The summit of this conglomerate stock is higher than you might think. Real earning power is 7%, not 4%.

Management teams opt to spinoff existing operating units if it means that those units become more valuable as independent companies. This works for companies like PayPal, whose stock price rose over 200% since its IPO in 2015.

But some companies tend to perform better by heeding the words of the great philosopher Aristotle, who once said, “The whole is greater than the sum of its parts.”

This giant Philippine conglomerate proves that through proper breadth of offerings and the right strategies, having numerous business units helps diversify away investment risk. Their TRUE Uniform ROA shows that the company isn’t as weak as they appear.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earning Tearsheets – Philippine-listed Focus

Powered by Valens Research

In 1954, a man from Cebu decided to risk it all on a loan and entered the cornstarch manufacturing industry. It was a low-margins business, as businesses cut prices to remain competitive.

Against conventional thinking, he doubled down on the risk and expanded the business to other commodities, where the goliaths P&G and Nestlé were playing.

But he did not stop there.

In the 1990s, the company tripled in size. They entered the telecommunications industry, the banking sector, and even petrochemicals. They owned more than 50 shopping malls, and flew more passengers than any other airline in the country.

In an import-oriented local environment at the time, this businessman knew that they needed to set their sights on foreign markets if they wanted to grow.

The company was taken public in 1993 to raise the necessary capital they needed to continue their expansion… this time, to foreign markets.

They imported their products to the rest of Southeast Asia, and even to India and South Korea.

With an eye looking at the future, this businessman, the late business tycoon John L. Gokongwei, Jr., left behind a legacy that is now one of the largest conglomerates in the Philippines, JG Summit Holdings, Inc.

With subsidiaries Universal Robina Corporation, Robinsons Land Corporation, Cebu Air, Inc., JG Summit Petrochemical Corp., and others, the company has been generating solid stock price returns since 2009.

Investors that foresaw this event have enjoyed a 4,230% stock price return, when they realized that the company’s true performance isn’t what investors could glean from using as-reported financials.

It’s only by using Uniform Accounting that we understand what’s causing their earning power to look much weaker than it really is. Return on assets (ROA) are really 7%, not 4%.

Minority interest expense has been the most significant culprit of this understatement. Just in the past five years, it has made up around a third of reported net income.

As it is capital provided by minority interest holders, minority interest expense is rightfully a financing cash flow, and not operating. As such, it should not be deducted from JG Summit’s earnings when measuring performance and comparing it to peers.

JG Summit’s earning power is stronger than you think

Historically, JG Summit Holdings, Inc. (JGS:PHL) has seen improving profitability, up until 2016, when Uniform ROA (blue bars) reached its historical high of 11%, though as-reported ROA (orange bars) will tell you the company only managed half of those ROA levels.

Before the global financial crisis, JG Summit’s earning power was below cost of capital, at 4%. Then it hit a low of -2% in 2008.

In 2009, the company’s ROA started to pick up from 4% that year to 11% in 2016. It declined to 7% levels in 2018.

As-reported metrics would have you believe that the company is struggling to maintain its performance above cost-of-capital levels, when in reality, the company was able to perform above or twice cost-of-capital levels.

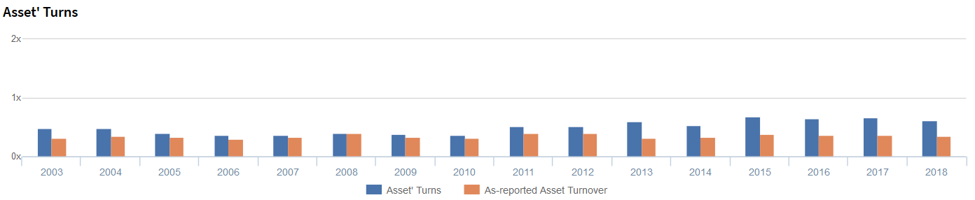

JG Summit’s asset turns are more robust than you think

While the company continues to operate in low-margin industries, the strength of their ROA lies in the strength of their Uniform asset turns, one of the main drivers of profitability, suggesting that the company is more concerned in generating sales for every dollar spent in assets.

Beginning 2011, the difference between JG Summit’s Uniform and as-reported ROA grew wider, as did the difference between their Uniform and as-reported asset turns.

Uniform asset turns have remained stable in the 0.6x-0.7x range over the past four years, while as-reported asset turns are only reporting 0.4x.

The as-reported numbers make the company appear to be much less efficient in churning revenue out of their asset base than real economic metrics highlight. It also distorts the market’s perception of the firm’s historical asset efficiency trends.

SUMMARY and JG Summit Holdings Tearsheet

As the Uniform Accounting tearsheet for JG Summit (JGS:PHL) highlights, JG Summit P/E trades at 19.2x, below market averages, but above its recent averages.

Low P/Es require low, and even negative, EPS growth to sustain them. In the case of JG Summit, the company has recently shown a 45% decline in Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for PFRS earnings and convert them to Uniform earnings forecasts. When we do this, JG Summit’s sell-side analyst-driven forecast is for Uniform earnings to grow at 61% in 2019, and then to a slower growth of 7% in 2020.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify PHP82.00 per share. These are often referred to as market embedded expectations. In order to meet the current market valuation levels of JG Summit, the company would need to have Uniform earnings grow by 5% each year over the next three years.

What sell-side analysts expect for JG Summit’s’ earnings growth is far above what the current stock market valuation requires.

To conclude, JG Summit’s Uniform earnings growth is at par with peer averages in 2020. They are also trading at below average peer valuations.

The company has an average earning power, based on its Uniform ROA calculation, and is trading below peer averages. Together, this signals a low cash flow risk to credit for the firm.

The company’s earning power, based on its Uniform return on assets calculation, is at peer averages.

About the Philippine Market Daily

“Tuesday Uniform Earning Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing himself, Benjamin Graham.

Warren Buffett and Charles Munger of Berkshire Hathaway; David Sanford Gottesman of First Manhattan Co.; Walter Schloss of WJS Partners; William Ruane of Ruane Cuniff, Sequoia Fund; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com