MONDAY MACRO: This key economic health indicator fell to historical lows, but investors shouldn’t be concerned about that this time

Filipinos immediately felt the impact of the community quarantines since mid-March 2020, with people losing their jobs, public transportation being suspended, and smaller businesses having to close.

After two consecutive quarters of economic contraction, it became official—the Philippines was now in its first recession in nearly thirty years.

This metric is key in measuring economic health, and its current new lows have analysts worried. While that might paint a concerning picture, this data needs to be analyzed together with other metrics for context to the current situation. After all, this particular recession is not like any other country has ever experienced.

Philippine Markets Daily:

The Monday Macro Report

Powered by Valens Research

Last week, we mentioned that the Philippines entered a technical recession, which occurs when an economy experiences two consecutive quarters of GDP contraction.

The last time the country experienced a recession was in 1991, during the Cory Aquino administration that was plagued with energy crises and political turmoil. The recession before that was during the Marcos administration when the economy contracted for 10 straight quarters from Q4 1983 to Q1 1986 due to political instability.

While neighboring countries experienced negative economic growth during the 1997 Asian financial crisis, and again during the 2008 global financial crisis, the Philippines managed to record positive GDP growth.

Therefore, historically, we see that recessions in the Philippines have been caused by internal problems and not by external factors. It is also important to note once more that this recession is not credit-driven, but rather because of government-mandated quarantines.

The uniqueness of this situation further stresses the importance of looking at metrics with other data for context, not just in isolation.

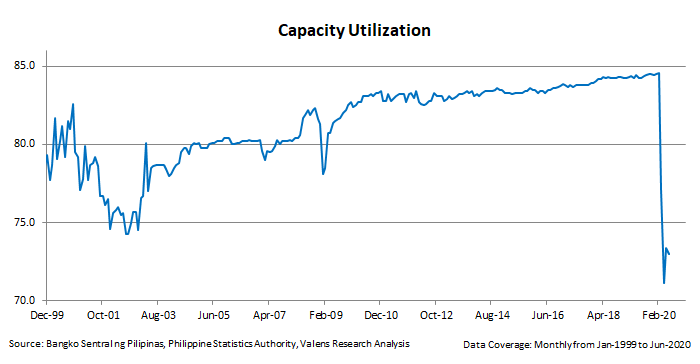

One key metric we often use to measure economic health is capacity utilization, which determines the potential output, in terms of capacity, that is actually realized without capex spending.

Companies operating at 85% capacity utilization are normally considered as operating at an optimal rate. A value above 85% means corporations need significant capex spending to grow, which could cause inflation.

Large dips in capacity utilization are a lagging indicator of a recession. They signal capex will likely be subdued going forward, and is also a signal of lower inflation going forward, due to slack in the economy.

As expected, Philippine capacity utilization fell to historical lows in the past months because of restricted economic activity.

When we discussed this metric in February, capacity utilization had been stable at 84% to 85% levels in the past four to five years. That meant significant investments were needed to push corporations to grow.

In April 2020, the value fell to 71%, showing how much actual output declined in just two months. Although there was a slight increase to 73% by June 2020, it was still at historical lows.

Capacity utilization does not just tell us whether or not economies are operating at optimal levels, it is also a great indicator of economic growth.

When utilization improves, companies are more efficient, and potential growth opportunities are realized from increased production. This results in more jobs for the companies and it improves the economy as well.

On the other hand, a shrinkage in utilization means limited economic growth due to a slowdown in capex investment, resulting in higher unemployment rates.

As we’ve mentioned many times in the past, this economic contraction is different from previous recessions. This decline in capacity utilization is also different from previous declines. Physical distancing and quarantine measures have pressured this metric, not structural problems in the wider economy.

This means that as the quarantine restrictions are eased, capacity utilization could rebound far faster than it normally does, assuming there aren’t other follow-on issues.

To gain more insight into growth, let’s take a look at the Net/Gross PP&E ratio, another great indicator of capex spending.

We mentioned in our February 10th Monday Macro how the Net/Gross PP&E serves as a guide to the potential GDP growth rate. A higher ratio means that assets are newer.

Unlike the capacity utilization, the Net/Gross PP&E currently is at a historical high of 59%. This indicates that companies spent on capex in Q1 2020 to widen their growth prospects, and invested more in expanding production capacities.

We still need to wait for what the Q2 2020 numbers for this ratio would look like since that was when local economic restrictions took place. If the ratio is lower, we could expect a faster rebound in capacity utilization once the quarantine is lifted.

About the Philippine Markets Daily

“The Monday Macro Report”

When just about anyone can post just about anything online, it gets increasingly difficult for an individual investor to sift through the plethora of information available.

Investors need a tool that will help them cut through any biased or misleading information and dive straight into reliable and useful data.

Every Monday, we publish an interesting chart on the Philippine economy and stock market. We highlight data that investors would normally look at, but through the lens of Uniform Accounting, a powerful tool that gets investors closer to understanding the economic reality of firms.

Understanding what kind of market we are in, what leading indicators we should be looking at, and what market expectations are, will make investing a less monumental task than finding a needle in a haystack.

Hope you’ve found this week’s macro chart interesting and insightful.

Stay tuned for next week’s Monday Macro report!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com