The real magic of Disney lies in their ability to monetize growth opportunities, and Uniform ROAs of 15%+ show that they’re great at it.

With a string of lucrative acquisitions under their arsenal, this company has cemented themself as a leader in the entertainment business.

They monetized their content through multiple platforms such as franchises, licensing fees, and even theme parks and cruises. The company is earning BILLIONS.

As-reported ROA looks fairly stable for the name. But TRUE UAFRS-based (Uniform) analysis shows that as a result of their monetization strategy, this company has been able to produce robust profitability.

Additionally, new initiatives to grow their platform may provide a tailwind to increases in ROA, exceeding market expectations and providing stock upside.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

No one believed in the success of Snow White.

Although Walt Disney had been creating short cartoons featuring Mickey Mouse and the gang, Snow White was his first actual venture into full-length films. And it wasn’t all smooth sailing.

The film took three years to produce, had a manpower of roughly 750 artists, and needed two million individual paintings to complete. The original budget was $250,000 but Disney ended up spending $1.5 million. Loans had to be taken out, and Walt even had to mortgage his own house.

Everyone said it’d be a box office failure—even his wife!

Snow White eventually premiered, proving the naysayers and non-believers wrong. The movie became a global massive hit, and was the highest grossing film at that time.

This film proved to be pivotal to the success that Walt Disney got, even a century after.

The company went on to produce more box office hits with Cinderella, The Little Mermaid, and more recently, Moana, and Frozen. This followed the fairy tale-esque princess route, of course.

But the majority of Disney’s success, although rooted in films, isn’t in the ticket sales. It’s in their ability to monetize their brands and franchises through multiple platforms.

Disney creates brands and stories. They create characters and worlds.

They then use this universe to make money from distribution and licensing fees, theme park admissions, merchandise sales, and even from cruise packages and vacation club property rentals and sales.

Acquisitions also play a huge part in the expansion of Disney’s content library and additional brands to sell. They now own Pixar, Marvel Entertainment, Lucasfilms, and Twenty-First Century Fox.

Now, they effectively own seven of the top 10 highest grossing films of all time, including four Avengers movies, Avatar, The Lion King remake, and Star Wars: The Last Jedi.

Part of what makes their monetization strategies so successful is the crazy amount of fans that they have.

The fans have always fueled the demand for the company’s content. And they have a lot of it. In the Philippines alone, a market study gathered that about 45 million of 60 million internet users are “unduplicated fans of Disney.” Globally, the company definitely has more.

The company’s ability to leverage their acquisitions and sell their brands to generate value-creating growth opportunities is the real magic of Disney.

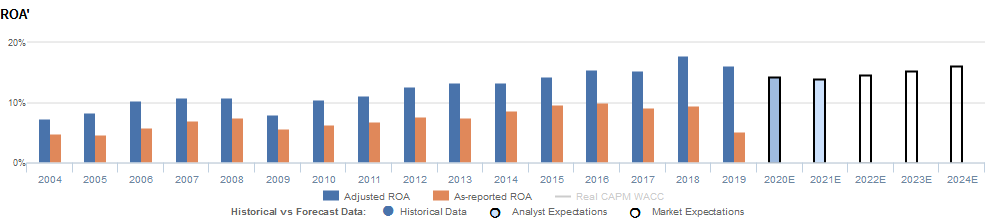

This is also precisely why Uniform ROA has expanded from 7% in 2004 to 16% in 2019 as opposed to the as-reported ROA hovering between only 5% to 10% levels.

With more initiatives coming into the picture, specifically Disney+, the company has the potential to drive Uniform ROA expectations upwards with limited necessary asset growth.

Disney’s earning power is higher than what as-reported metrics show

As-reported metrics significantly understate Disney’s profitability. For example, as-reported ROA for DIS was 5% in 2019, materially lower than Uniform ROA of 16%, making DIS appear to be a much weaker business than real economic metrics highlight.

Additionally, since 2015, as-reported ROA has never exceeded 10%, while Uniform ROA has remained above 14% in each year, distorting the market’s perception of the firm’s recent profitability levels.

Historically, DIS has seen somewhat cyclical, but generally improving profitability. From 2004-2008, Uniform ROA improved from 7% to 11%, before falling to 8% in 2009 amidst recessionary headwinds, and expanding to peak 18% levels in 2018. However, following the acquisition of Twenty-First Century Fox, Uniform ROA decreased to 16% in 2019.

Disney’s P/E is in line with Uniform Accounting metrics

DIS currently trades above historical averages relative to Uniform Earnings, with a 25.7x Uniform P/E (Fwd V/E’).

At these levels, the market is pricing in expectations for Uniform ROA to expand from 16% in 2019 to 18% by 2024, accompanied by 3% Uniform Asset growth going forward.

Meanwhile, analysts have more bearish expectations, projecting Uniform ROA to decline to 14% through 2021, accompanied by modest Uniform Asset shrinkage.

Disney’s earnings margins are overstated while asset turns are understated

Trends in Uniform ROA have been driven by cyclicality in Uniform Earnings Margin, coupled with stability in Uniform Asset Turns.

From 2004-2008, Uniform Margins improved from 8% to 12%, before declining to 10% in 2009 and expanding to 20% in 2018. Since then and after the Twenty-First Century Fox acquisition, Uniform Margins have fallen to 17% in 2019.

Meanwhile, since 2004, Uniform Turns have ranged from 0.8x-0.9x.

At current valuations, markets are pricing in expectations for Uniform Margins to rebound to pre-acquisition levels, coupled with further stability in Uniform Turns.

SUMMARY and Disney Tearsheet

As the Uniform Accounting tearsheet for The Walt Disney Company highlights, the company’s Uniform P/E trades at a very high 25.7x, well above corporate average valuation levels and its own recent history.

High P/Es require high EPS growth to sustain them. In the case of Disney, the company has recently shown only 3% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Disney’s Wall Street analyst-driven forecast is a very concerning negative 14% into 2020. That rebounds with only 2% growth in earnings from 2020 to 2021.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify $146 per share. These are often referred to as market embedded expectations. In order to meet the current market valuation levels of Disney, the company would have to have Uniform earnings grow by 7% each year over the next three years.

What Wall Street analysts expect for Disney’s earnings growth falls far below what the current stock market valuation requires.

To conclude, Disney’s Uniform earnings growth is above peer averages in 2020. Also, the company is trading at below average peer valuations.

The company’s earning power, based on its Uniform return on assets calculation, is above average as well. Together, this signals low cash flow risk to the current dividend level in the future.

About the Philippine Markets Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com