IT’S A MATCH! The country’s largest equity fund finds new home at the country’s largest investment house

AIA Philam Life is transitioning its subsidiary, Philam Asset Management, Inc. (PAMI) into a trust company to focus on managing Philam group’s investment portfolio.

This indicates that PAMI has to transfer all its existing mutual funds, which include the largest equity fund in the country, to BPI Investment Management, Inc. (BIMI), the country’s largest mutual fund manager.

We look at the Philippines’ largest equity fund to determine the underlying earning power of its major holdings and see how this fund fares with respect to BIMI’s investment objectives.

The results are unsurprising. Using as-reported financial metrics, the investments in this fund’s portfolio looks average. However, in reality, UAFRS-based financial metrics show above average returns and significant growth potential.

In addition, we dig through one of the funds largest holdings, providing you with the current Uniform Accounting Performance and Valuation Tearsheet for that company.

Philippine Markets Daily:

Friday Uniform Portfolio Analytics

Powered by Valens Research

AIA Philam Life is a household name in the insurance industry. They aim to innovate their solutions to effectively address the protection and wellness needs of their existing and prospective customers.

Last year, the firm decided to renew their focus on their core insurance operations.

In line with this, Philam Life announced on November 20, 2019 that it will transform its wealth management arm, Philam Asset Management, Inc. (PAMI) into a trust corporation.

Philam Life, through this trust corporation, will bring AIA’s investment expertise and best practices to the field. It will leverage AIA’s investment framework and business model in managing the Philam Group’s portfolio of general and variable-unit linked (VUL) funds.

During this transition period, PAMI will be turning over all of its contracts, agreements, and existing mutual funds to BPI Investment Management, Inc. (BIMI), the Philippine’s largest mutual fund manager in terms of assets under management.

PAMI’s mutual funds include the largest equity mutual fund in the Philippines, the Philam Strategic Growth Fund, which has PHP 34 billion worth of assets under management.

Just last month, BIMI officially took the helm of all nine PAMI funds. In other words, the country’s largest fund manager will now run the country’s largest equity fund.

BIMI currently manages more than PHP 580 billion worth of assets from its individual and institutional investors. The addition of PAMI funds would expand BIMI’s investment products and enable the firm to reach clients beyond their existing universe.

The firm’s investment decision-making process is grounded on heavy fundamental research that focuses on intrinsically undervalued companies with long-term growth potential.

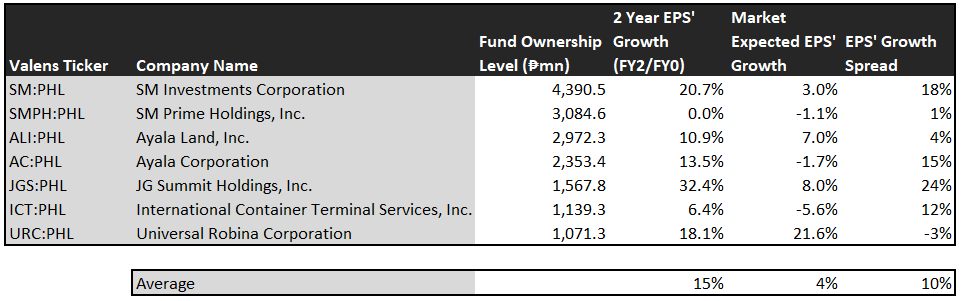

At first glance, the top non-financial holdings of Philam Strategic Growth Fund, as shown above, appear to be low-performing firms and may not be the type of companies BIMI would look into.

Looking solely at the as-reported return on assets (ROA), which can be found in various financial databases, you may wonder why most of these companies were chosen in the first place since their returns are below the cost-of-capital levels.

However, the Uniform ROA paints a different picture.

Based on Uniform Accounting, the ROA’ of these companies range from 7% to 28%. Contrary to what as-reported numbers suggest, these companies are actually profitable with real earnings above cost-of-capital levels.

As such, it should not be surprising that when analyzing the non-financial holdings of Philam Strategic Growth Fund, the figure that stands out is the huge discrepancy between ROA’ and as-reported ROA.

While the difference in raw figures may not seem too distant, the distortion in percentage ranges from 30% to 337%, with International Container Terminal Services (ICT:PHL) and Ayala Corporation (AC:PHL) both having distortions greater than one hundred percent.

As-reported numbers indicate that ICT is just an average company with ROA of 6%. However, when accounting distortions are removed, ICT has stronger profitability with 28% Uniform ROA. In fact, the country’s leading terminal operator has consistently generated Uniform ROAs of 20% or above over the past decade.

Furthermore, as-reported accounting distort not just profitability but a company’s earnings growth as well as shown above. This table has three interesting data points:

– The first datapoint is what Uniform earnings growth is forecast to be over the next two years when we take consensus analyst estimates and convert them to the Uniform Accounting framework. This represents the Uniform earnings growth the company is likely to have for the next two years

– The second datapoint is what the market thinks Uniform earnings growth is going to be for the next two years. Here, we are showing how much the company’s Uniform earnings need to grow in the next two years to justify the current stock price of the company. This is the market’s embedded expectations for Uniform earnings growth

– The final datapoint is the spread between how much the company’s Uniform earnings could grow if the Uniform earnings estimates are right, and what the market expects Uniform earnings growth to be

On average, Philippine companies are expected to have 6% annual Uniform earnings growth over the next few years. Meanwhile, Philam’s major holdings are forecast to surpass that with 15% projected Uniform earnings growth in the next two years. The market, meanwhile, is expecting these companies to expand by 4% a year, understating their growth by an average of 10%.

These are the kinds of companies that have growth potential.

Without Uniform numbers, the as-reported numbers would leave everyone confused.

Among Philam’s top investments, JG Summit Holdings, Inc. (JGS:PHL) has the highest Uniform earnings growth dislocation. Market is pricing this conglomerate to grow by 8% in the next two years. Meanwhile, the analysts are seeing robust 32% Uniform earnings growth.

Another company with understated earnings growth is ICT. The market is pricing the country’s leading port management company to shrink by 6% in the next two years. On the other hand, the analysts are seeing 6% Uniform earnings growth, fueled by the firm’s capacity expansion efforts and new shipping contracts across the Oceania region.

Meanwhile, there is one company in the portfolio that Philam may need to take another deeper review—SM Prime Holdings, Inc. (SMPH:PHL). The market is pricing SMPH to have 1% earnings shrinkage moving forward. Analysts are a little less bearish forecasting flat earnings growth annually. This doesn’t look like an intrinsically undervalued company.

With an average as-reported ROA of 5% and market-expected earnings growth of 4% annually, one might think that this portfolio has subpar returns with minimal growth prospects, which does not match BIMI’s investment philosophy.

However, looking through the lens of Uniform Accounting, for the most part, the Philam Strategic Growth Fund comprises firms with robust returns and undervalued earnings growth potential — exactly the type of companies BIMI looks for.

JG Summit Holdings Tearsheet

Today, we’re highlighting one of the largest individual stock holding in the Philam Strategic Growth Fund—JG Summit Holdings, Inc.

As the Uniform Accounting tearsheet for JG Summit (JGS:PHL) highlights, Uniform P/E trades at 18x, below market average valuations, but around its historical averages.

Low P/Es require low, and even negative, EPS growth to sustain them. In the case of JG Summit, their Uniform EPS growth declined by 45% over the past year.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, JG Summit’s sell-side analyst-driven forecast shows a 43% and 23% earnings growth in 2019 and 2020, respectively.

Based on the current stock market valuations, we can back into the required earnings growth rate that would justify PHP 73.9 per share. These are often referred to as market embedded expectations. Even if JG Summit’s Uniform earnings grows by 3% over the next three years, they will meet their current market valuation levels.

What sell-side analysts expect for JG Summit’s earnings growth is above what the current stock market valuation requires.

To conclude, JG Summit’s Uniform earnings growth is above peer averages in 2020. However, the company is trading slightly above average valuations of their peers.

The company has an earning power slightly greater than corporate average returns based on its Uniform ROA calculation. Together, this signals a low cash flow risk to the current dividend level in the future.

About the Philippine Markets Daily

“Friday Uniform Portfolio Analytics”

Investors who don’t engage in the buying or selling of securities for a living oftentimes rely on professionals to manage their own investments within the scope of their investment policies.

These portfolio managers either take on an active role in trading securities or take on a more passive role by putting additional investments in funds.

With so many funds and managers out there, it can get confusing and difficult to decide which one best suits your needs as an investor.

Sometimes, it might look like the manager is buying stocks that don’t seem like high-quality firms. Other times, it might look like the manager is taking a very long-term position on a stock that has not moved for a long time.

Every Friday, we focus on one fund in the Philippines and take a deeper look into their current holdings. Using Uniform Accounting, we identify the high-quality stocks in their portfolio which may not be obvious using the as-reported numbers.

We also identify which holdings may be problematic for the fund’s returns that they would need to reconsider from a UAFRS perspective.

To wrap up the fund analysis, we highlight one of their largest holdings and focus on key metrics to watch out for, accessible in our tearsheets.

Hope you’ve found this week’s focus on the Philam Strategic Growth Fund interesting and insightful.

Stay tuned for next week’s Friday Uniform Portfolio Analytics!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com