many cases of activist investing at play, and among the more popular ones was the case involving Kraft Foods. Nelson Peltz, the Founding Partner of Trian Capital Management, staged the Kraft intervention in 2009.

Peltz pushed then CEO Irene Rosenfeld to launch a hostile bid for Cadbury, who actively resisted the offer. Kraft initially proposed a price of 745 pence (or around $9) per share, which was then deemed as unattractive because it “fundamentally undervalued” the company.

Eventually, in the following year, a deal was struck between the two companies. A majority of Cadbury’s shareholders approved a takeover price of 840 pence (or around $11), including a 10 pence special dividend to sweeten the deal.

The main reason for Kraft’s acquisition of Cadbury was to provide scale for its snacks business as it planned to expand its reach outside of North America, particularly in emerging markets.

However, Kraft was more focused on grocery items while Cadbury focused on snacks, and management knew that they were running two different businesses in terms of growth rates, and in the strategies and capital requirements needed to accommodate that growth.

Kraft had higher margins but slower, stable growth, while Cadbury, the international snacks business, offered higher growth. So, in 2012, Cadbury (renamed Mondelez) was spun off, with management expecting that it would take advantage of the more expansive growth in international markets.

Both companies remained focused on their core businesses. Kraft kept the familiar grocery brands such as Jell-O and its namesake Kraft brands, and Cadbury kept Oreo, Nabisco, Cadbury, and other snack brands.

While Kraft succeeded in the expansion of its snack foods business through the acquisition and subsequent spin off of Cadbury, the company was back to being the stable, slow-growth business that it was.

That is, until 2015, when it decided to merge with H.J. Heinz Company to create the fifth largest food company in the world. The new company, Kraft Heinz (KHC), combined two iconic portfolios of grocery brands including Velveeta, Ore-Ida, and of course, Kraft and Heinz, among others.

Kraft derived about 98% of its revenues from North America. Heinz, on the other hand, had a wider market footprint, deriving only 40% of its revenues from North America, with the other 60% coming in from international markets.

The merger was perfect for Kraft. It was an opportunity for the company to expand its grocery business’ market reach and accelerate growth similar to how it expanded its snacks business with the Cadbury acquisition.

After the merger, however, the company came under immense pressure from the government and its stakeholders. Securities regulators were investigating the company for possible accounting fraud and for employee misconduct, all while shareholders were filing numerous lawsuits.

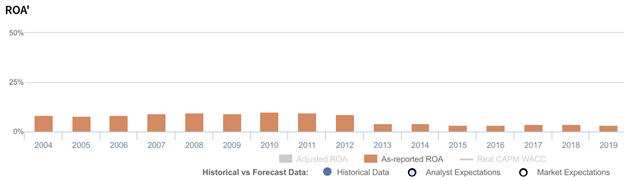

Most investors only saw the merger as a failure, and as-reported metrics show exactly that.

As-reported ROAs fell more than half from 9% in 2012 to just 4% in 2013, a year after the Cadbury spin off. This highlighted how the company had slower growth without the snacks business. In 2015, following the merger, ROAs dropped further to 3%.

In reality, looking at Uniform ROAs shows investors that the spin off and the merger actually created value for the company. Uniform ROAs rose from 19% in 2012 to 26% in 2013, and has climbed steadily to about 40% post-merger—a stark contrast to what as-reported metrics would have investors believe.

The merger did in fact achieve the synergies Kraft was hoping to get. It expanded the company’s portfolio of brands, as well as its international presence. This, in turn, created more revenues and higher returns.

The huge distortion between Uniform and as-reported ROAs, furthermore, can be explained from as-reported metrics failing to consider the amount of goodwill on Kraft Heinz’s balance sheet. In recent years, goodwill averaged about $35 billion or a third of its total assets, due to the company’s mergers and acquisition activities.

Goodwill is an intangible asset that is purely accounting-based and unrepresentative of the company’s actual operating performance. When as-reported accounting includes this in a company’s balance sheet, it creates an artificially inflated asset base.

As a result, as-reported ROAs are not capturing the strength of Kraft Heinz’s earning power. Adjusting for goodwill, we can see that the company didn’t make value destroying decisions. In fact, it has been the opposite, with returns that have become nearly 11x greater.

Kraft Heinz’s earning power is actually more robust than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

Kraft Heinz’s Uniform ROA has actually been higher than its as-reported ROA in the past sixteen years. For example, as-reported ROA was 3% in 2019, but its Uniform ROA was actually over 13x higher at 42%.

Specifically, Kraft Heinz’s Uniform ROA has ranged from 16%-44% in the past sixteen years while as-reported ROA ranged only from 3%-10% in the same timeframe.

After maintaining 16%-21% levels in 2004-2012, Uniform ROA gradually expanded to a peak of 44% in 2016 slightly compressing to 42% in 2019.

Kraft Heinz’s Uniform earnings margins are weaker than you think, but its robust Uniform asset turns make up for it

Kraft Heinz’s overall improvements in profitability has been driven by trends in Uniform asset turns and Uniform earnings margins.

From 2004-2015, Uniform turns ranged between 1.5x-1.8x, before expanding to a peak of 3.1x in 2018 and subsequently fading to 2.8x in 2019.

Meanwhile, Uniform margins remained at 11%-12% levels from 2004-2012, before jumping to a peak of 25% in 2015. Since then, Uniform margins have regressed to 15% in 2019.

At current valuations, markets are pricing in an expectation for Uniform turns to decline and for Uniform margins to stabilize near current levels.

SUMMARY and Kraft Heinz Tearsheet

As the Uniform Accounting tearsheet for the Kraft Heinz Company (KHC) highlights, the Uniform P/E trades at 18.8x, which is below corporate average valuation levels and its own recent history.

Low P/Es require low EPS growth to sustain them. In the case of Kraft Heinz, the company has recently shown a 2% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Kraft Heinz’s Wall Street analyst-driven forecast is a 22% EPS contraction in 2020, followed by a 24% EPS growth in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Kraft Heinz’s $29 stock price. These are often referred to as market embedded expectations.

The company can have Uniform earnings shrink by 3% each year over the next three years and still justify current prices. What Wall Street analysts expect for Kraft Heinz’s earnings growth is below what the current stock market valuation requires in 2020, but above the requirement in 2021.

Furthermore, the company’s earning power is 7x the corporate average. However, cash flows and cash on hand are lower than its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a high credit and dividend risk.

To conclude, Kraft Heinz’s Uniform earnings growth is below its peer averages in 2020 and the company is also trading below its average peer valuations.

About the Philippine Markets Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com