The call for automation during this pandemic is an opportunity for this company, resulting in a Uniform ROA of almost 8x the as-reported!

Different businesses thrive in different environments. Rising trends such as fintech and automation were previously the center of doubt and debates, but today they seem more viable after the changes brought about by the pandemic.

Automation, in particular, has experienced a significant boost this year due to the implementation of physical distancing measures to contain the spread of the virus.

This company is the biggest supplier of factory automation equipment in Japan, and is greatly benefiting from the rising trend in automation.

However, its as-reported returns do not reflect the tailwinds on the demand for automation. Uniform Accounting shows that this company’s Uniform return on assets (ROA) is more robust than what the market thinks.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Wednesday Uniform Earnings Tearsheets – Asia-listed Focus

Powered by Valens Research

Automation was already a hot topic even before the emergence of COVID-19.

As technological innovations grew in scale over the years, so did the shift from manual to automated processes. In a study by McKinsey in 2017, it was found that around 50% of work can be automated by adapting currently existing technologies.

Despite this, many companies still had little desire to fully integrate new technology into operations due to its high initial costs and the learning curve required for its employees to go through.

Moreover, some companies are wary of potentially triggering social backlash since labor groups claim that too much automation may lead to mass unemployment as machines take over human jobs.

To prove their claims against automation, they cite studies such as McKinsey’s, which estimates that 15% of the global workforce or 400 million workers could be displaced by automation from 2016 to 2030.

However, changes brought about by the pandemic seems to have boosted the growth of automation and have lowered barriers to adoption—-particularly, the outlook of the people involved.

As the coronavirus is spread mainly through close contact from person-to-person, workers worry about how they will stay safe on the job. Most of them worry about the possibility of contracting the virus on the way to and from work, how they will interact with colleagues, and whether it is possible for them to become carriers themselves and bring home the virus to their family members.

Because of employees’ concern for their own safety, employee turnover in factories this year has increased. According to Bloomberg, Chinese companies with production lines have reported a 90% turnover in the workforce after the economy started reopening in March, compared to just 25% to 30% before the pandemic hit.

To resolve this issue, manufacturing companies have become more open to increasing automation in their factories, to the benefit of tech equipment manufacturers.

One of these tech equipment companies is Japan’s Keyence Corporation.

Keyence Corporation develops, manufactures, and sells sensors and measuring instruments used for factory automation and high technology hobby products. Its offerings include fiber optic sensors, photoelectric sensors, programmable logic controllers, laser scan micrometers, bar code readers, and radio-controlled model cars.

Given the changes and risks that have arisen due to the pandemic, investors have started to prefer companies that eliminate humans from the process. Keyence, a company whose business model grows as automation grows, greatly benefits from this.

Since the pandemic began early this year, Keyence’s stock price has jumped by almost 50%. With a valuation of over JPY 11 trillion (USD 100 billion), it has overtaken Japan’s telecommunications giants SoftBank Group Corp. and NTT Docomo Inc., and now sits behind Toyota Motor Corp. as the country’s second-largest company by market capital.

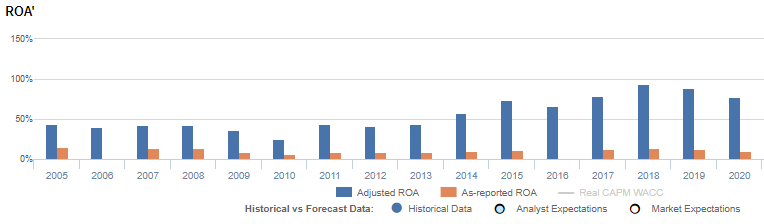

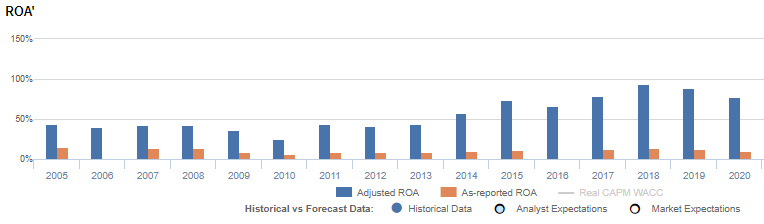

However, despite the tailwinds from automation, as-reported metrics still show Keyence as less profitable than it actually is. For the past sixteen years, the company’s as-reported ROA trended from immaterial levels to an all-time high of just 14%. It is currently sitting at 10% in 2020.

Uniform Accounting tells us that this is a misrepresentation of Keyence’s profitability. In fact, the company’s Uniform ROA is far more robust than what the as-reported figures show.

What as-reported metrics fail to do is to consider the company’s excess cash on the balance sheet. While most companies inherently need some level of cash to operate, the portion of that balance that is earning limited or no return—or excess cash—ends up diluting as-reported ROAs.

When excess cash remains included in the company’s asset base in computing its performance metrics, the company’s profitability and capital efficiency may appear weaker than it actually is. Removing excess cash allows investors to see through the distortions that come from management carrying much more cash on the balance sheet than what is operationally required.

From 2004 to 2020, Keyence has had a significant amount of excess cash sitting idly in its balance sheet, ranging from 32% to 62% of its as-reported total assets.

After excess cash and other significant adjustments are made, Keyence’s Uniform ROA is at 77% in 2020, which is almost 8x higher than its as-reported ROA of 10%.

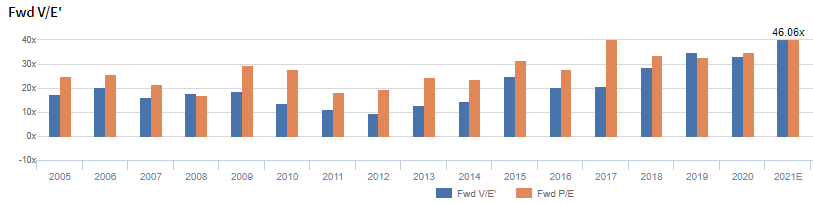

Keyence’s valuations are above global market averages

Keyence Corporation (6861:JPN) currently trades above global market averages at a 46.1x Uniform P/E (blue bars), but below its as-reported P/E of 52.8x (orange bars).

At these levels, the market is pricing in expectations for Uniform ROA to increase to 134% in 2025, accompanied by a 9% growth in Uniform assets going forward.

On the other hand, analysts have less bullish expectations, projecting Uniform ROA to increase to 84% levels in 2022, accompanied by a 2% Uniform asset shrinkage.

Keyence’s profitability is much better than you think

As-reported metrics are distorting the market’s perception of Keyence’s profitability.

If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics highlight.

Keyence’s Uniform ROA has actually been higher than its as-reported ROA in the past sixteen years. For example, as-reported ROA is 10% in 2020, which is almost 8x lower than its Uniform ROA of 77%.

When Uniform ROA reached an all time high of 94% in 2018, as-reported ROA was just at 13%. The company’s Uniform ROA for the past sixteen years has ranged from 25% to 94%, while as-reported ROA ranged only from immaterial levels to 14% in the same timeframe.

Keyence’s Uniform earnings margins are weaker than you think, but its robust Uniform asset turns make up for it

Movement in Uniform ROA has been driven by trends in Uniform asset turns and to a lesser extent, by Uniform earnings margins, with peaks and troughs lining up with that of Uniform ROA.

From 32% in 2005, Uniform earnings margins gradually fell to 24% in 2010, before increasing to 18% levels in 2011-2013. It then peaked at 40% in 2018, before decreasing to 36% in 2020.

Meanwhile, Uniform asset turns fell from 1.4x in 2005 to 1.1x in 2010, before recovering to 2.2x in 2015. It then declined to 2.0x in 2016, before reaching its all-time high of 2.3x in 2018. In 2020, it slightly declined to 2.2x.

SUMMARY and Keyence Corporation Tearsheet

As the Uniform Accounting tearsheet for Keyence Corporation (6861:JPN) highlights, the Uniform P/E trades at 46.1x, which is above the corporate average valuation levels and its own recent history.

High P/Es require high EPS growth to sustain them. In the case of Keyence, the company has recently shown a 14% Uniform EPS shrinkage.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Japan’s Modified International Standards (JMIS) earnings and convert them to Uniform earnings forecasts. When we do this, Keyence’s sell-side analyst-driven forecast is a 7% earnings shrinkage in 2021, before a 29% growth in 2022.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Keyence’s JPY 43,660 stock price. These are often referred to as market embedded expectations.

In order to justify current market expectations, Keyence would need to have Uniform earnings grow by 17% each year over the next three years. What sell-side analysts expect for Keyence’s earnings is below what the current stock market valuation requires in 2021, but is above that requirement in 2022.

The company’s earning power is 13x the corporate average. Also, cash flows are more than 28x higher than its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit and dividend risk.

To conclude, Keyence’s Uniform earnings growth is above its peer averages in 2021, and the company is trading above its peer valuations.

About the Philippine Markets Daily

“Wednesday Uniform Earnings Tearsheets – Asia-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one company listed in Asia that’s relevant to the Philippines and that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

Hope you’ve found this week’s Uniform Earning Tearsheet on an Asian company interesting and insightful.

Stay tuned for next week’s Asia company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com