MONDAY MACRO: Rising levels of this ratio shouldn’t be a concern, especially as Uniform Accounting reveals this economic recession is not debt-driven

Micro, Small, and Medium Enterprises (MSMEs) play an important role in the development of the economy. Many successful corporations in the Philippines started small before becoming the industry juggernauts they are today, such as Jollibee and SM Investments.

However, because of their size, MSMEs are one of the hardest hit businesses in the pandemic—their pockets are not deep enough to hunker down for prolonged periods of time. It’s one of the reasons why expectations for this banking ratio has analysts concerned about its further deterioration.

Although a higher value for this metric is concerning, Uniform Accounting highlights that this ratio might be too pessimistic. There is still enough financial safety in the banking system and the aggregate credit profile of smaller listed firms remains safe.

It is worth monitoring what happens to this ratio once the country comes out of this health and economic crisis.

Philippine Markets Daily:

The Monday Macro Report

Powered by Valens Research

Our September 7th Monday Macro report mentioned how businesses have adapted to the current environment by transitioning their operations to online platforms. However, the unemployment rate still remains at high levels, as many businesses have closed because of the lack of revenue opportunities.

One of the best ways to tackle a high unemployment rate is for the government to focus on helping small businesses grow and thrive. Approximately 70% of employment in the Philippines comes from the MSMEs. If more of these MSMEs went bankrupt or closed down, it would take a much longer time for unemployment to improve.

With limited revenue sources because of the quarantine period, most of these small businesses would need external funding to pay for their operating expenses. Unfortunately, finding a bank to give them favorable terms for a loan is a feat in and of itself.

Unlike much larger businesses, MSMEs in developing economies have always struggled to access credit services, according to the World Bank. There isn’t a lot of collateral these small businesses could offer banks in exchange for loans.

This is where the government comes in.

The Bangko Sentral ng Pilipinas (BSP) approved a package in April 2020 to count bank loans for MSMEs as part of the banks’ reserve requirements. The package is one way to incentivize banks to extend loans to these small businesses without worrying about the banks’ compliance with BSP regulations.

As a recap, reserve requirements are the total amount of compliance funds that are monitored by the BSP. These have been used often in monetary policy to control the money supply in the economy.

Meanwhile, the recent passage of the Bayanihan 2 allows the infusion of capital of government financial institutions (GFIs) into these small businesses. Particularly, the Land Bank of the Philippines (LandBank) and Development Bank of the Philippines (DBP), are allowed to provide low-interest loans for workers and businesses, especially for MSMEs.

Although additional sources of capital will go a long way in helping MSMEs recover, weak consumer demand will continue to pose a threat to how long these small businesses can hold out during this pandemic.

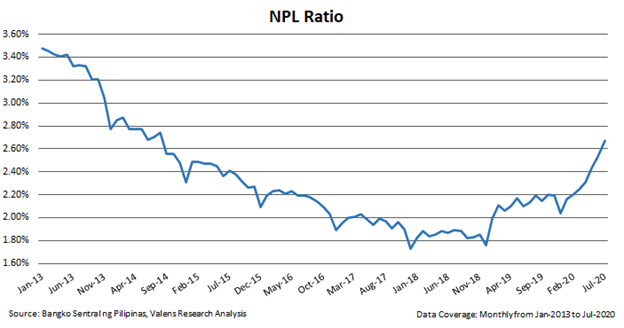

Experts and analysts alike estimate that non-performing loans (NPL) will continue to increase throughout 2021, and MSME borrowings are likely to drive them. At the same time, the BSP expects NPLs to even double by the end of the year to 4.6%.

The NPL ratio is the portion of unpaid loans for more than 30 days after the due date, as a percentage of the total loan portfolio. A low NPL ratio shows strength in the financial system and state of the economy, while a high NPL ratio implies that banks have taken on low-quality loans.

Since March 2020, the NPL ratio of the Philippine banking system has expanded from 2.2% to 2.7% in July. This is the highest it has been since 2014 when banks’ real estate exposure peaked, and the ratio is even expected to nearly double by December due to the pandemic.

Even with the BSP’s expected NPL ratio of 4.6% by December 2020, this is no reason to be concerned about the Philippine banking sector.

The Philippine banking system saw NPL ratios skyrocket to 12.1% in January 1998 following the 1997 Asian Financial Crisis. Since then, the country has managed to keep its NPL ratios low thanks to key policies from the government. Even during the previous global financial crisis, Philippine banks just showed 5.0% in March 2008.

This shows how much our banking system has improved over the years. The banking system is more likely to maintain its strength through this pandemic, especially since this latest recession is not credit-driven.

Furthermore, with the passage of the Bayanihan 2 law, key bills to help the economy are expected to be prioritized, such as the Financial Institutions Strategic Transfer (FIST) bill, and Government Financial Institutions Unified Initiatives to Distressed Enterprises for Economic Recovery (GUIDE) bill.

The FIST bill aims to reduce the threat of NPLs to the banking system by advocating strategic transfer corporations that would receive distressed loans and resolve them. This would enable banks to have more space to underwrite new credit that will sustain the economy.

On the other hand, the GUIDE bill aims to strictly support strategically important companies on the verge of insolvency by infusing capital from GFI-supported companies.

Fortunately, as we discussed in our August 10th Monday Macro report, the aggregate credit profile of publicly-listed companies in the PSE All Shares Index (excluding Financials and top 30 companies) shows that it isn’t just the large Philippine companies that will survive the crisis. Even smaller companies have sufficient cash available to pay high priority obligations such as debt and interest payments.

That said, ample corporate liquidity, a robust financial system, and government support through bills should be able to recover the economy at a faster rate compared to previous recessions since this was not driven by debt.

About the Philippine Market Daily

“The Monday Macro Report”

When just about anyone can post just about anything online, it gets increasingly difficult for an individual investor to sift through the plethora of information available.

Investors need a tool that will help them cut through any biased or misleading information and dive straight into reliable and useful data.

Every Monday, we publish an interesting chart on the Philippine economy and stock market. We highlight data that investors would normally look at, but through the lens of Uniform Accounting, a powerful tool that gets investors closer to understanding the economic reality of firms.

Understanding what kind of market we are in, what leading indicators we should be looking at, and what market expectations are, will make investing a less monumental task than finding a needle in a haystack.

Hope you’ve found this week’s macro chart interesting and insightful.

Stay tuned for next week’s Monday Macro report!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com