Looking through Uniform Accounting lenses shows how this lens company was able to generate 28%+ returns as a “pickaxe seller”

One industry that has a highly competitive environment is the smartphone industry, making it difficult to determine who among its major players would win. Although this company does not sell phones, it is benefitting from the demand in the market by supplying lenses to its players.

However, as-reported metrics do not seem to show how this company’s efforts to advance its products through innovation positively affect its returns. Uniform Accounting shows that the business has a better Uniform return on assets (ROA) than what you might think.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Wednesday Uniform Earnings Tearsheets – Asia-listed Focus

Powered by Valens Research

In one of our previous articles, we discussed the California Gold Rush in 1848 and how investing in “pickaxe sellers” will earn you more money than betting on the miners.

After all, not all miners struck it rich with gold, but all miners needed the equipment to even get started on finding gold. So if you had invested in the pickaxe sellers, you would have made money from the real winners of the gold rush.

Though it isn’t the next gold rush, the smartphone industry is an example of investing in the pickaxe sellers and not the prospectors.

In the past decades, we’ve seen mobile phones evolve from a tool you could use to conveniently call or message someone while on the go to a device that serves as a phone, a gaming console, a camera, a library, a radio, and a television all rolled into one.

Smartphone companies such as Apple, Samsung, Vivo, and Oppo have to continuously innovate and upgrade their offerings to maintain their market share. With consumers changing their phones every two years or so, the smartphone industry has become an incredibly competitive space.

As 85% of mobile phone buyers choose their phones based on the quality of the phone’s camera, today’s company is a “pickaxe seller” that’s benefiting from consumers’ demand for phones that could easily replace SLR cameras.

Taiwanese company Largan Precision, established in 1987, started out as a small plastic lens maker in Taichung City. Since then, the company has grown into one of the world’s major suppliers of optical lenses, offering optical equipment like mobile phone lenses, web cameras, and scanners.

A key factor to Largan’s success is its move of abandoning the mature and saturated glass lens market to develop plastic aspherical lens technology. This action aligned exactly when smartphone makers started demanding higher resolution cameras at lower costs. Since plastic was significantly cheaper than glass, this timing presented great opportunities.

Now, most of the smartphone-owning population carries a Largan product. Largan is the main supplier of camera lenses for iPhones and it also supplies lenses to Apple’s Android competitors, such as Samsung and Huawei.

This means no matter which smartphone manufacturer wins, Largan will always reap the benefits.

The company also maintains its competitive advantage through continuous research and development, as well as patents. Largan lenses are consistently one generation ahead of the rest. The most recent example being the company is now developing 9P lens technology while its competitors like Genius Electronic Optical are still busy developing 8P lenses.

Largan also has a massive portfolio of more than 2,000 patents, creating high technology development barriers in the market and further securing its leading position, with the company currently dominating 35% of the global optical lens market.

For competitors to reduce the technological gap, they will have to go around Largan’s patents to avoid any infringements. As Largan proved by winning its lawsuit against Samsung in 2016 due to a patent dispute, going around Largan’s patents won’t be easy. Samsung even ended up paying royalties to Largan.

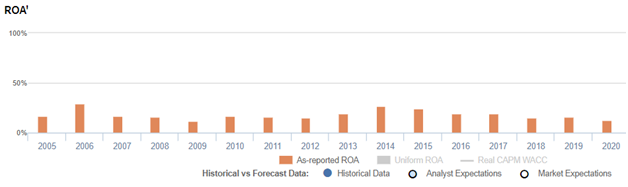

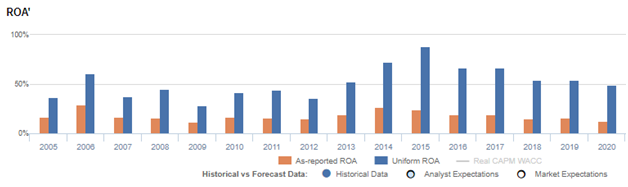

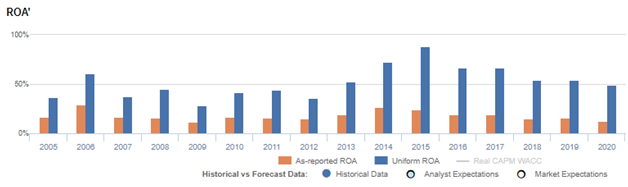

Despite the company’s leading status in the optical lens industry, as-reported metrics don’t seem to fully capture Largan’s stellar performance, ranging only from 12% to 29% in the past sixteen years.

Using Uniform Accounting, a clearer profitability narrative is uncovered. Specifically, the company’s Uniform returns are actually significantly higher than its as-reported metrics in recent years. For example, while as-reported ROA was only at 24% in 2015, Uniform ROA was actually almost 4x that at 89% peak levels.

What as-reported metrics fail to do is to consider the company’s excess cash on the balance sheet. While most companies inherently need some level of cash to operate, the portion of that balance that is earning limited or no return—or excess cash—ends up diluting as-reported ROAs.

When excess cash remains included in the company’s asset base while computing its performance metrics, the company’s profitability and capital efficiency may appear weaker than it actually is.

Removing excess cash allows investors to see through the distortions that come from management carrying much more cash on the balance sheet than what is operationally required.

From 2005 to 2020, Largan has had a significant amount of excess cash sitting idly in its balance sheet, ranging from 16% to 59% of its as-reported total assets.

After excess cash and other necessary adjustments are made, we can see that Largan’s returns are actually a lot stronger than what as-reported metrics show. Without these adjustments, it appears that the company hasn’t been successful in penetrating the mobile lens market with its R&D initiatives, leading to significantly poorer valuations.

Largan’s profitability is much more robust than you think

As-reported metrics are distorting the market’s perception of the firm’s profitability. If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics reveal.

Largan’s Uniform ROA has been higher than its as-reported ROA in the past sixteen years. For example, when Uniform ROA was at 89% in 2015, as-reported ROA was only 24%.

The company’s Uniform ROA for the past sixteen years has ranged from 28% to 89%, while as-reported ROA has ranged only from 12% to 29% in the same timeframe.

Specifically, Uniform ROA improved from 37% in 2005 to 61% in 2006, before subsequently declining to 28% in 2009. It then expanded to a peak of 89% in 2015, before declining to 49% in 2020.

Largan’s Uniform earnings margins are weaker than you think but its robust Uniform asset turns make up for it

Volatility in Uniform ROA has been driven by trends in Uniform asset turns and to a lesser extent, Uniform earnings margins, with peaks and troughs lining up historically with that of Uniform ROA.

Uniform margins expanded from 43% in 2005 to 53% in 2006, which then declined to 28% in 2012. It then recovered back to 47% in 2017 before compressing to 42% levels in 2020.

Meanwhile, Uniform turns steadily rose from 0.9x in 2005 to 2.1x in 2015, before compressing to 1.2x in 2020.

SUMMARY and LARGAN Precision Co.,Ltd Tearsheet

As the Uniform Accounting tearsheet for LARGAN Precision Co.,Ltd (3008:TAI) highlights, the Uniform P/E trades at 13.0x, which is below the global corporate average of 23.7x and its own historical average of 16.2x.

Low P/Es require low EPS growth to sustain them. In the case of Largan, the company has recently shown a 13% Uniform EPS contraction.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Taiwan Financial Supervisory Commission: International Financial Reporting Standards (TIFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Largan’s sell-side analyst-driven forecast is a 1% and 6% EPS growth in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Largan’s TWD 3,140 stock price. These are often referred to as market embedded expectations.

Largan is currently being valued as if Uniform earnings were to shrink 10% annually over the next three years. What sell-side analysts expect for Largan’s earnings growth is above what the current stock market valuation requires in 2021 and 2022.

Furthermore, the company’s earning power is 4x above the long-run corporate average. Also, cash flows and cash on hand are 5x above its total obligations—including debt maturities, and capex maintenance. All in all, this signals a low credit and dividend risk.

To conclude, Largan’s Uniform earnings growth is below its peer averages. However, the company is trading below its average peer valuations.

About the Philippine Market Daily

“Wednesday Uniform Earnings Tearsheets – Asia-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one company listed in Asia that’s relevant to the Philippines and that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on an Asian company interesting and insightful.

Stay tuned for next week’s Asia company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com