Many might think that it’s game over for the GameBoy maker, but its TRUE earning power is 4x stronger than as-reported!

Unable to leave their homes during quarantine, people have turned to personal hobbies for entertainment. Cooking, reading, exercising, watching shows online, and playing video games are some of the top choices.

While hobbies in general provide a much needed distraction from the COVID-19 health crisis, certain hobbies like gaming provide another avenue for human interaction. People have turned to gaming as a way to connect with friends during this time of social distancing.

This company is known for creating GameBoy, and its latest gaming console has been considered to be an essential quarantine item causing stocks of the device to be sold out everywhere.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Wednesday Uniform Earnings Tearsheets – Asia-listed Focus

Powered by Valens Research

The video game industry isn’t just about fun and games. It’s business.

With more than 2.5 billion gamers around the world, it is expected that the industry will continue to grow at an impressive rate.

According to Nielsen’s SuperData, the video game industry made $10 billion in digital revenues this March amid the COVID-19 pandemic. While other industries remain closed because of quarantines globally, gaming is experiencing a boom, with playtime surging by 45% in the United States.

As a result, March 2020 is recorded as the best month so far for the industry.

One of the largest video game companies in the world has greatly contributed to this spike, with its latest game hitting the record for the most console digital sales. This shows that this game maker has benefited greatly from people staying at home during the quarantine period.

This company is also known to have revived the industry after the 1983 video game crash, also known as the Atari shock, with the release of its very first console called Nintendo Entertainment System (NES).

Who would have thought that a company that used to manufacture playing cards would be the saving grace of the video game industry?

What sets Nintendo apart from its competitors like Sony and Microsoft is that it is a first-party developer. This means that Nintendo normally releases games for its own consoles, as opposed to the PlayStation and Xbox that are usually powered by third-party games.

This is in line with Nintendo’s mission of providing its customers with a unique gaming experience by “producing and marketing the best products and support services available.” Nintendo has created well-known industry icons such as Super Mario, Donkey Kong, Zelda, and Pokemon.

In spite of this, many have noticed that this strategy has been a hit and miss for Nintendo. Some critics even go as far as to say that the company has been on a decline since the NES. However, there are others who suggest that this isn’t something to worry about because it is simply how Nintendo operates.

Generally, the company has a cycle of releasing must-have first party games with long gaps in between. This has also been the case for Nintendo’s hardware, which experienced a similar “decline.” For example, the Wii of 2006 was a big hit, but its successor, Wii U, did not appeal to consumers at all.

Today, with the timely release of Animal Crossing: New Horizons, sales of Nintendo have skyrocketed. In March 2020 alone, this game has surpassed the lifetime sales of each previous Animal Crossing game in the series.

Furthermore, since the new Animal Crossing can only be played on the Nintendo Switch, sales of the console has doubled compared to last year. As a result, the Switch is now one of the company’s best-selling devices of all time.

However, there’s no telling if this would’ve been the outcome without the quarantine. Because of the coronavirus, consumer buying patterns have been affected, both in terms of online and offline shopping.

Being isolated at home gives people more time to do things that they wouldn’t normally do on a daily basis. Furthermore, panic buying around the globe has caused demand to surpass supply, especially with tech.

Due to continuous demand, Nintendo plans to increase its production of Switch consoles by 10% this year.

The company, however, has experienced supply chain problems because of the pandemic. In order to remedy this, Nintendo has been contacting suppliers and expanding its network to China and Southeast Asia.

Although these headwinds may have disrupted the company’s short-term operations, Nintendo still has plans lined up for the future.

Nintendo believes that investing and collaborating with partners in the entertainment sector will broaden its reach. In the years to come, Nintendo-themed amusement parks sections in Universal Studios around the globe will be made available to the public.

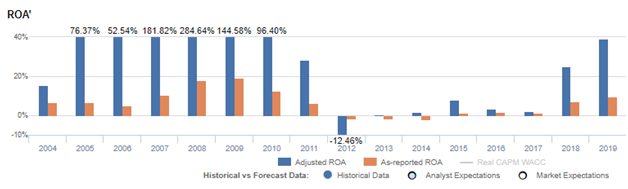

With all of the company’s offerings and long-term initiatives, as-reported returns have been weak at just 9% levels in 2019.

Nintendo’s real economic profitability can be better reflected with Uniform Accounting adjustments, to show its TRUE earning power.

Looking at the company’s 2008 performance where it benefited mostly from the continued success of both Nintendo DS and Wii, Nintendo’s Uniform ROA peaked at 285%. This is massively greater than the as-reported ROA of 18%. This shows that the company’s earning power has been distorted by the inconsistencies in accounting standards.

What as-reported metrics fail to do is to consider excess cash on the balance sheet. While most companies inherently need some level of cash to operate, the portion of that balance that is earning limited or no return—or excess cash—ends up diluting as-reported ROAs.

If excess cash remains included in the company’s asset base in computing its performance metrics, the company’s profitability and capital efficiency may appear weaker than it actually is.

Over the past 16 years, Nintendo has had a significant amount of excess cash sitting idly in its balance sheet, ranging from 53% to 75% of its unadjusted total assets.

After excess cash and other significant adjustments are made, the company reported a 39% Uniform ROA in 2019, which is 4x stronger than their as-reported ROA of 9%.

Nintendo is cheaper than you think it is

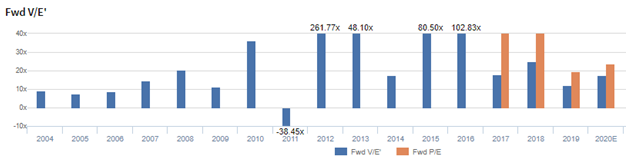

Nintendo Co., Ltd. (7974:JPN) currently trades below corporate averages with a 17.4x Uniform P/E (blue bars), which is also cheaper than the as-reported P/E of 23.7x (orange bars).

At these levels, the market is pricing in expectations for Uniform ROA to rise to 44% in 2024, accompanied by a 1% Uniform asset growth going forward.

However, analysts have more bullish expectations, projecting Uniform ROA to increase to 52% in 2021, accompanied by 3% Uniform asset growth.

Nintendo’s profitability is actually much better than you think it is

As-reported metrics distort the market’s perception of the firm’s profitability.

If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics highlight.

Uniform ROA has actually been higher than as-reported ROA in the past seven years. For example, as-reported ROA was 9% in 2019, significantly lower than its Uniform ROA of 39%. When Uniform ROA peaked at 285% in 2008, as-reported ROA was just at 18%.

Through Uniform Accounting, we can see that the company’s true ROAs have actually been higher. Nintendo’s Uniform ROA for the past seven years ranged from 1% to 39%, while as-reported ROA ranged only from -2% to 9% in the same timeframe.

After rising from 15% in 2004 to a peak of 285% in 2008 due to the success of both Nintendo DS and Wii, Uniform ROA reached rock bottom of -12% in 2012. This is primarily due to the weak sales of Wii U and unprecedented price cuts for Nintendo 3DS.

Afterwards, Uniform ROA recovered to 8% in 2015 before declining to 2% in 2017. After the release of Switch, Uniform ROA increased to 25% in 2018, and expanded further to 39% in 2019.

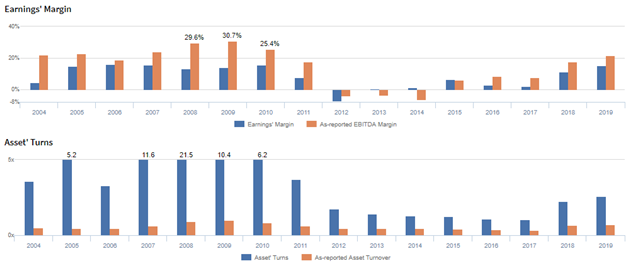

Nintendo’s margins are weaker than you think, but its consistently stronger asset turnover makes up for it

Cyclicality in Uniform ROA has been primarily driven mainly by trends in Uniform asset turns, impacted slightly by Uniform earnings margins, with peaks and troughs lining up historically with that of Uniform ROA.

Uniform earnings margins increased from 4% in 2004 to 16% levels in 2006, before falling back to 13% in 2008. It then recovered to 15% in 2010, but fell deeply to -7% in 2012 before recovering gradually to 15% in 2019.

Meanwhile, Uniform asset turns increased from 3.6x in 2004 to 5.2x in 2005 before falling to 3.3x in 2006. It then recovered and peaked at 21.5x in 2008 then gradually fell to 1.1x in 2017, before expanding again to 2.6x in 2019.

Summary and Nintendo Tearsheet

As the Uniform Accounting tearsheet for Nintendo highlights, they are trading at a 17.4x Uniform P/E, which is below average market valuations but around its historical P/E of 18.1x.

Low P/Es require low EPS growth to sustain them. In the case of Nintendo, the company has recently shown a 58% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Japan’s Modified International Standards (JMIS) earnings and convert them to Uniform earnings forecasts. When we do this, Nintendo’s sell-side analyst-driven forecast is for Uniform earnings to increase by 16% in 2020 and by 25% in 2021.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify JPY 46,900 per share. These are often referred to as market embedded expectations.

In order to meet the current market valuation levels of Nintendo, the company would have to have Uniform earnings grow by 1% each year over the next three years. What sell-side analysts expect for Nintendo’s earnings growth is above what the current stock market valuation requires.

The company’s earning power, based on its Uniform return on assets calculation, is almost 7x the corporate average returns. Furthermore, with cash flows and cash on hand consistently exceeding obligations, Nintendo has low credit and dividend risk.

To conclude, Nintendo’s Uniform earnings growth is above its peer averages in 2019 and it is trading in line with peer average valuations.

About the Philippine Market Daily

“Wednesday Uniform Earnings Tearsheets – Asia-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one company listed in Asia that’s relevant to the Philippines and that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on an Asian company interesting and insightful.

Stay tuned for next week’s Asia company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com