Innovating on digital transformation helped this company become the leading general contractor, building stronger Uniform ROAs than you think

When you think about construction, the first thing you might think of is a hard job on site. However, the construction industry involves everything from the initial planning of a project all the way to the painting of the walls.

As the biggest general contractor in the Philippines, this company uses Building Information Modeling (BIM) to develop siteworks efficiently by reusing materials for future projects.

However, as-reported metrics consistently show lower profitability in the last ten years, compared to what Uniform metrics portray.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

The construction industry plays a significant role in supporting a country’s economic growth through its infrastructure projects, especially for developing countries. It not only generates new job opportunities but also offers solutions to address social, climate, and energy challenges.

As a developing market itself, the Philippines’ growth is also tied with the country’s construction spending. Since the Duterte administration started its “Build! Build! Build!” program in 2016, spending on infrastructure development has expanded to 5% of GDP, which is double its average expenditure over the last 50 years.

The total budget for the program was set at PHP 4.3 trillion for a total of 100 projects, 46 of which are ongoing until 2022.

EEI Corporation (EEI:PHL), one of the largest general contractor companies in the country, is one of the bidders in these government infrastructure and construction projects.

The company services both local and overseas markets by supplying manpower for construction services, construction, installations, and erection of different facilities that generate power for both public and private companies.

EEI Corporation was established in 1931 as a machinery and mills supply house, but eventually fully equipped the machine shop to handle general machine work, steel fabrication, and welding.

By the 1940s, the company had expanded into metal works and shipbuilding. It also won contracts to fabricate the chassis of Manila’s garbage trucks and to construct the Philippine Coast Guard’s vessels.

The company further developed its engineering shop facilities and entered the power development business in the 1950s.

From the 1960s to 1980s, the company continued to grow, operating three main divisions: construction, machinery, and foundry. Through the firm’s continued expansion, EEI Corporation was able to build subsidiaries in the 1990s, which were designed to support the growth of Middle Eastern and Asian markets for construction services.

In the 2000s, EEI Corporation started to acquire major projects overseas, particularly for the Kingdom of Saudi Arabia. On the domestic front, the firm acquired more high-rise building and infrastructure projects.

To further strengthen its position in the construction industry, EEI Corporation deployed key technologies, particularly Building Information Modeling (BIM). This technology helped the company develop siteworks more efficiently by reusing material for future projects.

The company’s growth initiatives over the years has made it one of the leading contractors in the country at present, with its quadruple-A rating as a General Engineering Contractor – the highest category rating for contractors.

However, just like others in the construction industry, EEI Corporation was negatively affected by building restrictions due to the pandemic. Unlike other industries, the company’s workers could not work from home. Moreover, since construction was halted in the early part of the quarantine period, the firm could not finish projects and collect revenue.

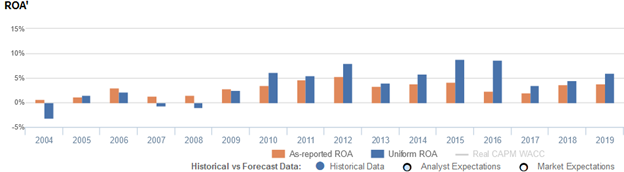

Taking a look at the company’s returns before the pandemic, we see a company generating above cost of capital returns using Uniform Accounting. On the other hand, as-reported metrics suggest that the company has not been profitable in the past sixteen years.

For example, according to as-reported metrics, EEI Corporation posted a 4% ROA in 2019, whereas by looking at Uniform metrics, TRUE earning power is actually higher at 6%.

One of the said distortions for the discrepancy is due to the treatment of non-operating long-term investments according to the Philippine Financial Reporting Standards (PFRS).

Based on PFRS, non-operating long-term investments are part of the company’s balance sheet, but in reality, non-operating long-term investments are not essential to the firm’s assets and should be removed from the total assets.

For example, in 2019, EEI Corporation recognized a non-operating long-term investment of PHP 3.8 billion, accounting for 14% of its as-reported total assets of PHP 28 billion.

After removing the PHP 3.8 billion from the asset base and with the many other adjustments Valens makes, we arrive at a TRUE earning power of 6%.

EEI Corporation’s earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s profitability. If you were to just look at as-reported ROA, you would think EEI Corporation’s profitability has been weaker than real economic metrics have highlighted in the past ten years.

In reality, EEI Corporation’s true profitability has been higher than as-reported ROA claims since 2010. Specifically, as-reported ROA was only 4% in 2019, but Uniform ROA was actually 6% that year.

After expanding from 3% in 2010 to 5% in 2012, as-reported ROA gradually declined to 2% in 2016, before recovering to 4% in 2018-2019.

Meanwhile, after improving from 6% in 2010 to 8% in 2012, Uniform ROA dropped to 4% in 2013, before peaking at 9% in 2015-2016. Thereafter, Uniform ROA fell to 4% in 2017, before expanding to 6% in 2019.

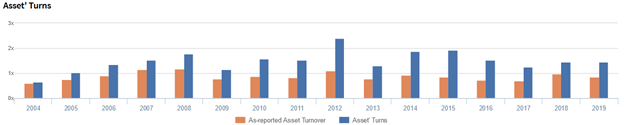

EEI Corporation’s asset turns are stronger than you think

Strength in EEI Corporation’s Uniform ROA has been driven by strong Uniform asset turns. In fact, Uniform turns have been higher than as-reported asset turnover in each of the past fifteen years.

After reaching its peak at 1.2x in 2008, as-reported asset turnover had slowly declined from 0.7x in 2017, before recovering to 0.8x-1.0x levels in 2018-2019.

Meanwhile, Uniform turns expanded from 0.7x in 2004 to a high of 2.4x in 2012, before gradually compressing to 1.2x in 2019.

Looking at the firm’s turns alone, as-reported metrics are making the firm appear to be a less asset efficient business than is accurate.

SUMMARY and EEI Corporation Tearsheet

As the Uniform Accounting tearsheet for EEI Corporation (EEI:PHL) highlights, the Uniform P/E trades at 13.3x, which is below corporate averages and its own history.

Low P/Es require low EPS growth to sustain them. In the case of EEI Corporation, the company has recently shown a 6% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, EEI Corporation’s sell-side analyst-driven forecast calls for a 23% and 1% Uniform EPS growth in 2020 and 2021, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify EEI Corporation’s PHP 7.51 stock price. These are often referred to as market embedded expectations.

The company can have Uniform earnings shrink by 6% each year over the next three years and still justify current valuations. What sell-side analysts expect for EEI Corporation’s earnings growth is above what the current stock market valuation requires in 2020 and 2021.

Furthermore, the company’s earning power is near the long-run corporate average, but cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals high credit risk.

To conclude, EEI Corporation’s Uniform earnings growth is above peer averages, but the company is also trading around peer average valuations.

About the Philippine Markets Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com