MONDAY MACRO: At 2.4%, this metric hasn’t changed much this year even as PH hit a recession, Uniform Accounting shows valuations have become cheaper

At a glance, this metric can provide multiple insights on an economy’s health.

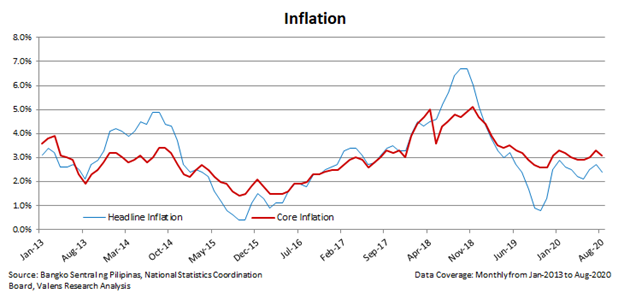

While economic activity in the Philippines has contracted in the first half of 2020, this metric has remained sideways.

Even with continued assistance from the Bangko Sentral ng Pilipinas (BSP) through its extensive use of its expansionary monetary policy tools, investors are concerned about Philippine economic recovery.

Uniform Accounting shows how valuations are affected by this metric and how changes in this metric further support how the Philippines’ technical recession is not a long-term concern.

Philippine Markets Daily:

The Monday Macro Report

Powered by Valens Research

Since the start of 2020, the BSP has slashed interest rates four times, and the rates are now 175 basis points lower than last year.

If you recall in one of our Monday Macro reports, the BSP increased interest rates five times in 2018, ending the year 150bps higher than interest rates in 2017. This was in response to the effects of the Tax Reform for Acceleration and Inclusion (TRAIN) Act on inflation in 2018.

Once inflation had stabilized, the BSP decided to cut rates in 2019, ending the year at 75bps lower than in 2018. Analysts were expecting this rate reduction to continue in 2020 by about 50bps.

Of course, no one could have predicted that a pandemic would occur. Instead of just a 50bps rate reduction, we’re now seeing 175bps lower rates compared to 2019.

Lower interest rates are good in an environment where economic activities need a boost. This scenario would mean lower costs to borrow, which should improve capital availability in businesses.

Since the Philippines has just experienced two consecutive quarters of negative GDP growth, offering low interest rates to businesses to aid in their expansion should help spur economic growth.

Moreover, in line with the BSP’s objective to spur growth, the BSP also lowered the reserve requirement ratio imposed to banks.

These two policy actions have effectively resulted in an increase in domestic liquidity by 14.5% year-on-year as of July. As mentioned in our July 20th Monday Macro report, sustainable domestic liquidity around the Philippine economy should entice banks to further lend to their clients.

However, despite the increased liquidity in the domestic market, lending activities have been slow. This is due to an overall decrease in loan demand, as well as banks tightening credit standards.

According to the Q2 2020 Senior Bank Loan Officers’ Survey (SLOS), banks were taking a more conservative stance because of uncertain economic outlook, expected deterioration in borrowers’ profiles, worsening of industry- or firm-specific outlook, and banks’ lower tolerance for risk.

As we have mentioned in our August 24th Monday Macro report, banks’ credit standards will likely ease in the succeeding quarters as economic activity picks up, and as earnings generation becomes more stable. This easement should further assist in the recovery of aggregate spending levels as businesses start to expand again and get more people employed.

Philippine inflation rate eased to 2.4% in August after rising for two consecutive months in June (2.5%) and July (2.7%). Similarly, the core inflation rate declined to 3.1% after hitting 3.3% in July.

The low interest rate environment and excessive liquidity surrounding the Philippine economy should have produced an inflationary outcome. Instead, we’re seeing inflation rates remain at the low end of BSP’s inflation target range since the start of the year.

Though businesses have slowly started reopening as Metro Manila shifted to the general community quarantine (GCQ), consumer spending growth remains muted. In the absence of increased demand and as supply conditions remain unchanged, inflation is likely to remain at its current levels.

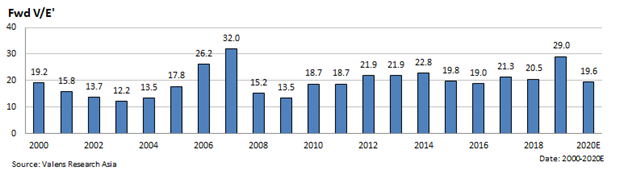

Under Uniform Accounting, current Philippine market valuations are at 19.6x Uniform P/E, falling from a 12-year high Uniform P/E of 29.0x. Prior to the global pandemic, the Philippine market was trading at high valuations relative to its earnings. Its growth potential, with GDP growing by over 5% over the last five years, justified it being fairly valued at best.

As the market corrected in the past months due to the pandemic, we’re seeing valuation levels come down from last year’s high. Since factors such as the low inflationary environment, young demographics, and high government spending continue to exist, the country’s growth potential is still there, making current valuations inexpensive.

In the end, investors should be patient as the Philippine economy should be able to recover soon from the recession as the public health crisis subsides. Despite the economic contraction, the technical recession was not credit-driven as we have identified in our August 10th article.

About the Philippine Market Daily

“The Monday Macro Report”

When just about anyone can post just about anything online, it gets increasingly difficult for an individual investor to sift through the plethora of information available.

Investors need a tool that will help them cut through any biased or misleading information and dive straight into reliable and useful data.

Every Monday, we publish an interesting chart on the Philippine economy and stock market. We highlight data that investors would normally look at, but through the lens of Uniform Accounting, a powerful tool that gets investors closer to understanding the economic reality of firms.

Understanding what kind of market we are in, what leading indicators we should be looking at, and what market expectations are, will make investing a less monumental task than finding a needle in a haystack.

Hope you’ve found this week’s macro chart interesting and insightful.

Stay tuned for next week’s Monday Macro report!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com