MONDAY MACRO: Low to no risk of recession warranted as the Philippines presents a healthy UAFRS-based credit profile

The 1997 Asian Financial Crisis came as a surprise to most countries. It started out as a currency crisis among a few Asian countries, including Thailand, Indonesia, South Korea, and even the Philippines.

But look deeper, and you’ll find that these countries had high leverage ratios in their largest companies.

While the Philippines did take a hit, with GDP growth dipping to negative levels in Q2 and Q4 of 1998, the country did not enter a recession. This is thanks to the continued support that OFW remittances have provided the Philippine economy.

Philippine Markets Daily:

The Monday Macro Report

Powered by Valens Research

The Philippines faced a recession from 1984 to 1986 during the Marcos administration, brought about by an increasing budget deficit, the difficulty of securing new capital, and the collapse of confidence and credit ratings from international financial institutions.

In 1991, the country had another recession after suffering from a power crisis that caused major nationwide outages.

However, the Philippines did not experience a recession during any of the recent global economic crises such as the Asian Financial Crisis in 1997-1998 and the Global Financial Crisis in 2008.

But growing concerns surrounding the economic stability of the Philippines’ largest trading partners have made investors wonder if the Philippine economy will take a bigger hit this time. The US accounts for 15% of Philippine exports, while China contributes to 13% of total exports.

The recent trade war between the United States and China has made a number of investors pessimistic, although recent developments on this front have eased concerns.

Then there’s the 2019 Novel Coronavirus outbreak.

WHO declared the coronavirus outbreak a global public-health emergency last January 30, 2020. With the Chinese economy affected with the virus, some may argue of its lasting impact with the Philippines and its GDP growth for 2020.

These trade issues could disrupt aggregate Philippine earnings growth in the short term and create short-term volatility. However, a lack of growth in profitability will not start a recession on its own.

Recessions begin when there’s an underlying credit crisis.

That normally happens when creditors have to refinance debts at the very moment when they cannot.

It happens when corporations take on too much leverage and cannot service their obligations.

In all the major global recessions that occurred, it is very difficult to find one that didn’t start with a debt crisis.

Our previous Monday Macro Report for the Investors Essentials Daily can provide more instances surrounding bear markets that followed from debt crises.

Negative credit events and credit destruction are essential for a recession to occur. This is something that Philippine companies have the advantage of.

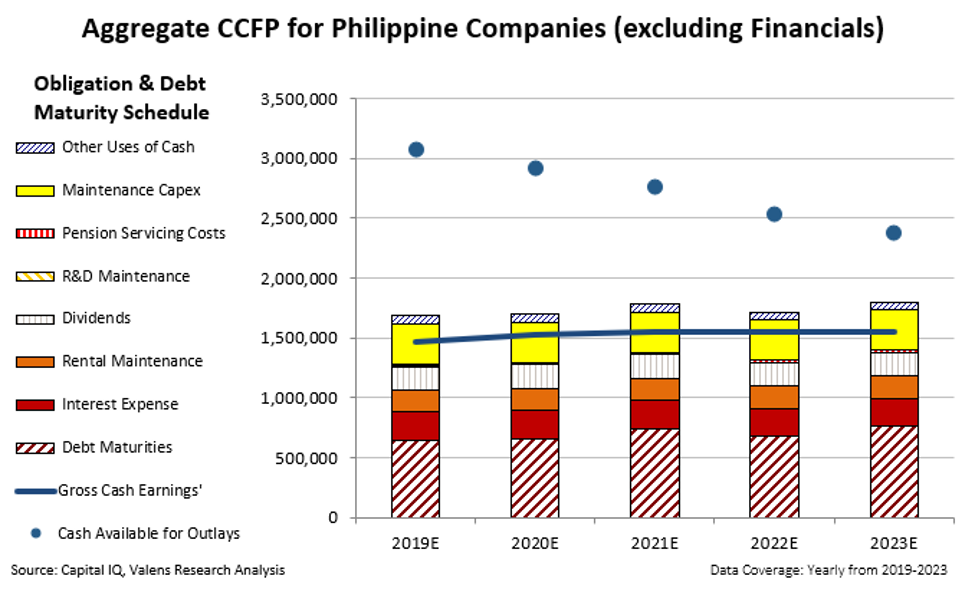

The chart above, the Credit Cash Flow Prime chart, or CCFP, provides a snapshot of the credit health of Philippine companies on aggregate.

Using Uniform Accounting numbers, the bars represent the financial obligations that Philippine companies need to service.

The most flexible obligations would be at the top (blue stripes). These ones could be delayed until further notice since they are of least priority. The least flexible at the bottom (red stripes) are of utmost priority.

This “stack” bar includes items like debt maturities, dividends, required reinvestment levels into the business, and rent.

The blue line represents the aggregation of corporate cash flows available for paying their financial obligations. The blue circles above represent the liquidity available to the company which includes excess cash on hand.

Even when debt and capital requirements exceed the firm’s cash flows, as long as they still have enough cash on hand, there should be nothing to worry about for the year.

That is exactly what the Philippines’ credit profile looks like in the next five years.

With stable debt maturities over the next several years, companies in the Philippines have no material debt headwall that would cause refinancing concerns. There is still a sizable amount of cash available for outlays that should cover their obligations and debt maturities even when their Uniform gross earnings cannot.

Going back to the Philippines’ trading partners, the US aggregate credit profile shows that cash on hand is more than enough to handle their cash requirements over the next three years at the very least.

China also has sufficient earnings that would cover all of their pending commitments in the foreseeable future.

It is also important to note that the Philippines’ robust remittances have helped insulate the country from the impact of past crises such as the Global Financial Crisis in 2008.

With no catalyst for credit destruction for the Philippine Composite Index and proper fiscal and monetary stimulus, a bullish 7% GDP growth set by the government for 2020 is warranted.

About the Philippine Markets Daily

“The Monday Macro Report”

When just about anyone can post just about anything online, it gets increasingly difficult for an individual investor to sift through the plethora of information available.

Investors need a tool that will help them cut through any biased or misleading information and dive straight into reliable and useful data.

Every Monday, we publish an interesting chart on the Philippine economy and stock market. We highlight data that investors would normally look at, but through the lens of Uniform Accounting, a powerful tool that gets investors closer to understanding the economic reality of firms.

Understanding what kind of market we are in, what leading indicators we should be looking at, and what market expectations are, will make investing a less monumental task than finding a needle in a haystack.

Hope you’ve found this week’s macro chart interesting and insightful.

Stay tuned for next week’s Monday Macro report!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com