MONDAY MACRO: This indicator still hasn’t behaved the way analysts thought it would despite a 5-year high of 11% growth in national debt.

In the past few months, the Philippine government has borrowed more than $5 billion from various international lenders to fund its efforts against the novel coronavirus disease.

Given the significantly larger Philippine national debt, and the increasingly uncertain economic environment because of the growing number of coronavirus cases, one would expect this economic indicator to rise.

However, it hasn’t moved the way most analysts would expect it to. Uniform Accounting provides some insights on why this downward shift occurred.

Philippine Markets Daily:

The Monday Macro Report

Powered by Valens Research

One of the Philippine government’s responses to the coronavirus pandemic was to implement community quarantines in major and affected cities in the Philippines. It also borrowed over $5 billion dollars from various lenders such as the Asian Development Bank, the World Bank, and the Asian Infrastructure Investment Bank.

These additional funds were deemed necessary to support the medical front-liners through the purchase of necessary personal protective equipment and test kits. The funds were also needed to offer financial assistance to displaced workers and small businesses affected by the temporary shutdowns.

By April 2020, the Philippine’s national debt reached PHP 8.6 trillion, an 11% increase from 2019, and the highest growth rate it has seen in the last five years.

Even with this much larger budget, the Philippines has yet to flatten the coronavirus curve.

Despite the economy slowly reopening after over 100 days, investors are still concerned. Establishments are still unable to operate at 100% capacity and many small businesses have already filed for bankruptcy.

Furthermore, the unemployment rate is at all-time highs, reaching 18% in April 2020. This means consumers as a whole have lower disposable income, which means lower consumer spending. This impacts businesses’ ability to generate income.

With lower potential tax collections from both businesses and employees as a result of the quarantine, and the need for the government to continuously spend to support the economy, the Philippine budget deficit is expected to further widen to PHP 202.1 billion.

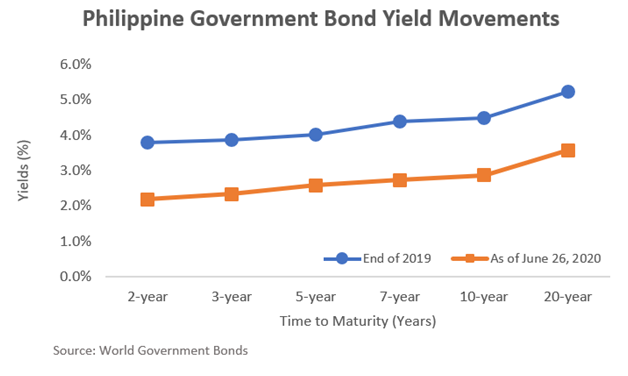

Normally, when the government wants to attract more investments in the country to compensate for any economic difficulties it is experiencing (e.g. mounting national debt), it raises interest rates on government-issued bonds.

When the government increases its interest rates, companies also end up increasing the rates they offer on their own bonds to remain attractive to investors. When the government increases its interest rates, interest charged on debt that companies and individuals pay also increases.

It becomes a whole cycle of increasing risk in the short term, which usually results in an inversion of the yield curve. In the near term, investors generally demand much higher interest rates than in the long term, to compensate for the additional risks they are taking on now.

We normally see the inversion of yield curves before a recession, but we haven’t seen yield curve inversions. We also haven’t seen an increase in interest rates, which is another behavior we can expect in times of economic difficulties as discussed above.

What we are seeing instead is a downward adjustment for interest rates.

As of June 26, 2020, the 2-year local government bond yield was at 2.183%. 5-year bonds reported a 2.579% yield, while 10-year bond yield was at 2.874%.

This downward shift of the curve can be attributed to the increase in demand for safe-haven investments such as government bonds, as well as the low-inflation environment.

In addition, as we have mentioned in our June 15th Monday Macro report, Aggregate Uniform ROA is still expected to be above global cost-of-capital levels this year. Uniform Accounting credit analysis from our June 1st Monday Macro report also shows sufficient cash levels to pay off debt obligations in the same time period.

Moreover, if we look at total government debt relative to GDP, the debt to GDP ratio in 2019 was actually just 40%. Department of Finance Spokesperson Tony Lambino provided reassurance that the ratio will be kept within the 50% range, which is still far from its historical high of 118% in 2003 and below the emerging market average.

That said, government bond yields are expected to stay low given the robust profitability and healthy credit profile of large businesses. The current yield curve shape indicates that investors are not seeing imminent concerns on the country’s recovery prowess.

About the Philippine Market Daily

“The Monday Macro Report”

When just about anyone can post just about anything online, it gets increasingly difficult for an individual investor to sift through the plethora of information available.

Investors need a tool that will help them cut through any biased or misleading information and dive straight into reliable and useful data.

Every Monday, we publish an interesting chart on the Philippine economy and stock market. We highlight data that investors would normally look at, but through the lens of Uniform Accounting, a powerful tool that gets investors closer to understanding the economic reality of firms.

Understanding what kind of market we are in, what leading indicators we should be looking at, and what market expectations are, will make investing a less monumental task than finding a needle in a haystack.

Hope you’ve found this week’s macro chart interesting and insightful.

Stay tuned for next week’s Monday Macro report!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com