Switching to a fabless model jump-started this company’s position in the semiconductor industry, building Uniform ROAs of 10%+

Contrary to industry norms, this company shifted to the fabless business model and went on to become one of the leading semiconductor companies in the world.

With a renewed focus on product innovation and development that came with the shift, as well as a few complementary strategic acquisitions, the company earned a position at the top of the premium audio technology market, and has continued to do so.

However, as-reported data suggests that an innovation-driven strategy isn’t generating robust returns for the company. In reality, Uniform Accounting shows that the company has actually been achieving returns north of 10%.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

During the 1970s, semiconductor manufacturers utilized a vertically integrated business model, a style purely focused on designing, testing, and building the companies’ own products.

However, with the rising number of chip manufacturers, an oversupply of chips became a prevalent issue in the industry. This led to the formation of the fabless business model, which is short for fabricationless.

Similar to the first business model, this framework enabled semiconductor companies to design and market their products. The difference is, it doesn’t manufacture the products directly; the fabrication process is outsourced to another manufacturer in countries with lower labor costs.

This gave companies the advantage of focusing their investments on research and development, particularly in product innovation and in the strengthening of their distribution processes.

When Cirrus Logic’s (CRUS) co-founder Michael Hackworth became CEO in 1985, he adopted the fabless business model for the company.

During that time, becoming a fabless semiconductor company was a bold step because all of the firms in the industry were fixated on having their own manufacturing capabilities. However, CEO Hackworth believed that this move was necessary in order for Cirrus Logic to become one of the leading semiconductor companies in the world.

During the early years of its operations utilizing the fabless business model, the company only wanted to develop integrated circuits (IC) for the personal computers (PC) components market.

However, in 1991, it acquired Crystal Semiconductor, a company that provided mixed-converter ICs for multimedia devices. This proved to be a key component of Cirrus Logic’s success as one of the leading suppliers of low-power, high-precision mixed-signal processing solutions for audio applications.

Basically, the technology from Crystal enabled the company to innovate products that significantly improved how digital devices process audio signals, therefore enhancing the user’s listening experience.

These mixed-converter ICs were used for electronics such as media players, gaming devices, and eventually, for smartphones and tablets, particularly as a main component for Apple and Android devices.

Cirrus Logic then continued to make strategic acquisitions to strengthen operations and broaden its product portfolio, with its Wolfson Microelectronics acquisition in 2014.

With both companies being huge players in the portable audio applications space, the acquisition turned Cirrus Logic into one of the strongest semiconductor powerhouses in a growing market.

Wolfson’s main customer, Samsung, provided Cirrus Logic the opportunity to diversify its customer base and its revenue source, of which about 80% came from Apple. Furthermore, the company then got access to the target’s noise-cancellation technology, a feature that major audio equipment manufacturers are now highlighting.

Currently, with more than 3,450 issued and pending patents on technology across the globe, Cirrus Logic continues to build and improve its diverse portfolio through the optimization of its existing products and by enhancing its innovation process.

In 2019, due to the company’s strong drive for consistent innovation, it was able to become one of the strategic partners of Silicon Catalyst—a company that is currently the world’s only incubator that specializes in developing solutions for silicon technology.

Overall, Cirrus Logic’s consistent focus on innovation and product development has led to strong relationships with two of the largest smartphone manufacturers, as well as superior positioning in the premium audio market for a vast range of devices.

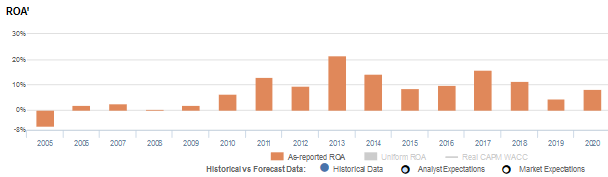

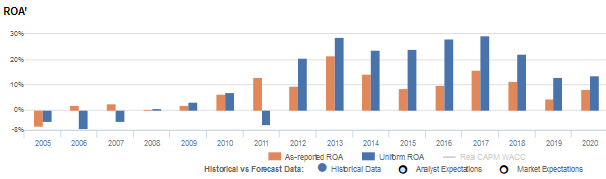

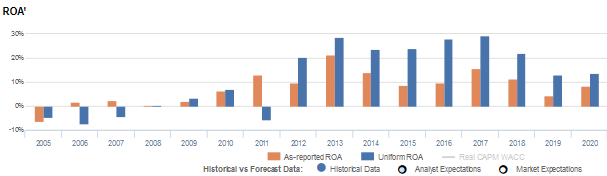

However, as-reported data doesn’t seem to reflect this accurately, with return on assets (ROAs) that have ranged only from -6% to 21%.

On the other hand, Uniform ROAs signal higher profitability levels, ranging from -7% to 29%. Although the company did struggle with returns during the 2000s, which was before the boom of smart devices, it was able to generate returns consistently above 10% when technology became more advanced and as the demand for premium audio solutions rose.

One source of the distortion between Uniform and as-reported ROAs comes from as-reported metrics incorrectly treating R&D as an expense.

R&D is an investment in the long-term cash flow generation of the company. By recording R&D as an expense, this violates one of the core principles of accounting, which is that expenses should be recognized in the period when the related revenue is incurred.

Since as-reported accounting records R&D on the income statement instead of as an investment on the balance sheet, net income can become materially understated.

Cirrus Logic materially spends on R&D as it continues to make investments to improve its existing products and expand its portfolio. The company’s R&D spend has consistently been around 60% of total operating costs, significantly distorting the company’s profitability.

After adjustments, we can see that Cirrus Logic’s Uniform ROAs are actually significantly higher than as-reported ROAs. Without this adjustment, it appears that the firm is having less success with its R&D investments than it really is, leading to poorer valuations.

Cirrus Logic’s earning power is actually more robust than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

Cirrus Logic’s Uniform ROA has actually been higher than its as-reported ROA in the past nine years. For example, as-reported ROA was 8% in 2020, but its Uniform ROA was actually higher at 14%.

Specifically, Cirrus Logic’s Uniform ROA has ranged from -7% to 29% in the past sixteen years, while as-reported ROA ranged only from -6% to 21% in the same time frame.

After inflecting positively from -7% in 2006 to 7% in 2010, Uniform ROA dropped again to negative levels in 2011 before jumping to 29% in 2013. Then, it declined to 24% levels in 2014-2015, before expanding back to 29% in 2017. Thereafter, Uniform ROA compressed to 14% in 2020.

Cirrus Logic’s Uniform earnings margins and Uniform asset turns are in line with as-reported metrics

Overall improvements in Uniform ROA have been driven by compounding improvements in Uniform earnings margins and Uniform asset turns.

From 2006 to 2012, Uniform margins inflected from a low of -17% to 24%, before fading to 20% in 2015 and subsequently recovering to a peak of 27% in 2017. Since then, Uniform margins have compressed to 18% in 2020.

Meanwhile, Uniform turns improved from 0.4x levels in 2005-2006 to peak 1.1x-1.2x levels in 2013-2018, before falling to 0.8x levels in 2019-2020.

At current valuations, markets are pricing in expectations for both Uniform margins and Uniform turns to continue to decline to pre-2012 levels, which may be too bearish, considering management’s positive sentiment.

SUMMARY and Cirrus Logic Tearsheet

As the Uniform Accounting tearsheet for Cirrus Logic, Inc. (CRUS) highlights, the Uniform P/E trades at 16.0x, which is below corporate average valuation levels but above its own recent history.

Low P/Es require low EPS growth to sustain them. In the case of Cirrus Logic, the company has recently shown a 12% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Cirrus Logic’s Wall Street analyst-driven forecast is an 11% and 9% EPS growth in 2021 and 2022, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Cirrus Logic’s $74 stock price. These are often referred to as market embedded expectations.

The company can have Uniform earnings shrink by 2% each year over the next three years and still justify current prices. What Wall Street analysts expect for Cirrus Logic’s earnings growth is above what the current stock market valuation requires in 2020 and 2021.

Furthermore, the company’s earning power is 2x the corporate average. While cash flows and cash on hand are 3x higher than its total obligations—including debt maturities, capex maintenance, and dividends, intrinsic credit risk is 120bps above the risk free rate. Together, this signals a moderate credit risk.

To conclude, Cirrus Logic’s Uniform earnings growth is in line with its peer averages in 2021, but the company is trading below its average peer valuations.

About the Philippine Markets Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com