The tobacco industry’s market leader is generating smoking returns by capturing demand with innovation

Smoking has always been one the leading causes of preventable death, which is why governments are adamant about reducing the use of cigarettes by imposing stringent regulations.

These regulations continue to affect this company, as it is one of the largest tobacco companies in the world. Because of this, the company shifted its focus into product innovation, specifically developing cigarettes that are significantly less harmful for its consumers.

However, as-reported metrics show that this company’s venture into less toxic cigarettes haven’t been translating into meaningful returns. On the other hand, Uniform Accounting displays that this company actually has significantly higher returns than what investors think.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

Cigarette smoking causes more than 7 million deaths each year globally.

Although the amount of use varies from person to person, there really is no safe level for tobacco use given its long-term effects. Smoking may cause life-threatening diseases such as lung cancer, stroke, and other heart and lung diseases.

Still, smoking continues to be a bad habit for millions of people worldwide. Some do it because of addiction, while others do it because they feel an increase in alertness and concentration, and feelings of relaxation when they smoke.

Throughout the decades, governments have had to control the use of tobacco. From advertising and marketing restrictions to outright smoking bans in most public spaces, there have been many efforts to reduce the number of smokers.

Of course, Big Tobacco, a group of the world’s largest tobacco companies, has been negatively affected by these legal changes. Most recently, it was announced in the U.S. that the Biden administration is considering legislation that would require a lower nicotine level in cigarettes.

This is the kind of news that sends cigarette stocks tumbling down. Altria Group (MO), for example, has seen a declining trend in its share price since its peak in 2017.

For over 180 years, Altria Group (MO), formerly Philip Morris Cos., has been the undisputed market leader in the U.S. tobacco industry. Though it may make sense that Altria would be fighting against the stringent regulations, the company has actually committed itself to being part of the solution.

Specifically, Altria believes that the future of the tobacco industry is about innovation, harm reduction, and informed consumer choice. Thus, there is a renewed focus on new approaches to converting adult smokers to non-combustible products like IQOS.

IQOS is an electronic device that heats tobacco to release nicotine without combustion, fire, ash, or smoke—“heat-not-burn” product—using the company’s patented HeatControl™ Technology.

Altria’s portfolio of non-combustible products also include other tobacco categories such as Oral Tobacco-Derived Nicotine (OTDN) and Electronic Nicotine Delivery Systems (ENDS) or E-vapor products.

Most of the toxic chemicals are formed as a result of combustion, so removing that element should significantly reduce the smokers’ exposure to those chemicals.

That said, combustible or non-combustible products aside, nicotine is still a highly addictive substance. This is what makes cigarettes an inelastic good—demand is persistent because the users are addicted to the product.

This also means that demand should be of little concern for the company regardless of the regulations thrown their way.

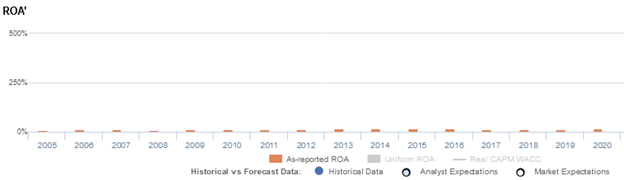

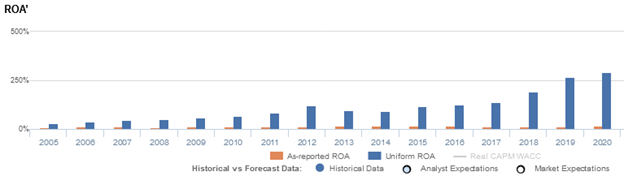

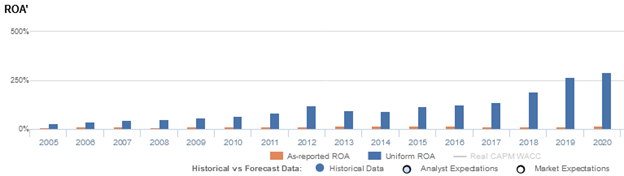

Looking at as-reported return on assets (ROAs), however, this does not seem to be the case. Altria has only sustained ROAs of 11%-16% in the past decade.

In reality, Uniform Accounting paints a significantly different picture, with Uniform ROAs that are 20x higher than as-reported ROAs in recent years. Furthermore, returns have continued to trend upwards, reaching a new high of 292% in 2020, opposite what stable as-reported metrics reflect.

This signals that the company has actually done a great job of adapting to the changing legal environment, and shows how relentless the demand is for addictive products such as cigarettes.

The distortion between Uniform and as-reported ROAs comes from as-reported metrics failing to consider the amount of non-operating long-term investments on Altria’s balance sheet..

These long-term investments are intangible assets that are purely accounting-based and unrepresentative of the company’s actual operating performance. When as-reported accounting includes this in a company’s balance sheet, it creates an artificially inflated asset base.

As a result, as-reported ROAs are not capturing the strength of Altria’s earning power. Adjusting for non-operating long-term investments, along with the other necessary adjustments Valens makes, we can see that the company isn’t actually displaying lackluster performance. In fact, it is the complete opposite, with returns that are 20x greater.

Altria’s earning power is significantly more robust than you think it is

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think the company is a much weaker business than real economic metrics highlight.

Altria’s Uniform ROA has actually been significantly higher than its as-reported ROA in the past sixteen years. For example, Uniform ROA was at 292% in 2020 while as-reported ROA was only at 15%.

Historically, Altria’s as-reported ROA has ranged from only 8% to 16% in the past sixteen years while Uniform ROA has ranged from 31% to 292% in the same timeframe.

From 2005 to 2012, Uniform ROA steadily rose from 31% to 121%, before fading to 92% in 2014 and subsequently expanding to a peak of 292% in 2020.

Altria’s Uniform earnings margin is weaker than you think, but its Uniform asset turns make up for it

Overall improvements in profitability have been driven primarily by trends in Uniform asset turns and to a lesser extent, recent trends in Uniform earnings margin.

After jumping from 37% in 2005 to a high of 92% in 2006, Uniform margins collapsed to 19% in 2008. Subsequently, Uniform margins slowly recovered to 42% in 2019, excluding a 21% underperformance in 2016, before fading to 32% in 2020.

Meanwhile, Uniform turns compressed from 0.8x in 2005 to a low of 0.4x in 2006, before rebounding to 4.6x in 2012. Thereafter, Uniform turns dropped to 3.1x in 2013 and then steadily expanded to a peak of 9.2x in 2020, excluding a 3.9x underperformance in 2017.

At current valuations, the market is pricing in expectations for a reversal of recent improvements in Uniform turns, coupled with continued compression in Uniform margins.

SUMMARY and Altria Group, Inc. Tearsheet

As the Uniform Accounting tearsheet for Altria Group, Inc. (MO:USA) highlights, the Uniform P/E trades at 12.1x, which is below the global corporate average of 23.7x, but around its own historical P/E of 12.2x.

Low P/Es require low EPS growth to sustain them. In the case of Altria, the company has recently shown a 22% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Altria’s Wall Street analyst-driven forecast is a 24% and 10% EPS growth in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Altria’s $47.62 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 9% annually over the next three years. What Wall Street analysts expect for Altria’s earnings growth is above what the current stock market valuation requires in 2021 and 2022.

Furthermore, the company’s earning power is 49x the long-run corporate average. Also, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. Meanwhile, intrinsic credit risk is 50bps above the risk free rate. All in all, this signals a moderate dividend and low credit risk.

To conclude, Altria’s Uniform earnings growth is significantly above its peer averages. However, the company is trading below average peer valuations.

About the Philippine Markets Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com