MONDAY MACRO: At 18.5x Uniform P/E, investors are still worried, even as this level is still much lower than at the beginning of the year

China’s CSI 300 Index, which consists of the 300 largest stocks in the Shanghai and Shenzhen stock exchanges, broke its five-year high in early July.

Other countries in Asia such as India, Malaysia, Japan, and South Korea have also seen improvements in their stock market in the same time period. The Philippines, on the other hand, continues to see weakness in the markets.

This indicator shows that even though the local stock market did enjoy some respite in June, we’re not out of the woods yet.

Philippine Markets Daily:

The Monday Macro Report

Powered by Valens Research

This year is proving to be one of the most challenging years for the Philippine stock market in recent history. In our March 16th Monday Macro Report, we talked about two black swan events that occurred just in the first quarter of 2020.

The first black swan event was the Taal Volcano eruption in January 2020, which caused ashfall to spread all over Metro Manila. This posed health issues to the residents of the capital, even causing the suspension of stock market trading on January 13.

The second black swan event was the spread of the novel coronavirus in the Philippines, causing sharp increases in confirmed cases and deaths in Metro Manila. Investors were understandably worried, especially since community quarantines essentially put economic activity to a temporary halt in key cities.

As the Philippines approaches its 5th month in quarantine, investors are still concerned about the state of the economy. The local stock market did see temporary market relief with small rallies in early June. Unfortunately, as daily active COVID-19 cases continue to grow, we have yet to see a flattening of the coronavirus curve.

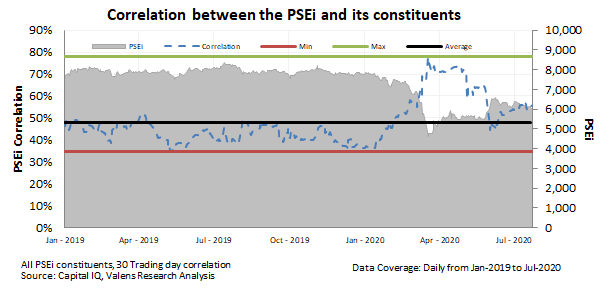

The country’s inability to control the spread of coronavirus cases has caused investor sentiment to stay bearish. We can see this in the correlation index between the PSEi and its constituents.

As we discussed in our April 20th article, a higher correlation indicates higher perceived market risk. That is, investors are actually indifferent to the potential returns of individual stocks and are more concerned about the risks of the general market as a whole.

We saw correlation cross over 50% just as the country was reporting its first cases of COVID-19 cases in late January. We then saw this number spike to a record high of 78% in March 2020 when quarantine orders were enforced and the Philippine stock market crashed.

Investors were concerned about the uncertainty brought by an unprecedented mandatory shutdown of most businesses in Metro Manila. At that point, it did not matter if a stock’s participation in the market sell-off was justified–investors turned to panic selling.

By early June 2020, travel and work restrictions in key economic areas such as Metro Manila were eased. The PSEi was able to recover most of its year-to-date losses, and correlation between the index and its constituents also fell significantly during that time.

Though correlation is at a less concerning 56% mark than at the start of the second quarter, it is still above its historical averages. Market sentiment is also expected to turn negative in the next few months as the country continues to deal with the COVID-19 pandemic.

For as long as the COVID-19 cases are still growing at an alarming rate, quarantine measures will likely continue to be in place in one form or another.

The PSEi performance will continue to be dragged down as it is heavily exposed to sectors that require looser travel restrictions to generate sales. This includes sectors such as real estate (e.g. residential and commercial space) and consumer discretionary-related services such as tourism, travel, and restaurants.

Banks will also be surrounded with negative sentiment given the economy’s expected lower earnings power under the current business environment, that will likely lead to lower debt repayment capability of its corporate borrowers.

With persisting limited economic restrictions, it is not surprising that both foreign and local investors have continued to sell off their shares as health improvements seem unlikely. Even the low-risk, blue-chip companies are feeling the effects of the weaker stock market.

Investors will likely stay cautious and stay away from the Philippine stock market. However, we continue to reiterate that this recessionary environment will not be for an extended period. The largest Philippine companies still have safe credit profiles, allowing them the flexibility to borrow more capital if necessary.

As mentioned in our June 15 report, Uniform Accounting sees the economy to retract by 2% this year and recover in the following year to pre-COVID-19 ROA levels.

A recession that is not caused by a credit-driven event will have a swift recovery as credit-driven recessions historically have a lot more inherent problems that need to be resolved before economic growth kicks back in.

About the Philippine Markets Daily

“The Monday Macro Report”

When just about anyone can post just about anything online, it gets increasingly difficult for an individual investor to sift through the plethora of information available.

Investors need a tool that will help them cut through any biased or misleading information and dive straight into reliable and useful data.

Every Monday, we publish an interesting chart on the Philippine economy and stock market. We highlight data that investors would normally look at, but through the lens of Uniform Accounting, a powerful tool that gets investors closer to understanding the economic reality of firms.

Understanding what kind of market we are in, what leading indicators we should be looking at, and what market expectations are, will make investing a less monumental task than finding a needle in a haystack.

Hope you’ve found this week’s macro chart interesting and insightful.

Stay tuned for next week’s Monday Macro report!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com