MONDAY MACRO: Unlike other macro indicators, this one is slow in its recovery, but that’s not necessarily a problem

A lot of macroeconomic statistics have recently shown signs of a recovering economy. GDP growth and the unemployment rate have been on a rebounding trend, while inflation is forecasted to be cooling off.

However, one indicator of manufacturing activity has been sluggish in its recovery. It may spell trouble for the Philippines, but when laying out the context, it’s not as troubling as it initially seems.

Philippine Markets Daily:

The Monday Macro Report

Powered by Valens Research

After more than a year into the pandemic, various economic indicators are showing signs of strength in the Philippines.

The country’s unemployment rate has finally improved from 17.6% in April 2020 to 7.7% in May 2021. Although this is still above the 4%-5% average, it is a welcome result.

Though the latest quarterly GDP numbers displayed a contraction of 4.2% year-over-year, which means the Philippine economy is still in a recession, the GDP growth rate has been improving since posting a 17.0% decline in Q2 2020.

Meanwhile, inflation has been hovering above the Bangko Sentral ng Pilipinas’ (BSP) 2%-4% guidance range for a few months now. Thanks to lower meat prices and transportation costs, forecasts now project inflation to decelerate within the coming months.

These widely used macroeconomic statistics highlight the slow-but-sure recovery of the Philippine economy, painting a more optimistic picture that the worst may be over.

Investors even share this sentiment as evidenced by the Philippine Stock Exchange Index (PSEi) recovering more than half of its pandemic losses.

With the vaccine rollout, many are now expecting that a bounce back to pre-pandemic levels and beyond is near.

While we do think economic activities will increase as businesses and tourism open up once more, one metric tells us economic expansion won’t primarily come from business expansion just yet.

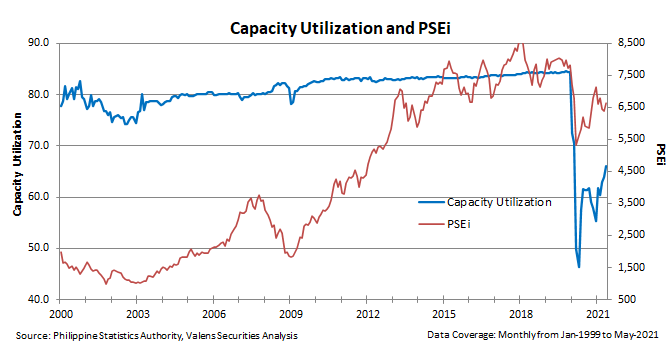

Capacity utilization is essentially a measure of slack in the economy. It compares a country’s current production relative to how much it can potentially produce without causing inflationary pressures.

Large dips in capacity utilization are a lagging indicator of a recession. They signal capex will likely be subdued going forward, and are also a signal of lower inflation going forward, due to slack in the economy.

Historically, the Philippines’ capacity utilization rate averaged 81% from 2001-2019, inching towards 85% levels during the later years. However, due to the coronavirus lockdown and the drastic reduction in consumer demand, it massively dropped to a low of 46% in April 2020.

Though capacity utilization recovered to 66% in May 2021, a significant upswing, this is still a far cry from historical averages.

This means even after the economy starts to recover, there is so much slack in the system that corporations do not need to rush to invest in capex for growth.

If businesses do invest in more assets, that would only keep capacity utilization rates low. There would be too many assets trying to generate fractional incremental revenue.

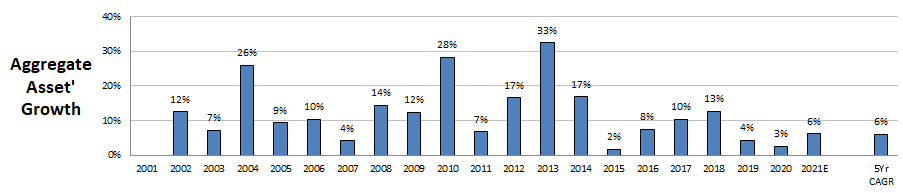

Given the Philippines’ economic state in 2020, one would think that businesses would prioritize minimizing costs over investing in more assets.

Looking at the aggregate real operating assets of the PSE-listed companies, we’re seeing the opposite. Uniform assets grew by 3%, indicating that there is more potential capacity now.

While many businesses may have shrunk, as a whole, corporate Philippines grew in 2020.

With how much unused capacity there is right now in the economy, one might think potential for growth is also limited and that perhaps, investors are too optimistic about the market’s recovery.

However, we have to also consider how differently capacity utilization was pressured because of the pandemic.

The decline was not due to slower capex spending or problems in the economy but because of quarantines and physical distancing measures. Once these restrictions are lifted, capacity utilization could rebound aggressively, faster than it normally does, assuming there aren’t other follow-on issues.

Furthermore, if capacity utilization does see a resurgence, we’ll see stronger capex recovery and better earnings growth.

Investors may also be expecting this as the PSEi is nearer to its pre-pandemic levels than its lowest point during the market sell-off in March 2020.

So though ordinarily, low capacity utilization levels mean a prolonged recession, because of the special situation of a pandemic-triggered recession we are in, that isn’t the case this time. Once an economic recovery is underway, we should see capacity utilization bounce back, which means at low levels, it should not be as worrisome to the stock market and the economy as people might think.

About the Philippine Markets Daily

“The Monday Macro Report”

When just about anyone can post just about anything online, it gets increasingly difficult for an individual investor to sift through the plethora of information available.

Investors need a tool that will help them cut through any biased or misleading information and dive straight into reliable and useful data.

Every Monday, we publish an interesting chart on the Philippine economy and stock market. We highlight data that investors would normally look at, but through the lens of Uniform Accounting, a powerful tool that gets investors closer to understanding the economic reality of firms.

Understanding what kind of market we are in, what leading indicators we should be looking at, and what market expectations are, will make investing a less monumental task than finding a needle in a haystack.

Hope you’ve found this week’s macro chart interesting and insightful.

Stay tuned for next week’s Monday Macro report!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com